I have written several articles about the upcoming Churchill Capital IV (NYSE:CCIV) reverse merger with Lucid Motors. I still think CCIV stock (the new symbol will be LCID after the merger) is at least 33% undervalued, based on my model, described in my prior articles. I can walk you through the highlights in this article.

But first, I want you to know, that I have more than a passing interest in this situation. After all, I live in Arizona where the first Lucid factory has been built (just south of Phoenix). It is in a highway town called Casa Grande (“Big House”) just off of I-10 that connects Phoenix and Tucson, the two largest Arizona cities. Everyone stops in Casa Grande on the way to Tucson, and vice versa. It takes less than an hour to get to and from Phoenix. I suspect they built there since this it’s one of the fastest-growing areas in Arizona. Casa Grande has very low prices for land and homes right now.

What’s more, management has now clearly said once again this past week that they expect to begin producing electric vehicles (EVs) by the second half of 2021. There’s no bull with this special purpose acquisition corporation (SPAC) merger. It is a real company with real prospects and definite production. So, despite what you hear about some SPACs being too speculative to invest in, this is a real company.

How To Value Lucid Motors

The easiest way to value Lucid Motors is to calculate its forecast market value, and then its enterprise value and compare its forecasts with peers. I have done this in several of my past articles, so here are the highlights.

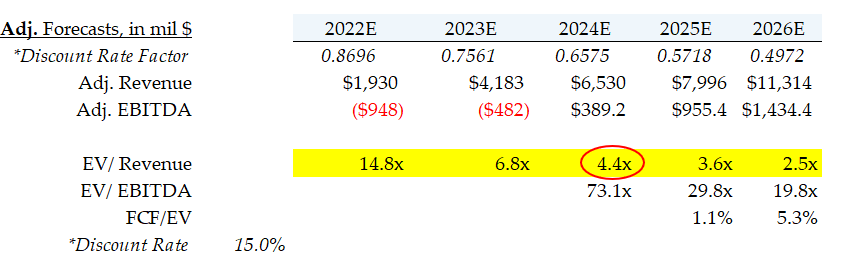

First, at the closing price of Friday, April 23, of $20.55, the pro forma market cap was $32.78 billion, based on an estimated 1.5997 billion shares to be outstanding, not including warrants. Moreover, the enterprise value (EV), after receiving $4.405 billion in cash at the merger close, will be just $28.468 billion.

Therefore, using the company’s own forecasts, LCID stock trades for just 5 times EV/Revenue in 2023 and 2.9 times based on the 2024 forecast.

Click to Enlarge

You can see this in the table above. Moreover, the company also expects to be EBITDA profitable (earnings before interest, taxes, depreciation, and amortization) by 2024.

Peer Comps

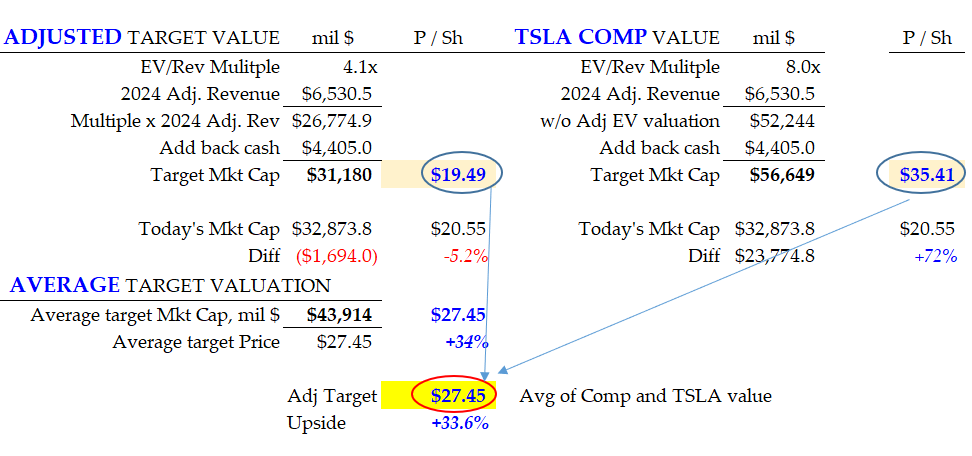

Lucid Motors provides a comp with other EV stocks. For 2024, the median EV-to-sales multiple is 4.1 times. LCID stock, on a pro forma basis trades for just 2.9 times sales, so it is 29.2% undervalued. That implies a gain in the stock of at least 41.4% (i.e., 1 divided by (1-0.292) is 41.4%).

However, if we adjust the 2024 revenue by a 15% discount rate, to account for the time value of money, it falls by 34.25%. Therefore, LCID’s revalued enterprise to sales ratio is 4.4 times.

Click to Enlarge

You can see this in the table on the right. This implies a slight fall in LCID stock’s value to just $19.49 (-5%).

On the high end of the range, Tesla (NASDAQ:TSLA) trades for 8 times revenue. At that price, LCID stock should be worth 72% more or $35.41 per share.

Click to Enlarge

The table above shows these two calculations and how the average is $27.45 per share. This implies a potential 33.6% gain in the CCIV stock price (LCID post-merger).

What To Do With CCIV Stock

The bottom line here is that I have shown that CCIV stock is worth somewhere between $19.49 and $35.41 per share. The stock could end up trading anywhere between these two valuations, but the average is $27.45, or one-third higher.

That is still a very good potential return for most investors. In fact, even if it took two years for that price to happen, the return is still 15.59% annually on a compounded basis. That is also a good return for most investors. Either way, using an average estimate, including a 15% compounded discount rate on revenue, expect to see CCIV stock (LCID stock post-merger) hit $27.45 sometime in the next two years.

On the date of publication, Mark R. Hake held a long position in Tesla (TSLA) stock.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.