After a rough start following its initial public offering, Coupang (NYSE:CPNG) stock has been in a narrow trading range between $38 – $45.

Its lack of real movement either way is puzzling.

On July 12, inews24 posted that Coupang will acquire the trademark for “Coupang Biz.” If true, the retailer’s focus on the small business segment will widen its prospects.

The growth in self-employment that has taken hold in North America is bound to follow in Asia. As that happens Coupang likely will increase its addressable market by selling office supplies to the business customer via Coupang Biz. It already has one of the fastest online delivery logistics in the world.

Coupang claims that it delivers goods faster than Amazon.com (NASDAQ:AMZN) with 99.3% of its orders delivered within 24 hours of purchase.

For example, Dawn Delivery, introduced in 2019, will guarantee delivery by 7 a.m. for orders received before midnight the previous day. The exceptional efficiency does not come without a cost: employee safety is at risk.

On June 25, Coupang’s logistics center warehouse caught fire. The death of a firefighter adds to the list of incidents that are hurting the firm’s reputation.

It would only take an extended boycott to hurt Coupang’s growth prospects. Customers may pressure the retailer to prioritize worker safety and staff well-being over efficiency.

A Closer Look at CPNG Stock

Click to Enlarge

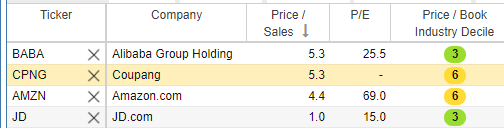

Valuations are another risk factor for Coupang investors. The stock trades at a price-to-sales ratio above that of its peers like JD.com

(NASDAQ:JD), Amazon.com, and Alibaba (NYSE:BABA). Its price/book industry decile is a low rank at 6, compared to a 3 for Alibaba and JD.com.

Considered the “Amazon of Asia” just as Alibaba is the “Amazon of China,” Coupang’s first-quarter strength indicates the year is off to a good start.

The company posted revenue growing by 74%, to $4.2 billion. Active customers grew by a steady 21% to 16.04 million. Active customers spent more on average, spending $262 each and up 44% Y/Y.

Coupang’s EBITDA loss rose from negative $42 million last year to $133 million. Operating, general and administrative costs rose. Also, investments in expanding its fulfillment center capacity, technology infrastructure and higher staff costs added to the losses.

Growth investors know all too well that the early costs are necessary for the early phases.

Coupang tested its services in Japan, selling food, drinks and daily necessities. It continued that expansion with Taiwan.

Depending on the customer response, Coupang may expand its product offering and increase its presence, adding to operating costs while increasing the sales potential. Investors need to take a position on the chances of its success. After its consistent branding and customer demand strength in South Korea, chances are high that Coupang will establish itself in Japan and Taiwan.

On Wall Street, analysts have an even number of “buy” and “hold” ratings on Coupang shares. The average price target is $46.60, according to Tipranks.

Your Takeaway

Coupang has plenty of investor support from the hedge fund community and with Softbank Group. Softbank invested $3 billion in Coupang for a 37% stake.

After Coupang raised $4.6 billion from the IPO, Softbank made $33 billion, at least on paper. Should it need more money, Coupang’s investors will not hesitate in helping.

The internet retailer built a strong moat in South Korea and is expanding in Asia. It faces no near-term threats from Amazon.com.

Alibaba is busy with growth in its Domestic market – China – that it will not compete with Coupang in the same markets.

Provided the Nasdaq index does not face a correction, Coupang stock should begin trading higher from here.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.