- Investors should not ignore value stocks any longer.

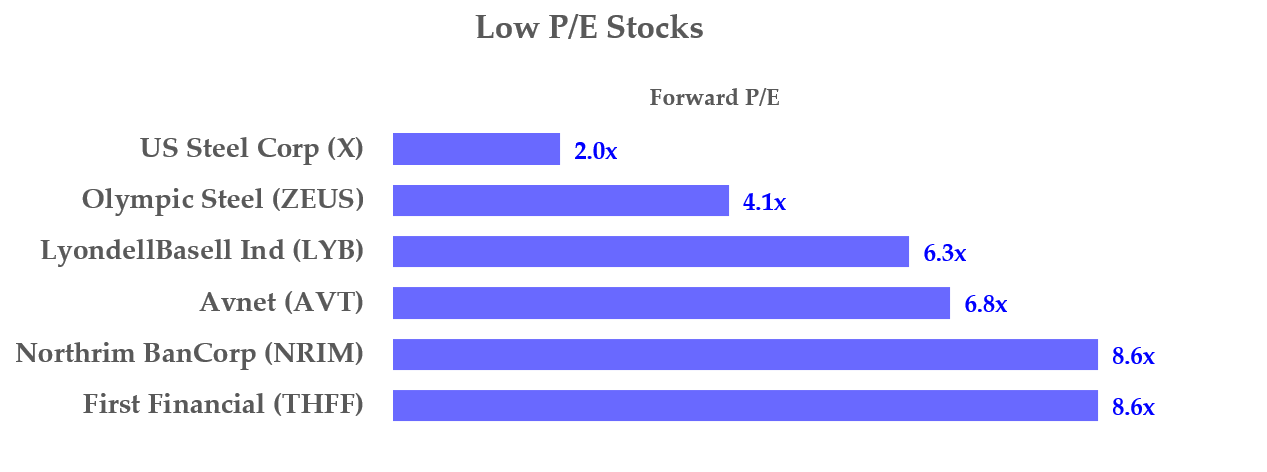

- United States Steel (X): This steel producer trades at 75% of its tangible book value, pays a 0.8% dividend, and trades for 2 times forward earnings.

- Olympic Steel (ZEUS): Another steelmaker trading at 96% of tangible book value, 4x forward earnings with a 0.6% yield.

- LyondellBasell Industries (LYB): This chemical company trades on a 6x forward P/E ratio, good growth, and a 4.10% yield.

- Avnet (AVT): This electronics distributor has a 6.8 forward P/E, good earnings growth, and a 2.23% dividend yield.

- Northrim BanCorp (NRIM): This midcap Alaskan bank has an 8.6x P/E, a 3.93% dividend yield, and has consistently raised its dividend over the past 12 years.

- First Financial (THFF): This Midwest bank trades for just 125% over its tangible book value, 8.5x forward P/E, and a 2.49% dividend yield.

Sometimes the best time to buy downtrodden stocks is when they are falling, even though they are already cheap. And these six value stocks are so cheap per their value metrics, like price-to-earnings (P/E) and price-to-book value (P/BV) that they are too low even for most value investors. Traditionally, value investing involves picking stocks near their lows in terms of the price-to-asset ratios, or low P/E ratios. So I think investors should pick up these bargain stocks now while they’re cheap despite the risk that their price might fall further.

Click to Enlarge

Additionally, these stocks also all pay dividends, which affords investors the ability to get paid while they wait for their prices to rise.

The cheapest of these stocks trades at just 2x forward earnings projections. The chart on the right shows the ranking of these six stocks by P/E.

Let’s dive in and look at these six value stocks:

| X | United States Steel | $24.59 |

| ZEUS | Olympic Steel | $34.10 |

| LYB | LyondellBasell Industries | $107.03 |

| AVT | Avnet | $46.54 |

| NRIM | Northrim BanCorp | $39.84 |

| THFF | First Financial | $44.26 |

United States Steel (X)

Market Capitalization: $6.2 billion

United States Steel (NYSE:X) is a flat-rolled and tubular steel maker that is too cheap. It trades at 75% of tangible book value and just 2 times forward earnings, according to Refinitiv’s survey of analysts (seen on Yahoo Finance’s statistics tab).

This is due to the market’s overzealous worry about a worldwide slump in economic activity including steel products. The worst of the future bad news is already in the stock price.

However, the problem is that the company is not in bad financial shape. For example, its debt-to-equity ratio is only 43% (again on the Yahoo Finance stats page), and its free cash generation is still positive. In fact, in the last quarter (Q1), U.S. Steel made $771 million in cash flow from operations (CFFO). After deducting $349 million in capital expenditure (capex) spending, it still made free cash flow (FCF) of $422 million.

That means that its cash balance won’t keep falling, and more importantly, its FCF ratio is now very attractive at 27.2% (i.e., ($422 x4)/$6.2b). That is a huge FCF yield. Its dividend yield of 0.82% and the repurchase of $122 million of its stock in Q1 make X stock one of the best value stocks.

Olympic Steel (ZEUS)

Market Cap: $363.6 million

Olympic Steel (NASDAQ:ZEUS) is an Ohio-based steel producer like U.S. Steel. It is cheap as well. It trades for just 4.1 times forward earnings and just 96% of its tangible book value. Moreover, the stock pays a slightly higher yield at 0.64%.

However, Olympic Steel has a higher debt-to-equity ratio of over 73% and also is generating negative FCF. That makes its cheap valuation somewhat suspect. For example, if it keeps burning through cash like this it will have to sell assets or borrow more money, or even raise equity.

For that reason, this might now be as good a value stock as United States Steel but it is still “statistically cheap” in terms of its typical value-based metrics.

LyondellBasell Industries (LYB)

Market Cap: $35.3 billion

LyondellBasell Industries (NYSE:LYB) is a Houston-based global chemical producer. The attraction to this stock is that it trades on a 6x forward P/E ratio, has good earnings growth, and has a 4.10% dividend yield. For example, earnings per share (EPS) are forecast to rise from $16.80 this year to $16.98 next year.

However, the company’s financial position is not particularly exciting. Its debt-to-equity ratio is over 100%, meaning that debt exceeds its equity (i.e., debt is greater than assets by the amount of equity).

Nevertheless, the stock’s cash flow generation is strong. Last quarter it produced $1.5 billion in CFFO and after capex spending of $446 million, the company’s FCF was over $1 billion ($1.06 billion). Therefore, its $4.2 billion annual run-rate FCF represents 12% of its $35.3 billion market value. That is a huge FCF yield and represents and makes it one of the cheapest large-cap value stocks.

Avnet (AVT)

Market Cap: $4.5 billion

Electronics distributor Avnet (NASDAQ:AVT) pays a $1.04 dividend annually which gives the stock a 2.2% dividend yield. The company has paid a dividend annually for the past eight years. Moreover, at $46.30 per share the stock is trading on a forward P/E of just over 6.8.

Earnings are forecast to rise from $2.71 earnings per share (EPS) in 2021 to $6.85 this year and $6.82 next year. This is mainly due to the higher price of chips and other technology-related items, as well as higher logistics-related revenue.

Avnet’s total debt-to-equity is just 38%, making its financial situation secure. In addition, the company produced $232 million in FCF last quarter. This shows that it is not burning through its cash balance. That again is a very conservative financial trait for the company.

With these stats, Avnet is a cheap stock and one of the better value stocks.

Northrim BanCorp (NRIM)

Market Cap: $228 million

Northrim BanCorp (NASDAQ:NRIM) is an Anchorage, Alaska community bank and home mortgage lending company. Value investors like it because it has an 8.6x P/E, good growth prospects, and a 3.93% dividend yield. Moreover, the bank has consistently raised its dividend over the past 12 years and has paid a dividend in each of the last 26 years.

Moreover, the company’s latest financials show it has a tangible book value (TBV) of $194.4 million. Compared to its $228 million market value, that means its stock market value is only 17% over the TBV. That makes it a very cheap stock.

Moreover, analysts forecast that earnings will rise from $4.57 this year to $6 next year. Assuming there is no major recession that could put a dent in these forecasts, this makes gives the company good earnings growth. Moreover, the cheap valuation and dividend yield make NRIM stock one of the best value stocks.

First Financial (THFF)

Market Cap: $541.5 million

First Financial (NASDAQ:THFF) is a Midwestern bank, operating in 78 branches in Indiana, Illinois, Kentucky, and Tennessee. It is attractive because the stock trades for just 125% over its tangible book value, 8.5x forward P/E, and a 2.49% dividend yield.

For example, its tangible book value as of March 31 was $431 million, compared to the $541.5 million market capitalization. That means its stock price is only 25% over the tangible value of its earning net assets (after deducting all liabilities).

This Midwestern bank makes money with commercial and residential lending. It has paid a dividend in each of the last 27 years. It has also raised the dividend in every one of the last six years. That gives investors confidence that the company should be able to weather any kind of future economic downturn.

The bottom line is that much of the forecast bad news is already in the stock price. That makes THFF stock one of the best value stocks going forward.

On the date of publication, Mark Hake did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.