It has handily outperformed the broader market this year and investors are now in a stronger position to continue rallying equities as we close out a gloomy June. But when it comes to blue-chip Visa (NYSE:V), are V stock investors wiser to buy now, or pay later?

Up until this past Friday, conversations of a dead cat bounce in the S&P 500 made sense following fresh year-to-date lows formed the prior week. But in closing out the abbreviated four-day period, investors received a more certain shot in the arm.

The index signaled a bullish follow-through day (FTD) and a historically critical element in eradicating 2022’s bear market. And financial payments giant V stock continued its streak of demonstrating outsized strength. Amid the burly broad-based buying, Visa shares gained more than 4.5% to outpace the S&P 500 by more than 100 basis points.

But not all FTDs ultimately work. This year alone, we’ve had a couple of the key technical events fail. That being said, let’s review what else is happening both off and on the V stock price chart to determine when and how bullish Visa investors won’t regretfully pay for their “buy” decisions.

| Ticker | Company | Price |

| V | Visa Inc. | $199.37 |

Visa Is a Card Carrying Blue-Chip With Growth

Dizzying inflation. Rate hikes. At-risk and less-than-confident consumers. Welcome to 2022. But amid all the bad actors hanging over a stock like Visa, the blue-chip has continued to deliver with enviable growth.

Visa reported its second quarter (Q2) results in late April. The company showed year-over-year top-line growth of over 25% on non-GAAP earnings that climbed by nearly 30%. The burly gains also easily bested Street forecasts by 5.21% and 8.39%, respectively. Additionally, they helped boost already strong compounded annual growth rates (CAGR) for revenue and earnings per share (EPS) to 7.4% and 9.5% over the last three years.

Moreover, Wall Street forecasts for fiscal-year growth of just over 21% and has long-term five-year projections of 18%. Not only that, but Visa’s business could be potentially strengthened by new product launches, such as Visa’s collaboration with Fundbox for small business or a “Buy Now, Pay Later” solutions. With this in mind, the outlook for V stock looks bright.

V Stock Optimism Versus Bear Market Realities

Click to Enlarge

Another viewpoint which reflects optimism is V stock’s consensus 12-month price target. According to CNN, analysts are forecasting a range of $225 to $292 for shares, with a median prediction of $270. The median implies upside of 35.1% from today’s price.

But the bullishness may not be as easy to capture as Wall Street would have us believe. All stocks, as 2022 has reminded us, go through corrective periods with larger cycles turning into bear markets.

In the case of V stock, shares have declined 26% at their June low since peaking 11 months ago at $250.99. The correction is no small feat in light of the blue-chip’s capitalization of $430 billion. But there are comparisons that seem relevant that continue to warn otherwise.

With the tech and growth focused Nasdaq still off 29% year-to-date compared to V stock’s decline of 8.7%, buying now could have investors paying later in a bad sort of way.

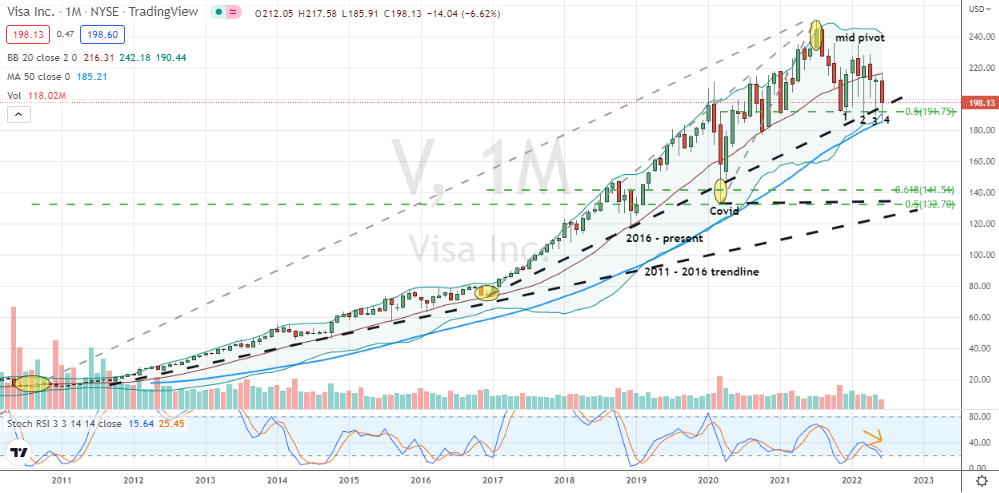

V Stock $130 to $142 Price Target

Technically, V stock is also hinting that a larger bearish cycle is in the offing. In reviewing Visa’s extended monthly chart, multiple tests of V’s 50% Covid-19 level are breaching the once-broken trend support from 2016.

Framed another way, Visa’s downside risk has grown following two bullish double bottom pattern failures after candles #2 and #3 formed. Regardless, those situations are made more concerning with stochastics bearishly rolling over, as well.

Should June’s low fail, the observation is a move to $130 to $142. A challenge of longer term supports dating back more than a decade is possible over the next several months. If correct, that puts V stock exposure at 27% to 34% for today’s buyers.

Bottom-line and regardless of how bullish investors see things in Visa, a longer term and actively-managed collar can help with shoring up risk on any stock merchandise purchased. Additionally, it could help avoid paying later with buyer’s remorse on a purchase right now.

On the date of publication, Chris Tyler did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.