Given the recent headlines and expert opinions, now doesn’t feel like a particularly great time to purchase a home. Although home prices continue to rise, rising interest rates set the stage for a sudden squelching of demand that could gouge prices.

At the same time, while home prices have grown tremendously since 2011, that growth may have been more a function of limited supply than overwhelming demand.

If the supply spigots suddenly get turned on by home builders, like KB Home (NYSE:KBH) or Beazer Homes USA, Inc. (NYSE:BZH), that finally break their self-imposed discipline, that too could drag new home buyers underwater shortly after taking on a home loan.

What if, however, the real estate market was actually poised to climb its wall of worry?

That’s apt to be the case.

Ask ten realtors if now is a good time to buy a home, and you’ll likely hear “yes” all ten times (and in all ten cases, the agent in question will just happen to have a listing you have to see).

Even beyond the self-serving rhetoric from realtors, though, now may well be a great time to purchase a new home despite what seems like relatively high home prices. Three reasons stand out among the rest.

Interest Rates Are Still Relatively Low

Yes, as of March, the Federal Reserve has imposed six quarter-point rate hikes since coming out of the subprime meltdown. Depending on when you read this, that tally may be seven. The Fed was/is largely expected to raise interest rates again in mid-June.

The average interest rate on a 30-year mortgage now stands at a 4.56%, matching its multiyear peak hit back in the fall of 2013. The 2016 low rate of around 3.4% isn’t even a fading memory anymore.

A little perspective may be in order, though. Between 2003 and 2008, the average 30-year loan sported an interest rate of around 6.0%.

Click to Enlarge

It’s also worth bearing in mind that while 4.56% is a quarter point more than the rate of 4.31% available just a few weeks ago, on a typical $250,000 mortgage, that only increases the monthly payment from $1239 to $1276. That $37 difference isn’t earth-shattering.

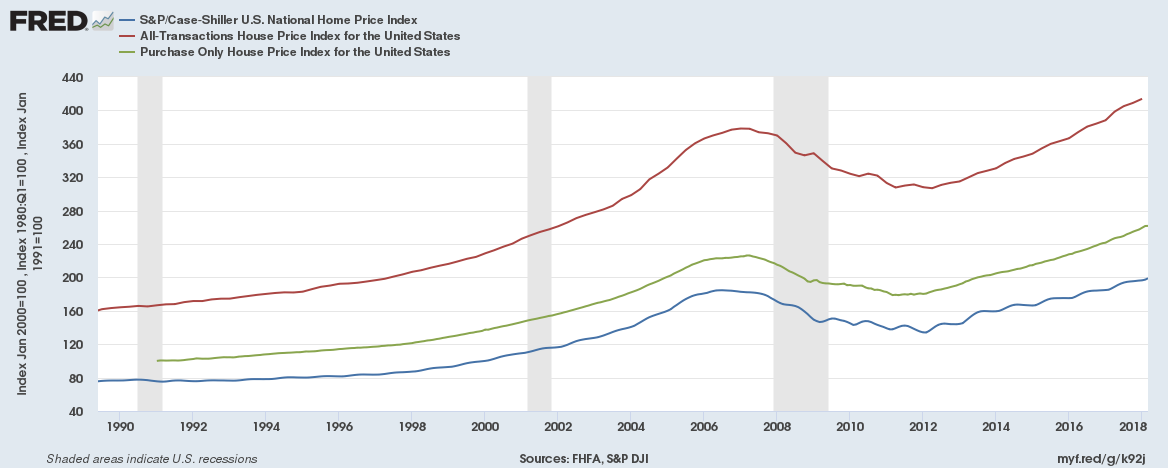

Home Prices Are Still Relatively Low

Whether you’re talking about the FHFA’s data or the Case-Shiller home-price index, the average reported home sales price now exceeds 2006’s highs, loosely implying we’re back in the same frothy boat we were in just a decade ago.

Click to Enlarge

A little perspective may be in order, though.

First, with the exception of 2008’s highly unusual circumstances, home prices have always edged higher — even when that growth may have slowed down during a recessionary phase. Second, after factoring in the inflation that’s occurred between 2008 and 2018, home prices are actually still lower than where they were a decade ago.

Granted, incomes are also not what they were then, once adjusted for inflation. But as of March, wage growth is accelerating again. We may have just unlocked another wave of would-be home buyers.

The Economy Is Still Accelerating

Last but certainly not least, buying a home sooner than later makes sense simply because a booming economy has only just started to prod that next tranche of home buyers into the market. The stronger the economy gets and the better incomes workers earn, the more they’ll demand houses.

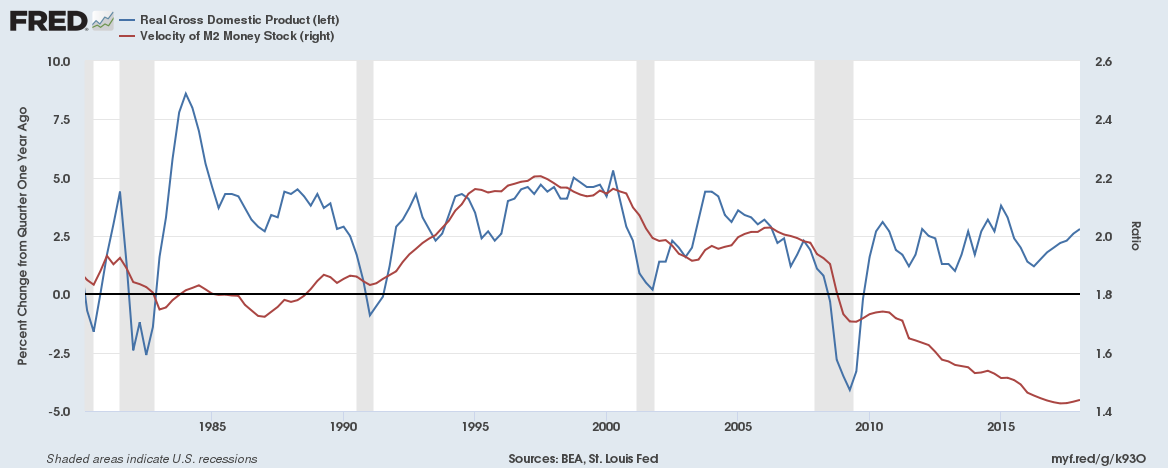

Yes, the economy has technically been on the mend since 2009. We’re now actually in one of longest economic growth phases ever seen, suggesting a recession is inevitable in the foreseeable future.

And, maybe it is.

But take a closer look at the economic data now and compare it to the economic data logged between 2009 and 2016, and you’ll see the pre-2016 economic growth pace was tepid. Namely, the velocity of money — the number of times a dollar exchanged hands over the course of a 12-month stretch — continued to fall to multi-decade lows despite forward progress for the nation’s GDP.

As of the third quarter of last year, though, we’re finally seeing the velocity of the greenback start to edge higher in step with real, sustainable GDP growth. A couple of major banks are looking for Q2 GDP growth of around 3.7%, which would be one of the best growth readings in years.

Click to Enlarge

Bottom Line on Home Prices

Don’t misread the message. In certain markets, it remains all too easy to pay too much for a house that will be difficult to sell if and when such a time comes.

There are real estate investments meant to pay off for the long haul, providing you a place to live in the meantime. Then there are bad bets taken on by buyers that make misguided assumptions about a job, an industry, or about what they can afford.

There’s also always that chance of an economic curveball.

But, for most consumers and potential home buyers that just want a nice, affordable house that will appreciate in time, the current environment isn’t even anything close to being a repeat of 2008’s wildly overheated real estate market.

Go ahead and start looking before a few-too-many soured loans force lenders to make borrowing more difficult for everyone. There’s more currently working in favor of home prices than not.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.