Welcome to Eric Fry’s Smart Money!

It has long been said that the market is dominated by one of two emotions: fear or greed.

Though in truth, the two work in tandem. It’s what makes a market a market; you need both a buyer and a seller, a bull and a bear.

We don’t need to tell you that in the first quarter of 2022, fear was clearly in the driver’s seat. The chaotic conditions in the stock market have been creating a stiff headwind for most stocks… to the point that a market crash is not out of the question.

And while investors often see crash as a four-letter word, big market dips allow you to purchase the best stocks out there and to diversify your portfolio.

We should not ignore the risks out there, but neither should we let them chase us out of the market. We’ve found it works better to stay with the high-quality stocks you own… and to add positions in the strongest stocks out there.

In other words, the best defense is a strong offense.

Stay Confident

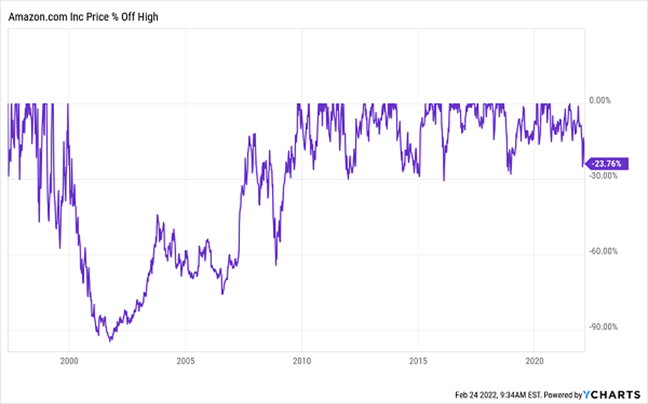

Think about Amazon.com Inc. (AMZN) for a second. That stock is up more than 100,000% since it went public, yet there were massive drops along the way.

Look at the chart below, and you can see multiple 30% pullbacks, a few 60% drops… and even a 90% plummet back in 2001.

After every single falter, Amazon shares went on to new highs for one reason: The company itself matters much more than the broad market, the economy, or anything else.

If a business is innovative, provides value to customers, outperforms the competition, has a smart business model, and operates in a powerful trend, odds are incredibly high it will grow substantially and become a moneymaker over time.

It is easy to lose sight of that fact when you’re watching stock prices go down. It is easy to want to sell everything and crawl into a hole until the storm passes.

But that’s not what the great investors do. Instead, they stay with high-quality stocks they already own and add positions in new stocks in which they have high confidence.

By the way, the stock market has a perfect record of recovery. There have been more than a dozen bear markets since 1930. Stocks rallied to new all-time highs after every single one, from Black Monday in 1987 (when the Dow Jones Industrial Average fell 22% in one day)… to the dot-com bust in the early 2000s… to the financial crisis of 2008.

Zooming out even further, stocks appreciated about 1.5 million percent in the 20th century. And if you know your history, you know that century was filled with wars, recessions, depressions, crises, bear markets, and more.

That said, even though it’s the best time to do so, we hate spending during market crashes. That’s just human nature.

When the headlines are scary and investors are selling pretty much anything and everything, it can cause even the best and most experienced investors to tuck their wallets in their back pocket and turn off their brokerage account.

That’s why, in this report, we’re showing you five stocks with share prices right around or under $20. However, these aren’t volatile “penny stocks” or bleeding-edge microcap tech startups that aren’t showing profits or even rising sales yet.

In his premium services, Smart Money Editor Eric Fry uses a unique set of criteria, which we’ll tell you about in a minute, to separate the likely winners from the likely losers. Eric then dives even deeper to determine which stocks he recommends to his paid-up subscribers.

In this report, we’ve screened the entire stock market to find five low-cost stocks that pass through the “Fry Formula.” While these aren’t immediate “Buys” that Eric is recommending – you’ll want to do your own deeper dive – you can feel comfortable that all five are worth a closer look.

With this list in hand, you can put together a basket of “cheap” stocks that could help you prosper during a potential market crash without spending a bundle.

Let’s take a look…

Cheap Stock No. 1: Arcos Dorados Holdings Inc. (ARCO)

- 52-Week High/Low: $4.33–$8.44

Eagle-eyed linguists will notice that the first company on our list of cheap stocks’ Spanish name translates to “Golden Arches,” which aptly describes its corporate focus.

Arcos Dorados Holdings Inc. (ARCO) manages more than 2,200 McDonald’s restaurants throughout South and Central America and the Caribbean. The company operates 1,580 units directly, while sub-franchisees operate 662 of them.

As a franchisee, Arcos pays a 5.3% royalty fee to the mothership, McDonald’s Corp. (MCD). Arcos’s agreement with McDonald’s expires in 2027 but is renewable at decade-long intervals thereafter.

The COVID pandemic dealt a harsh blow to Arcos’s operations, but the company is highly leveraged. Its net debt is nearly four times annualized EBITDA (gross earnings), which puts Arcos in the neighborhood of “junk credit” companies.

That’s the bad news.

The good news is that Arcos’s leverage ratio has been falling rapidly. Therefore, as the company’s operations continue to recover, its net debt could easily fall to a comfortable two times EBITDA by the end of this year.

Furthermore, the Arcos balance sheet includes significant “hidden assets,” which could be tapped in an emergency. The company owns the land under about 500 of its restaurants. That land could probably fetch close to $1 billion – a figure that is nearly equal to Arcos’s entire net debt.

But asset values are not the reason to invest in Arcos, a profit recovery is. That recovery is already underway.

The company has produced a net profit in each of the last two quarters and will likely post another one when it reports earnings on Mar. 16.

Looking ahead, Arcos’s earnings per share (EPS) should top $0.30 this year and $0.40 in 2023. At that level of profitability, the stock would be trading for 20 times this year’s earnings and 16 times the 2023 result.

That valuation might not qualify the stock as a “bargain basement” special. But adaptive companies like Arcos rarely tumble to deeply distressed valuations.

Cheap Stock No. 2: Coty Inc. (COTY)

- 52-Week High/Low: $7.24–$11.12

Heavy insider buying is one of the reasons to consider the next stock on our list, but it isn’t the only one.

The company in focus is Coty Inc. (COTY), a struggling fragrance and cosmetic enterprise that has embarked on a major turnaround campaign.

Although Coty is the world’s No. 1 fragrance company, that status has not prevented the company’s stock from slumping ~53% over the last five years.

But a reversal of fortunes appears to be underway, thanks mostly to the newly installed CEO, Sue Nabi, a 28-year veteran of the beauty industry.

Her résumé features a string of successes at both L’Oréal and Lancôme. To top it all off, she cofounded Orveda, the thriving super-premium skincare brand.

Nabi hit the ground running at Coty in 2020 with a four-part plan to slash the New York-based company’s heavy debt load and to place the company on a new path of sustainable revenue and profit growth.

Anyone can talk the talk, of course. But Nabi and her team are demonstrating already that they can walk the walk.

Since this new group tool over the reins, the company’s debt load has dropped by 42%, from $8.2 billion to $4.8 billion. At the same time, several key product lines are showing signs of resurgent revenue growth.

As Coty’s turnaround become more a matter of fact than faith, investors will likely award its stock with a much higher price.

Risks remain, of course. But the company’s turnaround seems to have taken root… and as it blossoms, Coty should establish a strong, long-term growth trend.

Cheap Stock No. 3: International Game Technology PLC (IGT)

- 52-Week High/Low: $16.26–$32.95

The London-based International Game Technology PLC (IGT) offers products and services such as lottery management services, online and instant lottery systems, gaming systems, instant ticket printing, electronic gaming machines, sports betting, digital gaming, and commercial services.

The company works with governments and regulators in over 100 countries. While the stock is still relatively cheap, its value, according to Investors Observer, has risen 33.19% over the last year while the S&P 500 has gained only 0.89%.

IGT describes itself as “the world’s leading end-to-end gaming company.” In plain English, the company is the world’s largest provider of slot machines and other video gaming machines, as well as the world’s leading operator of lotteries.

But as the company’s name implies, IGT really provides the technology that drives gaming and lottery platforms. The guts of gaming systems.

Obviously, IGT is not the only company vying for a chunk of the sports betting bounty. Industry insiders have referred to the current activity in this sector as a “land rush” or a “gold rush.”

Lots of companies – large and small – are hoping to get a piece of the action, and lots of companies will. But IGT is uniquely positioned to gain critical footholds in most states, and then scale those footholds into significant profit growth.

IGT’s gaming revenues are very solid. The company maintains an installed base of nearly 23,000 slot and gaming machines.

And as other states approve online sports betting, IGT can expand its platform into those states as well.

Net-net, IGT is a market-leading provider of gaming and lottery systems. But it is now vying to become the market leader of sports betting systems in the U.S.

The company has all of its ducks in a row, both strategically and technologically, which is why we expect it to achieve major success in the budding U.S. sports betting industry.

Cheap Stock No. 4: Nokia Corp. (NOK)

- 52-Week High/Low: $4.17–$6.40

In 2030, the idea of investing in Nokia Corp. (NOK) may seem like the most obvious investment anyone could have ever made. But in the here and now, the stock seems like nothing more than a perpetual loser… a stock market has-been.

Its dismal history is probably a big reason investors have been hesitant to embrace the stock now, even though the company is on the verge of what will probably become a multiyear phase of explosive growth, thanks to 5G.

The global 5G rollout is providing a truly enormous investment opportunity that will enrich millions of investors along the way.

The United States, the European Union, and several other countries have taken decisive new steps to shift supply chains from China to domestic companies, or at least non-Chinese companies.

Now that Huawei has become an outcast in the United States because of its alleged spying activities on behalf of the Chinese government, Nokia is another competitor set to benefit from its banishment.

And the company is wasting no time capitalizing on Huawei’s retreat. Nokia has already landed 160 commercial 5G deals and 63 live 5G network deployments. And if paid trials were added to the mix, the number of total 5G agreements would exceed 220.

Meanwhile, the company possesses a kind of “secret weapon” that attracts little attention from investors: a lucrative and growing patent portfolio.

This portfolio throws off more than $1.5 billion a year in licensing revenue. Because most of that revenue flows directly to the bottom line as net profit, it provides Nokia with steady, robust cash flow.

In fact, this source of income is so substantial that it has totaled more than twice the entire company’s net income during the last six years. Intriguingly, this line item on Nokia’s income statement, called “Nokia Technologies,” is likely to grow considerably over the next few years, thanks to new licensing deals.

Cheap Stock No. 5: Sonos Inc. (SONO)

- 52-Week High/Low: $21.46–$43.39

If your household is one of the 9 million that contains a Sonos speaker, you probably understand one major reason to buy the company’s stock: Sonos Inc. (SONO) makes great products.

For those who aren’t familiar with the company, Sonos doesn’t simply make audio speakers. It literally invented multiroom home audio technology and holds more than 500 patents related to this technology.

This Santa Barbara, California-based company designs, develops, and produces audio products like wireless speakers, charging cradles, and music players. Its wireless speakers can integrate with multiple audio platforms like Apple Music, Spotify, and Pandora, and can operate seamlessly throughout every room in the house.

Nevertheless, producing a popular consumer product never guarantees long-term success. Many times, a popular product becomes a flash-in-the-pan fad that flames out after a few years. Or sometimes, hot products succumb to competition.

But Sonos speakers do not seem to be a fad, and the company has successfully thwarted intense competition. The company has consistently innovated and enhanced its product offerings and platform to strengthen its leadership position.

As company CEO Patrick Spence said, “The quality of our products across design, ease of use, sound quality, the openness of our platform, and the premium positioning our brand drives growth in purchases by both new and existing customers.”

As a result of its success, the company announced another strong annual performance two days ago.

Specifically, Sonos delivered its third straight year of double-digit revenue growth and third straight year of 20%-plus bottom-line growth. As a result, the company’s free cash flow is trending sharply higher, as is the net cash on its balance sheet.

The company’s strengthening financial performance is the direct result of its marketing success. During the last 12 months, 1.7 million new households purchased at least one Sonos product – bringing the total to nine million households.

That number illustrates the growing popularity of the Sonos audio platform. But it also provides a glimpse into the company’s massive growth potential.

Less than 7% of U.S. households own a Sonos product. Therefore, the company could double its consumer base by penetrating just 14% of U.S. households. Furthermore, the longer a household remains a Sonos customer, the more products it tends to buy.

Summing Up

We’re so glad that you decided to further your journey to wealth by joining Smart Money.

While these five “cheap” stocks are sure to fortify your portfolio in 2022 and beyond, those aren’t the only benefits of this free e-letter…

Nearly every Tuesday, Thursday, and Saturday, you’ll receive an email from Eric Fry, wherein he’ll share his insights on the latest market “megatrends,” how to hedge against inflation, which stocks you should avoid, and more.

Get started by visiting your Smart Money website here.

Of course, there’s a good chance that not all five of these “cheap” stocks will end up winners. Every investor will suffer losses from time to time. That’s inevitable.

But we have hopefully minimized your risk of loss – and maximized your opportunity for gains – with these carefully selected prospective investments…

Even when a market crash may seem possible.

These are the times to heed the advice of Rudyard Kipling…

“Keep your head when all about you are losing theirs.”

Regards,

Dave Gilbert

Editor, Smart Money