Growth stocks have been on a wild ride for the past few years. The pandemic sent many soaring to unbelievable heights. Then, rising rates and recession fears brought them crashing back to earth. But I believe the growth stock story is far from over. In fact, with the Fed now signaling rate cuts are on the horizon, I think growth stocks are poised for an epic comeback.

Sure, many growth names are still quite risky. Chasing the latest meme stock or unproven biotech is a good way to lose your shirt. However, for investors with a long-term mindset, now is the perfect time to start building positions in high-quality growth stocks.

As rates come down and the economy stabilizes, these businesses could deliver explosive returns. I wouldn’t be surprised to see some of the best growth stocks 5X or more in value over the next five years. Of course, you have to be selective and manage your risk. But if you’re aiming for outsized gains, having some exposure to growth is a must. Here are seven growth stocks that have the potential to be mega-winners.

Cadeler (CDLR)

Cadeler (NYSE:CDLR) installs and maintains offshore wind farms with its fleet of specialized vessels. These massive turbines out at sea generate more consistent power than their land-based counterparts without noise complaints. Cadeler seems perfectly positioned to ride this wave of clean energy expansion.

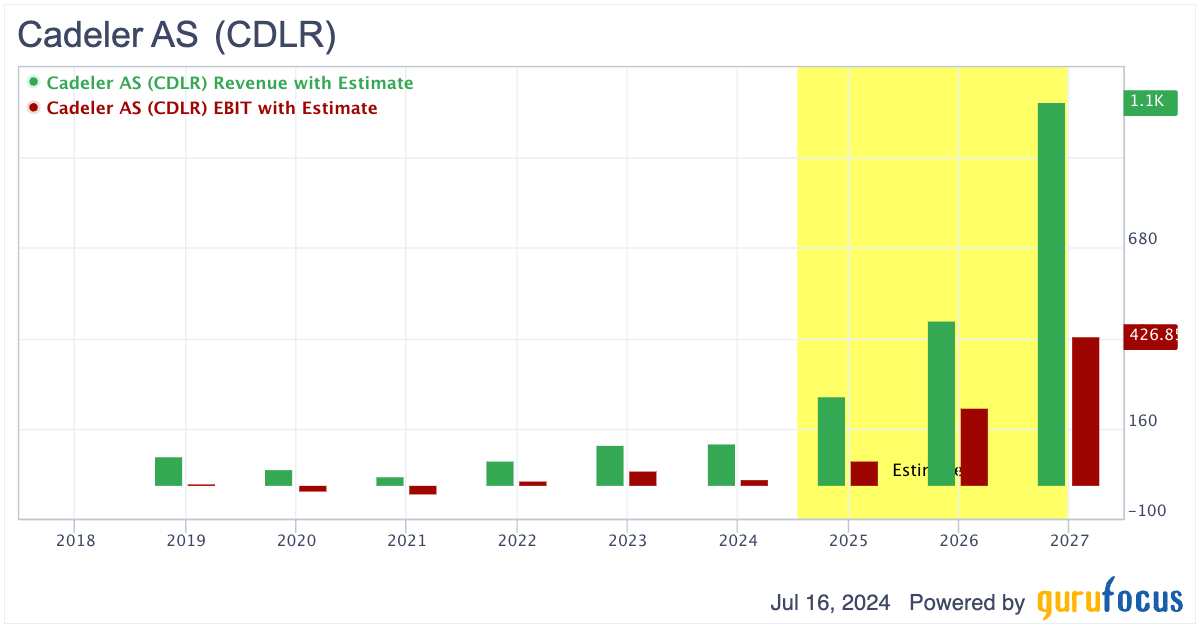

Analysts project the company’s revenue to surge from $255 million in 2024 to over $1 billion by 2027. Earnings per share is expected to skyrocket from just 20 cents to $1.86 in that same period. With numbers like these, I wouldn’t be surprised to see Cadeler’s stock deliver 5x returns or more.

Click to Enlarge

The company keeps racking up new contracts, too. They recently inked a deal with Orsted (OTCMKTS:DNNGY) for a long-term vessel lease starting in 2027.

Of course, I have to temper my enthusiasm with a dose of realism. Cadeler operates in a capital-intensive industry with plenty of risks. Weather delays, project cancellations, or new competitors could throw a wrench in their plans. But from where I’m sitting, the potential rewards far outweigh the risks for this offshore wind pure-play.

Megaport (MGPPF)

Megaport (OTCMKTS:MGPPF) operates a global software-defined network platform that enables businesses to connect their networks to cloud services and data centers. Thanks to the AI revolution, the data center industry is booming and this trend will only accelerate in the coming years. Megaport is perfectly positioned to ride this wave of growth.

Megaport reported impressive numbers. Revenue increased 30% year-over-year to 49.5 million AUD, while EBITDA nearly doubled to 14 million AUD. The company also upgraded its full-year EBITDA guidance.

Despite these strong results, Megaport’s stock price took a hit recently. Regardless, this company is profitable and growing rapidly, with plenty of runway ahead as the data center and AI industries continue to expand.

Sure, there are risks to consider. Megaport’s success hinges on sustained growth in AI and data center demand. But given the massive investments pouring into these sectors, I’m optimistic about the company’s prospects.

Ouster (OUST)

Ouster (NYSE:OUST) makes high-resolution digital lidar sensors for autonomous vehicles, robotics and smart infrastructure. This company is poised to ride the massive robotics and automation adoption wave in the coming years. The lidar industry could surge as companies across sectors embrace these technologies, and Ouster seems uniquely positioned to capitalize. Their recent financial performance has been stellar compared to lidar peers. It is still unprofitable, but analysts project Ouster could reach profitability by 2027 with significant growth after that. If analyst estimates pan out, you’re looking at just 3x 2027 earnings at current prices.

Of course, it’s speculative at this stage. But I see multibagger potential here if robotics continues its exponential growth and EVs come back with increased lidar usage. The stock has surged lately on strong Q1 results, with revenue up 51% year-over-year to $26 million. Several analysts have boosted price targets, including Craig-Hallum to $13 and Rosenblatt to $17.

ClearPoint Neuro (CLPT)

ClearPoint Neuro (NASDAQ:CLPT) makes platforms for performing minimally invasive surgical procedures in the brain. CLPT stock has surged about 40% in the past two weeks and could climb even higher if the company maintains its growth trajectory and continues making medical breakthroughs.

While I typically steer clear of small biotech firms, I think it is worth considering CLPT. I’m personally quite bullish on gene-editing companies. These cutting-edge businesses have the potential to cure a wide array of diseases and boast extensive pipelines. This optimism extends to ClearPoint Neuro as well.

In Q1, revenue rose 41% year-over-year to $7.6 million. That’s not too bad, considering this top-line number beat estimates by 9.23%. It still trades at quite a steep sales premium, but I see multiple catalysts on the horizon that could keep sales growing fast.

Cash is also one of the most important metrics for an unprofitable biotech company. This company’s cash holdings are around $35 million, which is satisfactory considering its $4.15 million in net losses in Q1.

Block (SQ)

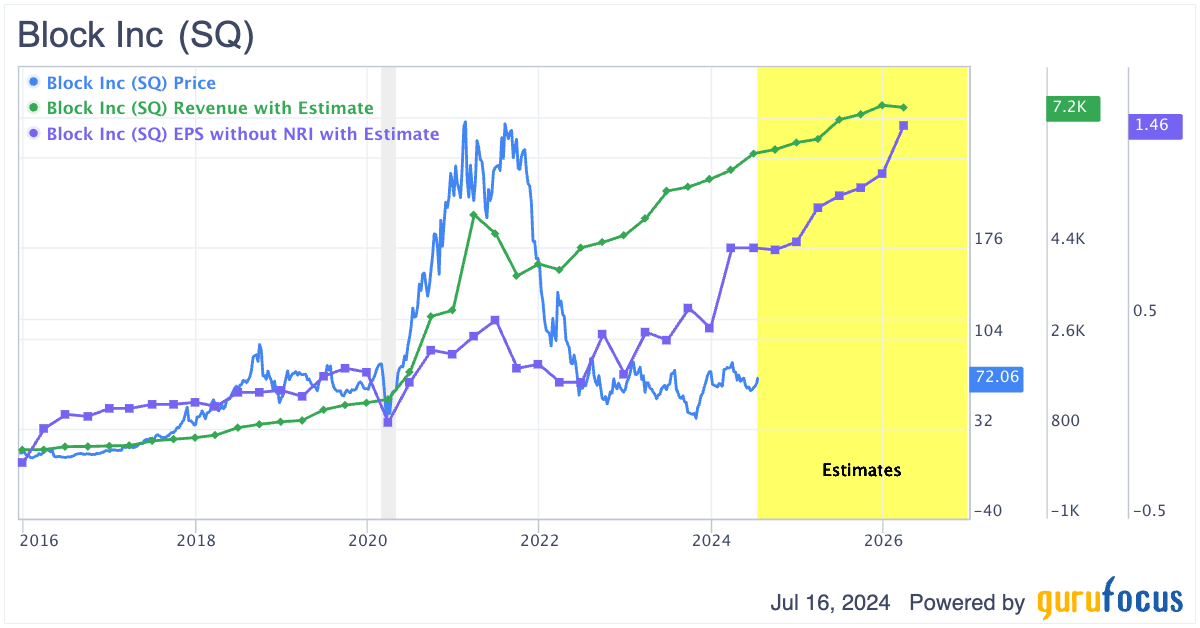

Block (NYSE:SQ) is much more than just a PayPal (NASDAQ:PYPL) alternative as it has been in the past. It has delivered impressive financial results recently, with Q1 2024 revenue of $5.96 billion beating estimates and adjusted EPS of 85 cents, surpassing expectations. Block raised its full-year 2024 guidance, now expecting gross profit of at least $8.78 billion (17% growth) and adjusted operating income of at least $1.3 billion. If we look at fundamentals, this stock should’ve recovered to around $100 many months ago, but the broader fintech industry has not been cooperating.

Click to Enlarge

That said, analysts are now projecting EPS to increase from $3.4 in 2024 to $15 by 2033 — and it is expected to double from 2024 by 2028. Block’s stock has been trading sideways at a discounted level due to the depressed fintech sector; rising EPS should lead to an eventual breakout.

Moreover, impending interest rate cuts could also catalyze a major rally for Block. Block could deliver 5x returns in five years if the market fully appreciates its profitable growth. Management would need to surpass those optimistic EPS expectations I mentioned above. Can they do it? That’s for you to bet on.

Fastly (FSLY)

Fastly (NYSE:FSLY) operates a content delivery network that enables faster and more reliable delivery of digital content. Fastly is an exciting bet on the future of cloud computing, edge computing and streaming over the next five years. Yes, the stock has plummeted nearly 58% in the past year amid concerns over slowing growth and mounting losses. However, shares have stabilized recently, and Fastly could deliver outsized returns.

Analysts seem cautiously optimistic, with an average price target of $9.8, implying a 29% upside from current levels. The company also reported solid Q1 results, with revenue up 14% year-over-year to $133.5 million, beating estimates.

Looking ahead, Fastly is expected to turn profitable in 2025. You are currently paying just four times 2030 earnings, though I will warn again that these estimates are very speculative.

Regardless, the risk-reward looks favorable for people willing to ride out the volatility. Cloud and edge computing are clear megatrends that should provide strong long-term tailwinds for Fastly’s business.

freee K.K. (FREKF)

freee K.K. (OTCMKTS:FREKF) specializes in delivering cloud-based accounting and HR software solutions to small and medium-sized businesses in Japan. This company is poised for hypergrowth as more Japanese companies rush to digitize their back-office operations. In fact, freee’s revenue surged 31% year-over-year to 6.65 billion Yen in Q1 2024.

Despite this impressive performance, freee’s stock is still down nearly 78% from its all-time high. A weakening Japanese Yen has been a headwind for the company. However, I think the worst may be over for the stock. As global interest rates stabilize and the Yen potentially recovers, investor sentiment toward Japanese equities could improve.

Japan is finally ending its negative interest rate policy, and I expect the macroeconomic environment to become more favorable for growth stocks like freee.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.