As the summer of 2024 heats up, so does my excitement for under-$10 stocks. I believe these affordable picks strike a sweet spot between volatility and medium-term potential. Sure, penny stocks and most sub-$10 shares often get lumped together, and for good reason – many smaller companies have struggled in the market despite the broader rally. However, these budget-friendly stocks are still worth a closer look.

Why? They offer an enticing balance of risk and reward. Plus, as interest rates inevitably cool off in the coming quarters, it could be just the catalyst needed to push these stocks to new heights. I’m not saying it’ll be a smooth ride, but for those willing to buckle up, the potential payoff could be well worth it. Let’s take a look!

Udemy (UDMY)

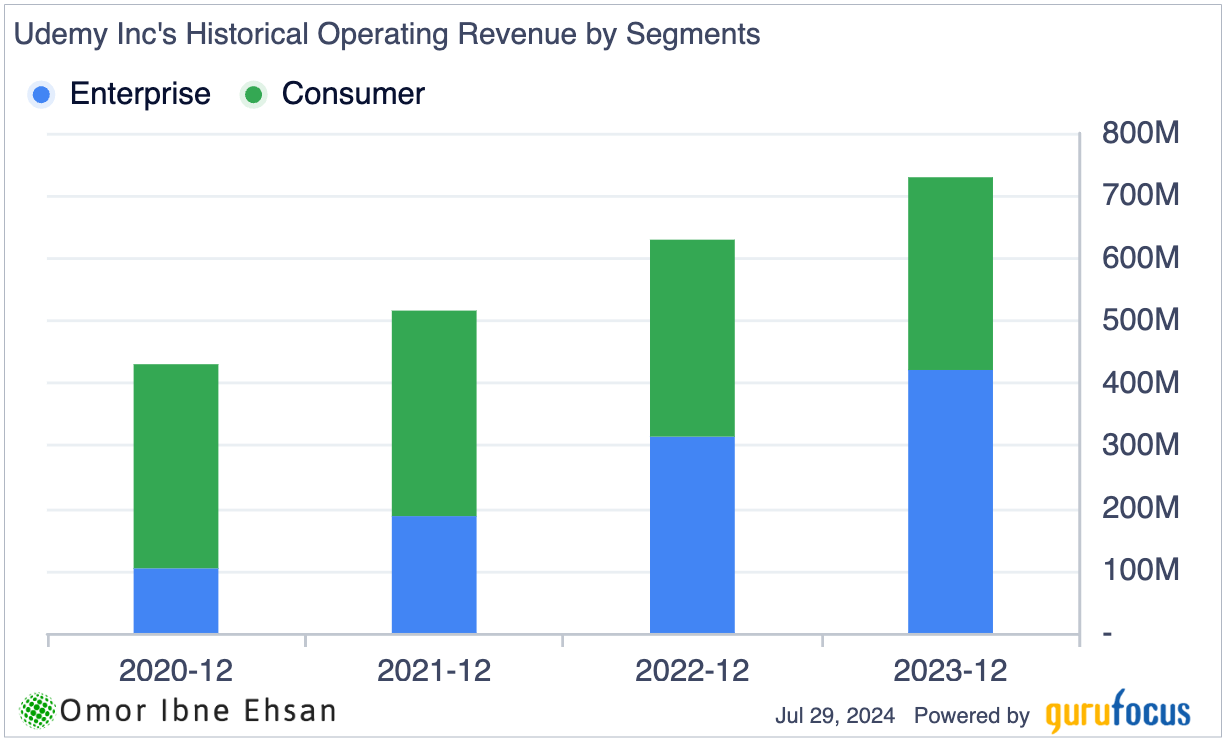

Udemy (NASDAQ:UDMY) is an online learning platform that offers courses in various fields to over 64 million learners worldwide. The company recently reported strong first-quarter 2024 results, with 24% year-over-year revenue growth in its Business segment and expansion to over 16,000 enterprise customers globally. This is the biggest segment now, as the Consumer segment has been declining.

Click to Enlarge

I believe Udemy is well-positioned for long-term success as demand for online learning and upskilling continues. Analysts seem bullish on Udemy’s prospects, with firms like Keybanc, Cantor Fitzgerald, and Needham maintaining positive ratings and price targets indicating significant upside. Cantor Fitzgerald’s Brett Knoblauch reiterated an Overweight rating with a $20 price target, implying a 122% upside from current levels. While I’m encouraged by the optimism, I would caution that such a lofty target may be overly ambitious in the near term.

That said, with Udemy guiding for profitability in 2024 and analysts projecting 54 cents in earnings per share in 2026, the current valuation of under 17x 2026 earnings looks quite reasonable for a high-growth software name. If Udemy executes well, there could still be plenty of room for upside.

Taboola.com (TBLA)

Taboola (NASDAQ:TBLA) is an advertising technology company that provides content recommendation services. The company has been navigating a challenging environment, but I believe it is well-positioned to benefit from the accelerating shift of advertising dollars to digital channels.

In today’s world, content consumption is increasingly moving online. People are spending more time than ever watching videos, reading articles and otherwise engaging with digital media. Naturally, advertisers are following suit by allocating larger portions of their budgets to online channels and sponsored content. This mega trend plays right into Taboola’s wheelhouse. Despite near-term headwinds, Taboola delivered solid Q1 2024 results, beating the high end of its guidance across all key metrics.

Revenues grew 26% year-over-year to $414 million, while ex-TAC gross profit increased 20% to $139 million. The company is making good progress on strategic priorities like ramping up its Yahoo partnership and driving advertiser success through AI-powered tools. The expected growth in the coming years is very promising, too.

Taboola’s stock has been flat over the past year and is down 17.6% year-to-date, but I view this as an attractive entry point.

Kinross Gold (KGC)

Kinross Gold Corporation (NYSE:KGC), a Canadian-based gold mining company, has been striking it rich thanks to soaring gold prices. With economic uncertainty driving investors towards safe havens like gold, Kinross has seen its stock rise by 77% over the past year.

The company posted strong Q1 2024 results, with margins jumping 20% to $1,088 per ounce sold. The analyst consensus is bullish, but bears argue the stock may be getting ahead of itself. Personally, I’m in the bull camp and believe gold prices have room to run.

Kinross is making smart moves, like investing in the promising Manh Choh project in Alaska. The company also published an impressive sustainability report to boost ESG.

Regardless, Kinross’ fortunes are closely tied to the price of gold. If the yellow metal loses its luster, expect KGC shares to follow suit. But for now, I’m excited to see how this gold rush plays out. With Q2 results due out soon, Kinross investors could be in for another pleasant surprise.

Aware (AWRE)

Aware (NASDAQ:AWRE) receives limited analyst coverage, but those who follow it see long-term potential due to the increasing global need for secure biometric solutions. Craig-Hallum analyst Jeff Van Rhee recently reiterated his “Buy” rating on Aware.

However, Aware’s financial performance has been volatile, and the company is still unprofitable. In Q1 2024, Aware reported a 3% year-over-year increase in revenue to $4.4 million, while its net loss improved to $1.0 million from $1.6 million in the prior year period. I believe that if Aware continues to execute on its strategy, it could reach profitability in the near future.

The rise of AI could disrupt many existing verification systems, potentially driving companies to rapidly adopt more advanced biometric solutions. This trend could benefit Aware as businesses turn to the company’s expertise in biometric software.

UP Fintech Holding (TIGR)

UP Fintech Holding (NASDAQ:TIGR) operates an online brokerage platform focusing on global Chinese investors. The company has faced challenges in recent years, with its stock price down significantly from 2021 highs and trading mostly below $5 for over two years now.

However, I believe UP Fintech is starting to turn things around financially and could deliver solid upside if it maintains its current trajectory. While the stock is flat year-to-date, I expect positive moves going forward as the company reported total revenue of $78.9 million in Q1 2024, a 19% increase year-over-year. Both GAAP and non-GAAP net income also saw significant growth.

Of course, skepticism still abounds regarding the Chinese economy, but I don’t necessarily view that as a negative for UP Fintech. As the “largest online broker focusing on global Chinese investors in terms of U.S. securities trading volume,” the company could actually benefit from Chinese investors increasingly looking abroad amidst a poorly performing Hang Seng Index.

Red Cat Holdings (RCAT)

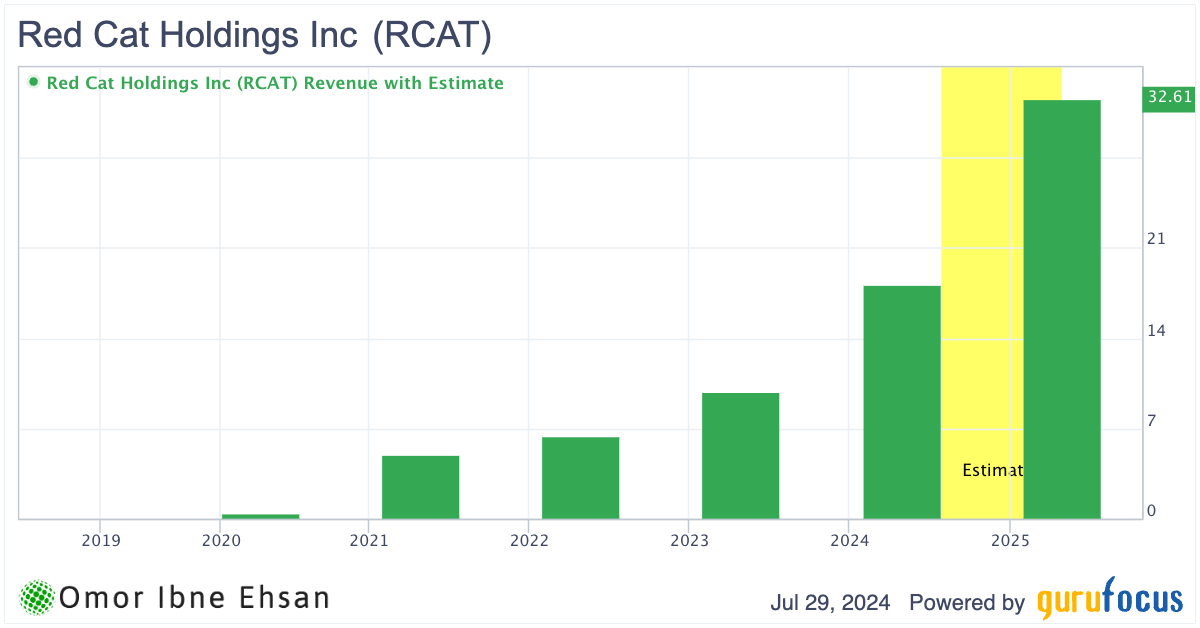

Red Cat Holdings (NSADAQ:RCAT) is a small drone drone startup. The company recently reported revenue of $5.8 million in fiscal Q3 2024, representing 250% year-over-year increase and marking the third consecutive quarter of double-digit sequential growth. The growth ahead looks solid, too.

Click to Enlarge

In my view, Red Cat is a risky but intriguing investment for those seeking significant upside potential. This small drone player could hit pay dirt by landing hefty contracts as unmanned aerial vehicles gain popularity with government and military customers. After all, drones are already heavily utilized by law enforcement, and the Pentagon is just beginning to ramp up its drone deployments.

Red Cat aims to replicate that manufacturing capability domestically, and I believe it could soar if successful. The company also recently secured $4.4 million in non-dilutive financing and is poised to join the Russell Microcap Index.

Analysts seem bullish on Red Cat, with Ladenburg Thalmann initiating coverage in June with a “Buy” rating and $4 price target, implying over 75% upside from here.

PowerFleet (AIOT)

PowerFleet (NASDAQ:AIOT) provides IoT and AI solutions to optimize logistics operations. The company has been pivoting to a SaaS-centric business model centered around its Unity platform.

I believe PowerFleet is well-positioned to benefit from the rapid digitization of the logistics industry. Companies are investing heavily in AI and software to maximize supply chain efficiency, and PowerFleet’s device-agnostic Unity platform puts it in the sweet spot of this trend.

The market seems to be recognizing PowerFleet’s potential. The stock has surged 76% over the past year as the company’s recurring SaaS revenue gains traction. However, it still trades 42% below pre-pandemic levels.

Analysts are overwhelmingly bullish, with all six covering the stock rating it a “Buy.” Canaccord Genuity nearly doubled its price target to $10, implying a 110% upside. While I’m not quite that optimistic, I agree PowerFleet’s valuation doesn’t reflect its growth prospects in a booming industry.

On Penny Stocks and Low-Volume Stocks: With only the rarest exceptions, InvestorPlace does not publish commentary about companies that have a market cap of less than $100 million or trade less than 100,000 shares each day. That’s because these “penny stocks” are frequently the playground for scam artists and market manipulators. If we ever do publish commentary on a low-volume stock that may be affected by our commentary, we demand that InvestorPlace.com’s writers disclose this fact and warn readers of the risks.

Read More: Penny Stocks — How to Profit Without Getting Scammed

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.