If you’re looking for signs of what’s next for the economy, look no further than the checkout aisle.

Because of the government shutdown, we have still not received a retail-sales report since September 16 – which provided us with data for August.

That data gap leaves investors flying partially blind at a moment when questions about the strength of the U.S. consumer are growing louder.

What’s more, it leaves the Federal Reserve without crucial data it needs to continue lowering key interest rates.

In this kind of murky backdrop, earnings season steps in.

In uncertain environments like this, where talk of a “K-shaped” economy is growing louder, results from consumer-driven retail names often reveal what economic indicators can’t: who’s adapting and who’s losing momentum.

For retail specifically, this means that higher-income shoppers continue spending, while lower- and middle-income households pull back.

And as you’ll see in a moment, the retailers positioned on the right side of that divide are separating from those caught in the middle.

This week, we got results from two major retailers: Target Corporation (TGT) and Walmart Inc. (WMT).

So, in today’s Market 360, I’ll review both companies’ results and tell you which one is the better buy according to Stock Grader. Then, I’ll explain why being selective in your stocks is more important than ever right now.

Target

Target reported its third-quarter earnings before the bell on Wednesday morning. It reported adjusted earnings per share of $1.78, narrowly beating expectations of $1.72. Net revenue declined 1.5% year-over-year to $25.27 billion, slightly below expectations of $25.32 billion.

That revenue weakness continues a much longer trend: Target has now posted roughly three years – 12 straight quarters – of flat or negative sales. Ouch.

In a normal economy, that would be concerning. In a K-shaped one, it’s a major warning sign that Target’s strategy simply isn’t matching what shoppers want.

What stood out were the strategic shifts. Target is increasing capital expenditures by 25% to $5 billion, even as it plans to cut 1,800 jobs. It also announced a leadership change, with current COO Michael Fiddelke stepping in as CEO in 2026, replacing Brian Cornell.

In a notable tech move, Target is preparing to launch a beta experience with OpenAI, allowing customers to use ChatGPT within its app for shopping purposes.

But these investments are happening at the exact moment Target’s customers are shifting to lower-priced alternatives, such as Amazon.com, Inc. (AMZN), The TJX Companies, Inc. (TJX) – and, yes, Walmart.

Company management has lowered its full-year profit guidance, now expecting full-year adjusted earnings per share between $7.00 and $7.50. Its previous guidance was $7.75 to $8.25. The company also maintained its expectation for a low single-digit decline in sales for the fourth quarter.

Chief Commercial Officer Rick Gomez struck a cautious tone heading into the holiday season during the earnings call Wednesday morning, saying shoppers are focusing on “what goes under the tree versus what goes on the tree.”

Translation: Even during the peak retail period, shoppers are focusing on essentials and gifts, not décor or home items – which are one of Target’s key calling cards. Not a good sign, folks.

Walmart

Now, let’s turn to Walmart.

On Thursday morning, Walmart reported third-quarter earnings per share of $0.62, just above analysts’ expectations for $0.60. Revenue rose 6% year-over-year to $179.5 billion, also above expectations for $177.6 billion.

Walmart also surpassed expectations with its same-store U.S. sales, rising 4.5%, which exceeded the expected 4% rise. It also reported a 1.8% rise in foot traffic and a 2.7% rise in the average ticket at U.S. stores.

Looking ahead, Walmart has raised its guidance for the fiscal year, stating that it now expects net sales to increase 4.8% to 5.1%. The previous guidance was 3.75% to 4.75%.

One of the most impressive highlights was Walmart’s 27% surge in global online sales – a sign that its digital investments, logistics upgrades and automation strategy are paying off. This kind of execution has helped Walmart succeed across income levels, even as lower-income shoppers cut back.

See, unlike Target, Walmart is benefiting from both ends of the K-shaped economy. Budget-stretched consumers continue to rely on Walmart for essentials, while higher-income households are trading down to Walmart for value on their bigger-ticket items.

That shift is becoming a major growth engine. I should also add that Walmart has managed tariff pressures far better than its peers. This discipline helped Walmart avoid the margin hit that led Target to cut guidance.

Furthermore, a technological transformation is happening behind the scenes. Aside from the incredible online sales growth fueled by its Walmart+ membership app, it’s notable that the company’s advertising business grew 53% year-over-year. And through a new partnership with OpenAI, Walmart and Sam’s Club members can now reorder groceries directly through ChatGPT.

Overall, the company’s goal is to change the way you shop online – from a traditional search-and-scroll model to a personalized, conversational interaction.

Increasingly, the company is becoming one of the most tech-forward retailers in the business.

It’s no wonder, then, that shares of Walmart jumped 6% after the market closed on Thursday.

The Better Buy to Put in the Check Out Aisle

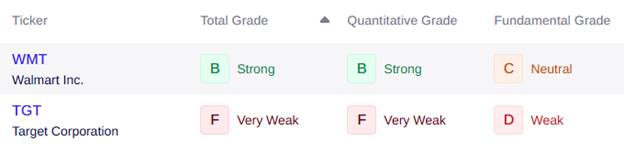

Now that we’ve reviewed the numbers, which company is the better buy? Let’s take a look at what my Stock Grader (subscription required) has to say…

Based on these results, Walmart is the clear winner. It earns a solid Quantitative Grade of B, a Fundamental Grade of C, giving it a Total Grade of B. This signals that the stock is “Strong.”

Target, on the other hand, receives poor marks across the board, with a Quantitative Grade of F, a Fundamental Grade of D and a Total Grade of F, making it “Very Weak.”

The divergence makes perfect sense when you consider the differences in execution I noted earlier.

Walmart has earnings momentum, digital acceleration and market-share gains across income levels. Target has declining traffic, heavier exposure to discretionary categories, strategic inconsistency and no clear catalyst.

But the real takeaway here is bigger than just one stock…

What to Focus On

These results highlight a broader truth: This is a stock picker’s market, folks.

Walmart vs. Target is a textbook example. There’s no rising tide lifting every retailer. There’s a widening gap between companies that are adapting to consumer behavior, pricing pressures and AI-driven operational changes – and those that aren’t.

Because the divide between the “haves” and “have nots” – and the “good stocks” and “bad stocks” – isn’t going away anytime soon. If anything, it will accelerate in the age of the Economic Singularity…

This is the next great phase of AI-driven disruption. It’s when AI becomes the central engine of productivity, growth and innovation across every major sector.

Walmart’s own evolution shows what this future looks like. AI is no longer a side story… It is THE story. And the companies embracing it fastest are pulling away from the pack.

So, what does that mean for you?

It means focusing on fundamentally superior companies is now more important than ever.

That’s why I recently put together a special report, where I identify seven fundamentally superior companies in the heart of this sea change that are poised to deliver extraordinary returns in the years ahead.

Sincerely,

Louis Navellier

Editor, Market 360

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

Walmart Inc. (WMT)