Even before the novel coronavirus came through, CrowdStrike (NASDAQ:CRWD) was already under significant pressure. CRWD stock hit its 2020 high on Feb. 19 just like the S&P 500. However, shares were still down more than 33% from its 52-week high at that point.

While shares were then crushed lower amid the coronavirus selloff, we’ve seen a robust rebound in CrowdStrike.

Shares have not only recouped all of the losses from the February high, but have actually made new all-time highs earlier this month. Let’s look at three reasons bulls can continue to bet on CRWD stock.

Coronavirus as a Catalyst

What propelled CRWD stock to new highs earlier this month? It was the company’s better-than-expected earnings results. Of course, it helped that the overall market has been in a strong uptrend too.

CrowdStrike earned 2 cents per share in the quarter, 8 cents better than expected as analysts were looking for a loss in the quarter. Revenue of $178.1 million grew more than 85% year-over-year and beat expectations by $12.7 million.

Here’s the kicker. CrowdStrike didn’t just deliver a beat-and-beat, it raised its guidance as well. In short, the company is seeing increasing demand for its cybersecurity products as Covid-19 forces more work-from-home and online work scenarios. From management’s release (bold emphasis added):

CrowdStrike finished the quarter with strong momentum and delivered results that exceeded our expectations across the board … Cybersecurity is mission critical and in the quarter our customers continued to prioritize their cybersecurity investments. With both security administrators and end-users working from home, we believe the rapid shift to a remote workforce has helped increase our leadership.

At a time where most companies are starving for growth or saw a large decrease in revenue and cash flow, CrowdStrike is seeing an inflow of business.

Growth Is Very Strong

Analysts expect full-year revenue growth of 60% to $770.5 million this year. However, they expect that rate to slow notably, down to about 32% growth in fiscal 2022 (next year). Although, they expect the company to generate just over $1 billion in sales that year.

One downside here is valuation, with CrowdStrike stock commanding a $20 billion market cap. Trading at roughly 20 times forward sales isn’t cheap, but for such strong growth — particularly in a period where many companies have no growth — growth investors are willing to pay a premium.

Given the growth the company is experiencing now, the secular demand for cybersecurity and the work-from-home trend, I would argue that estimates for fiscal 2021 and 2022 may be conservative. CrowdStrike isn’t just leaching off Covid-19 either, its products are high quality.

Just look at these notes from the release:

The CrowdStrike Falcon® endpoint protection platform was named a Leader in The Forrester Wave™: Enterprise Detection And Response, Q1 2020. CrowdStrike received the highest possible score in 11 criteria.

For the second consecutive year, CrowdStrike earned the highest overall rating among vendors named in 2020 Gartner Peer Insights Customers’ Choice for Endpoint Detection and Response (EDR) with an overall rating of 4.9 out of 5 from 106 verified customer reviews.

Analysts still expect the company to lose money this year, but just 4 cents per share. Remember, they were looking for a loss of 6 cents per share last quarter and CRWD turned in a profit, so maybe it can swing to profitability for the year, too.

Finally, I’ll just leave this here: CRWD is now free cash flow positive, has $1 billion in cash on hand and just $32 million in long-term debt.

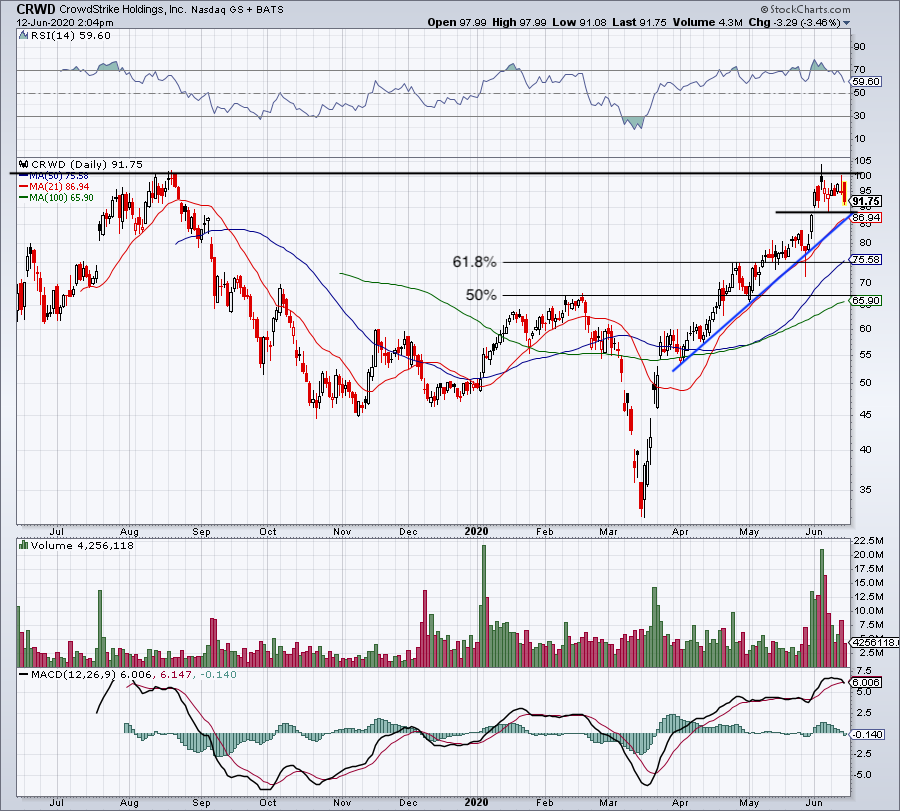

CRWD Stock Has Strong Technicals

Click to Enlarge

For a quick recap, we have a company with strong growth and break-even profitability trending in the right direction. The business is generating positive cash flow, has virtually no long-term debt, and more than $1 billion on its balance sheet. Lastly, it’s excelling, not losing momentum during the coronavirus outbreak.

The technical picture is the cherry on top — but it’s also the most vulnerable.

Unlike the business, which may hold steady or even pick up steam amid rising coronavirus numbers, the stock price may not be able to weather a selloff. While CRWD stock has proven to be a coronavirus play, a deep selloff will likely drag the stock down.

The silver lining to that is, a pullback would be a solid buying opportunity for investors. Let’s see if CrowdStrike holds $87. Below puts the 50-day moving average in play. Over $87 and $100-plus remains on the table.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.