Adobe Systems (NASDAQ:ADBE) is one of the names that should be on investors’ watch list as they look to buy the dip in tech stocks. While many focus on the larger tech stocks out there, ADBE stock has quietly had a stellar run of its own.

From the March low to the recent high, shares have climbed 110%. However, the stock is getting caught up in the tech selloff that started last week. From here, we simply have no idea what September, the fourth quarter, and the election will bring us.

Perhaps the tech dip is a short but viscous decline before resuming the trend higher. Maybe it will be an ugly and prolonged decline as investors look at risk-off avenues.

In either case though, Adobe should be on investors’ list of potential buys. Let’s look at why.

Breaking Down Adobe Stock

Adobe won’t report earnings until next week, on Sept 15. However, when the company reported in May, it showed solid growth.

Even though revenue slightly missed consensus estimates, sales still grew 14% year-over-year to $3.13 billion. Bottom-line profit of $2.45 per share beat estimates by 13 cents.

For the year, analysts expect 14% revenue growth in 2020 and 15% growth in 2021. That’s alongside 24% growth in earnings this year and expectations for 14% growth in 2021.

The above estimates — which may very well be conservative — highlight exactly why Adobe, and tech in general, is like cream rising to the top. So many other industries, like automotive, travel, leisure, parts of retail and dozens of other industries are struggling for growth.

Meanwhile, many names in tech — like Adobe — continue to churn out growth with or without the novel coronavirus. This is not 1999. It is not 2008. This is a different economic disruption and the tech industry is not made up of fly-by-night names with poor revenue and weak balance sheets.

On the downside to last quarter’s report, guidance came up a little short of expectations. But we saw that in other cloud stocks too and many of these companies blew estimates out of the water in the most recent quarter. Can Adobe do the same thing when it reports?

I think it will tell a promising story. But more importantly, Adobe has long-term drivers behind it. Its subscription revenue has helped make its sales figures more consistent — which is important during volatile economic times such as these. However, the recent shift to online and work-from-home solutions should help drive Adobe’s business higher as Covid-19 continues to disrupt traditional workflow.

Bottom Line on ADBE Stock

Click to Enlarge

With net debt of just $1.07 billion, I’m not going to lose any sleep over Adobe’s balance sheet. In fact, given its $221 billion market capitalization, it has quite a bit of flexibility.

Between its balance sheet and subscription-based revenue, it should have investors’ attention. However, the fact that it even has growth means it can garner a premium valuation.

I have made the case ad nauseam at this point, which is that companies with dependable growth deserve a premium. In general, that rule of thumb is accepted in the investment community. But it’s even more true during uncertain times such as this.

In pre-coronavirus days, plenty of companies had growth, with many boasting above-average growth. In a post-coronavirus world, most do not have growth, let alone market-beating growth. Those that have the latter are worth a higher valuation than they previously garnered, thus the strong rally.

In any regard, ADBE stock fits the bill.

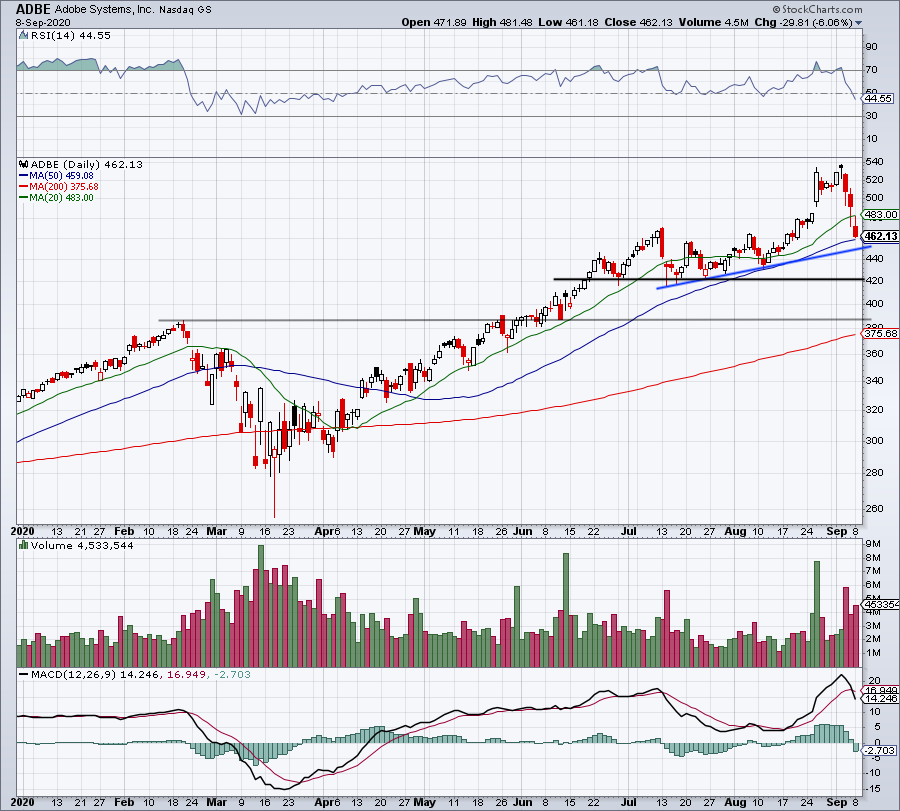

Four trading sessions ago, shares hit a new all-time high. Now the stock is down 14% and trading into its 50-day moving average. That’s a reasonable buying opportunity for investors.

That could set up ADBE stock for another move up through $500 and up toward its prior highs near $536. Should the stock take out its current highs, the 261.8% extension up near $600 will eventually be on the table — particularly if it has a positive reaction to earnings.

Either way, long-term buyers can still take advantage of market- or earnings-driven volatility. That comes in the form of buyable dips.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.