Hello, Reader.

Over the past several days, investors have been treated to endless variations of the chart below, regardless of their interest in oil markets.

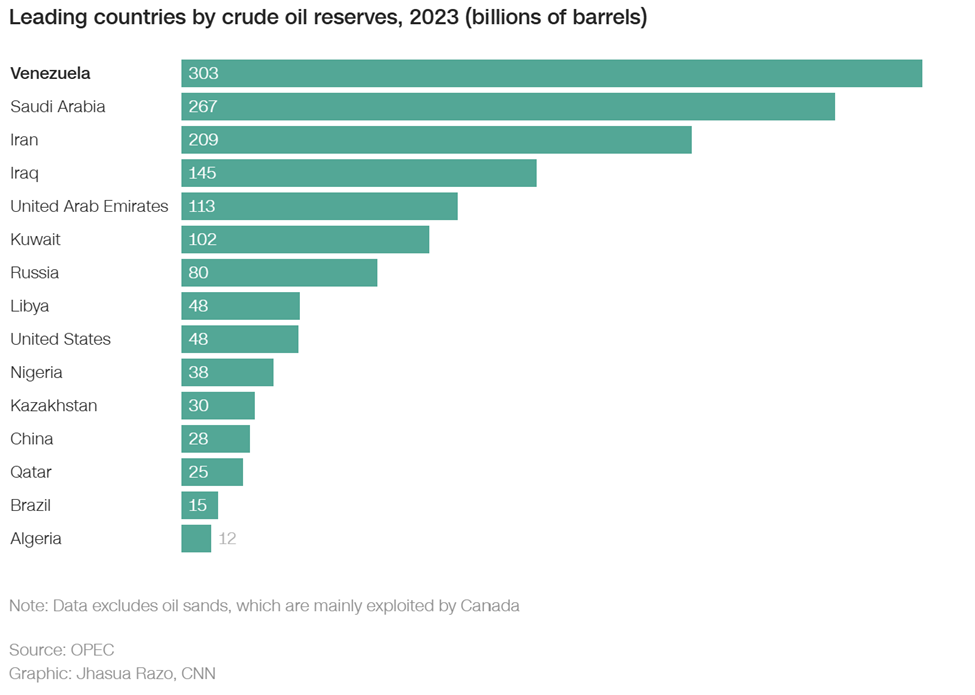

You see, Venezuela has the world’s largest oil reserves. And now, this past weekend’s geopolitical events seem to have a lot of investors salivating over these massive oil deposits. Shares of Chevron Corp. (CVX) –the sole American oil company still operating in the South American nation – spiked 6% earlier this week.

But the real story is more complicated.

So, in today’s Smart Money, I’d like to introduce three images – two charts and one map – that show why, even given the recent developments in Venezuela, I am not looking toward that country as an investment opportunity in oil.

Instead, my favorite bet on energy markets remains right here in the United States, specifically in the Permian Basin.

Let’s dive in…

Chart #1: American Versus Venezuelan Oil

One of the wonderful things about Permian Basin oil is that it’s considered “light.” There’s very little asphaltenes, heavy metals, or sulfur in the mix. Drillers essentially stick a bent straw into the ground, pump water and sand into the reservoir, and collect what comes back up.

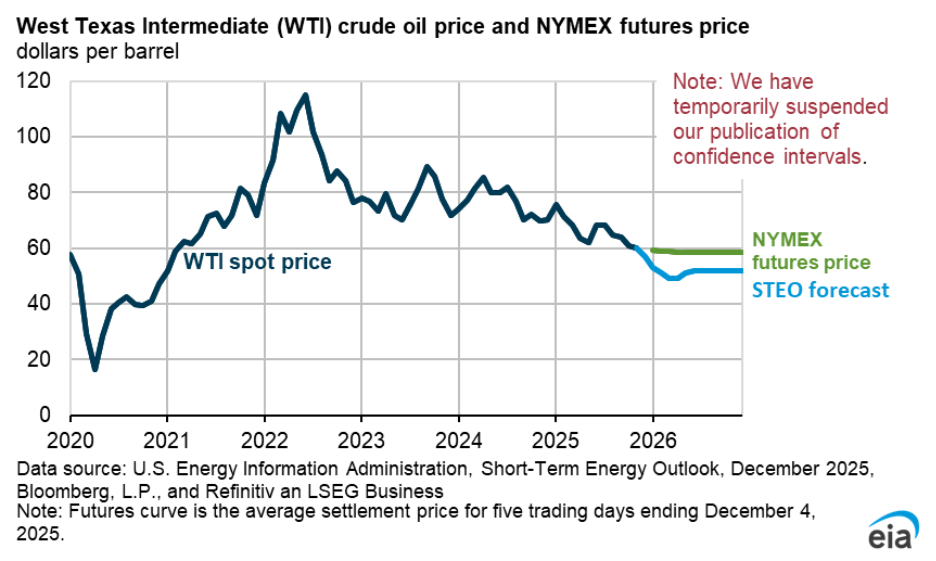

Most drillers (including one I recommend in Fry’s Investment Report) can do this for $12 per barrel or less. They’re printing money at current WTI crude oil prices of $57/barrel.

However, not every oil reserve is so easy to access.

Canadian oil sands contain so many asphalt-like contaminants that some deposits even require surface mining. (The sludge is mixed with hot water, and the bitumen is skimmed off the top.) Firms that own these unfortunate assets must spend between $20 to $40 to extract each barrel. Once you add in overhead costs, most Canadian oil sands firms are barely breaking even at current oil prices.

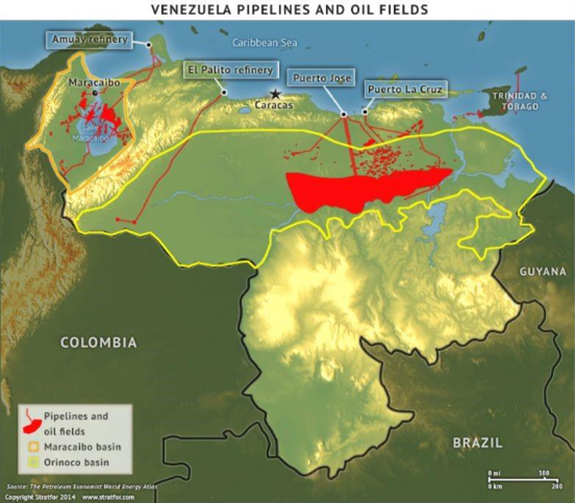

Venezuela’s oil reserves are in even worse shape. The table below lists several oil deposits in the country, the type of oil found in the reserves, and their current status…:

| Oil Deposit | What’s There | Status |

| Orinoco Oil Belt | Extra-heavy oil | Roughly 80% of Venezuela’s recoverable resources |

| Maracaibo Basin | Light to medium oil | Mature basin, but output has declined as fields run dry |

| Offshore | Mostly natural gas | Not particularly developed. |

By some estimates, oil would have to reach $80/barrel for new steam-assisted projects in the Orinoco belt to break even.

That’s a problem because futures markets currently expect the WTI oil benchmark to hover around $60 this year… and economists at the U.S. Energy Information Administration expect prices to fall to the low-$50 range.

That means any would-be driller stands to lose $20 to $30 for every barrel of Venezuelan oil it recovers.

Let’s take a look at that map…

Chart #2: Location, Location, Location

The second issue with Venezuelan oil is its geography… located smack in the middle of the country.

That makes it far trickier for energy firms to access, because these fields require access to pipeline infrastructure, road networks, and security guarantees.

In 2021, French oil major TotalEnergies SE (TTE) sold its remaining Venezuelan assets for an exceptional $1.38 billion loss after years of investment yielded little output. (At the time of sale, Venezuela made up less than 0.5% of TotalEnergies’ combined oil and gas production.)

That contrasts greatly with countries like Nigeria, Angola, and Guyana that have vast offshore oil and gas reserves. For these fields, energy firms can simply ship in supplies by boat and take out the oil via shuttle tankers. It’s noteworthy that TotalEnergies has now turned its attention to Mozambique… a fragile country that nevertheless allows for profitable oil and gas exploration because it’s offshore.

And last but not least…

Chart #3: Time Value of Money (and Oil)

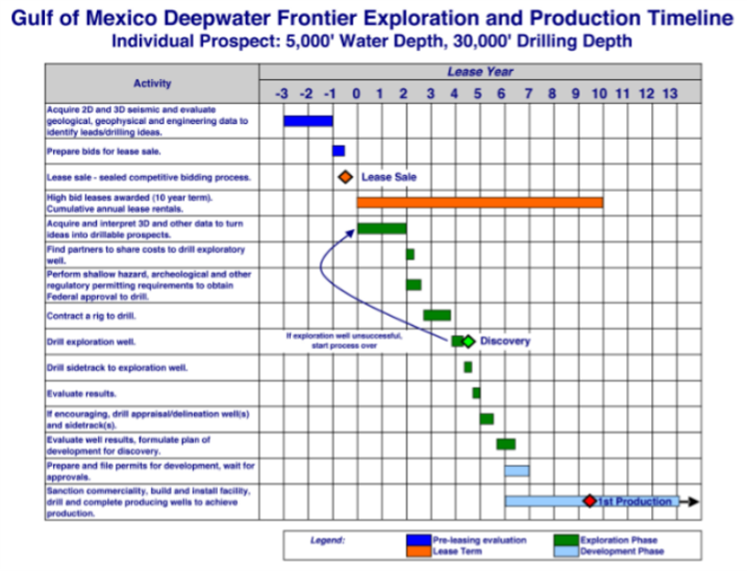

Finally, the issue with new oil wells is that it takes time to build them…

Not just weeks… or months…

But years.

Below is the third and final chart, which shows how long it takes to build a deepwater rig in the Gulf of Mexico… an area that’s already well explored. From initial lease to first production takes a full decade.

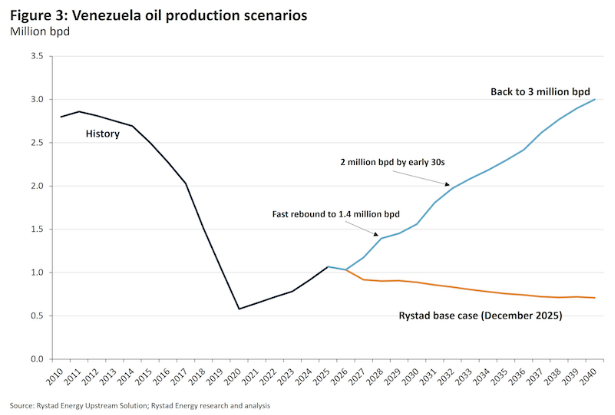

That matters because Venezuela’s challenging oil fields could take even longer to re-commercialize. Here’s the base case from the consultants at Rystad Energy, in a bonus chart.

Even in the most optimistic scenario, it will take 14 years to achieve Venezuela’s previous 2010 output of 3 million barrels per day. If you’re a professional investor, that’s essentially a lifetime.

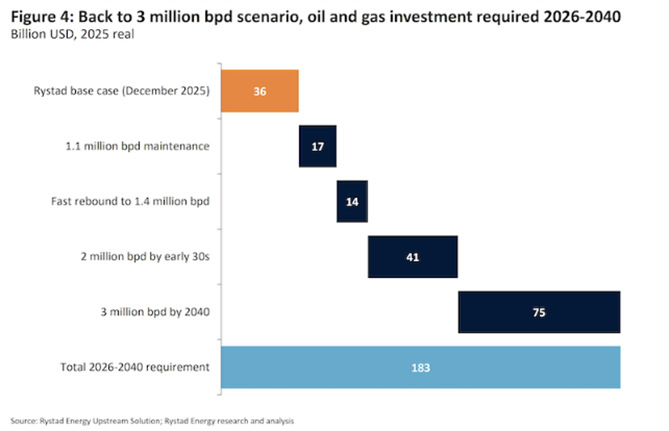

In addition, even reaching full production in 14 years would take an eye-watering $183 billion of investment by Rystad’s calculations. For comparison, that’s roughly 50% more investment per barrel than what Exxon Mobil Corp. (XOM) spent on its Liza Unity project in Guyana. Below is an additional chart that illustrates this issue…

So, perhaps Venezuelan oil may someday alter my bet on oil. After all, the country does sit on the world’s largest known oil reserves, and there’s probably plenty more that is yet undiscovered. I expect a lot of attention will be showered on firms like Chevron that have experience working in Venezuela.

Besides, Venezuela’s cheaper rivals will eventually run out of oil. No oilfield lasts forever.

But all this will take time, money, and oil prices moving back to the $80 range. And I don’t know about you, but I can certainly think of more profitable ways to ride oil 40% higher without having to wait on a Venezuelan oil bonanza that may never come.

Instead, my attention remains firmly focused on players in the Permian Basin… the ultra-low-cost producers in West Texas and southeast New Mexico that should print money over the coming decade.

Betting on America

You see, these oil companies sit on some of the easiest reserves in the world to extract. That means they generate a lot of excess cash that can be used to buy up even more cheap fields, and so on. There’s still a lot of untapped potential in the Permian Basin.

In addition, these companies are cheap. The one I own in Fry’s Investment Report trades at just 9X forward earnings and produces a splendid 4% dividend yield.

Best of all, these Permian firms are sitting on the cusp of a natural gas bonanza. Liquefied natural gas (LNG) terminals on the Gulf Coast are coming online all at once, and I expect my pick to perform splendidly in the coming years.

For the name of this “best of the best” oil and gas pick that I believe will outperform, learn more about joining me at Fry’s Investment Report here.

Regards,

Eric Fry