Meb Faber’s Idea Farm republished a great study — Capital Allocation: Evidence, Analytical Methods, and Assessment Guidance — by Credit Suisse’s Michael J. Mauboussin and Dan Callahan, CFA that breaks down what American companies have been doing with their cash over the past 33 years.

The results?

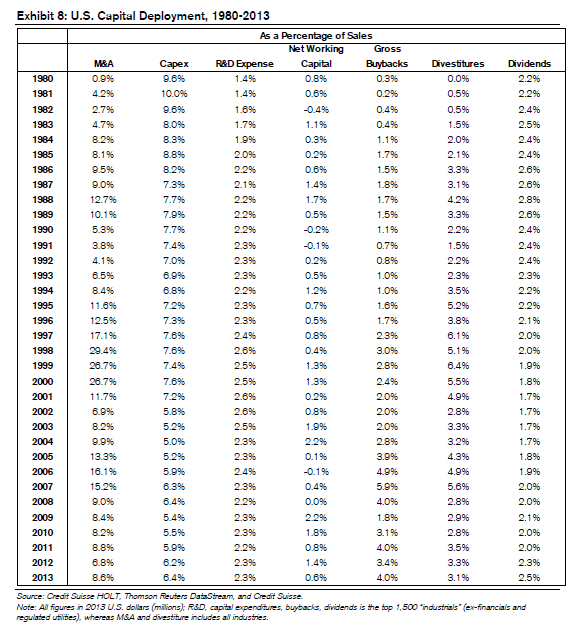

- Dividends paid as a percentage of total sales are at levels last seen in the 1980s. And share buybacks are at their highest levels since before the 2008 meltdown.

- Interestingly — and contrary to the common view that U.S. companies are failing to invest in the future — research and development expenses have stayed pretty constant since the mid-1980s.

- And capital expenditures — though lower than during the 1980s and 1990s — in 2013 reached the highest levels since 2001.

So where is the cash for dividends and buybacks coming from?

Primarily from divestitures (i.e., selling off less productive assets or business lines) and from fewer mergers and acquisitions.

In other words, U.S. companies really are getting to be more shareholder-friendly. They’re “investing” less in value-destroying mergers and selling off the parts of their businesses that contribute the least to shareholder value. Not bad!

So … Cheer Up!

Is there a takeaway from all of this?

Absolutely. We should give some of the doom and gloom a rest. American companies

are investing in the future, and they are doing so while still making it a priority to take care of their current investors. This has been helped along by record profitability, which in turn has been helped along by the brutal cost cutting of the past few years and by creative use of the tax code to minimize taxes paid.

Can it last? No, not forever. Extraordinarily high profits tend to be self-correcting in that they encourage new competition to enter the fray. And as the labor market heals, wages will rise and labor will take at least a modestly larger share of profits.

There also is blowback with respect to tax loopholes; consider the outcry for legislation to ban “tax inversions,” or mergers with no real purpose other than redomiciling for tax purposes.

So, the days in which companies can return record amounts of capital to shareholders while also funding their investment needs will eventually come to an end. When that happens — and it might be another several years before it does — I expect stock buybacks to be the first thing to be curtailed, as the consequences for reducing share repurchases are relatively minor, whereas decreasing a dividend tends to spook investors.

In other words, this golden age in which companies reward their shareholders lavishly while still funding future growth will gradually come to an end, but we’re not there yet.

And in a world in which the 10-year Treasury barely yields 2.4%, high-quality, dividend-paying stocks will remain the most attractive investment destination for the next several years.

Charles Lewis Sizemore, CFA, is the editor of Macro Trend Investor and chief investment officer of the investment firm Sizemore Capital Management. As of this writing, he did not hold a position in any of the aforementioned securities. Click here to receive his FREE weekly e-letter covering top market insights, trends, and the best stocks and ETFs to profit from today’s best global value plays.