Nowadays, not many banks can claim a mega star CEO like Jaime Dimon. One would expect his presence alone should reward JPMorgan Chase (JPM) stock. Ironically, however, the reverse is all too true.

Compared to peers like Wells Fargo (WFC), JPM stock trades at a discount despite having similar performances in most segments. This anomaly raises two important questions. First, why aren’t investors willing to pay a premium for JPM stock? And second, will that ever change?

Compared to peers like Wells Fargo (WFC), JPM stock trades at a discount despite having similar performances in most segments. This anomaly raises two important questions. First, why aren’t investors willing to pay a premium for JPM stock? And second, will that ever change?

To answer the second question, let’s look into the what has been holding down JPM.

JPM Stock and the Cost of M&A

JPMorgan hasn’t always been the behemoth it is today. In fact, the sheer size of JPMorgan is a result of an aggressive M&A strategy that was articulated by none other than Jaime Dimon. He sent JPM on an aggressive M&A spree, taking over Washington Mutual and of course Bear Stearns to make JPMorgan the mega bank that it is today.

The problem with this approach? While that growth made JPMorgan a global player, there has been no reward when it comes to JPM Stock.

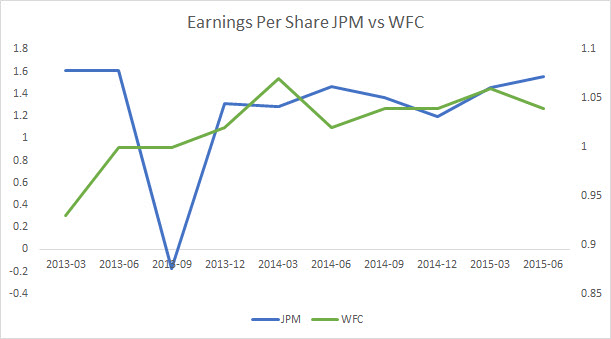

In terms of earnings per share growth, JPM stock has matched WFC stock — excluding a one-time bump in 2013. But when we examine efficiency indicators, such as return on equity, a different picture emerges.

On a trailing 12-month basis, JPM stock has posted a 10% return on equity, vs. 13% for WFC stock. JPM Stock suffers from higher operational and litigation costs, which eventually leads to lower shareholder returns. Hence why investors aren’t willing to pay a premium for JPM Stock.

Click to Enlarge

For example, WFC Stock trades at 11 a P/E ratio of 12.7 vs a P/E ratio of 11 for JPM Stock. Price-to-book ratio, another important valuation matrix for banks, presents the same picture. WFC stock trades at 1.6 times book value, and JPM Stock trades at a mere 1.1.

JPM Stock just isn’t profitable enough per dollar of revenue.

JPMorgan Earnings: What to Expect?

Now, the more important question is, can this change?

It certainly can. JPMorgan is leading an aggressive cost-cutting initiative that should amount to a total of $1.4 billion in annual savings. So next week, when JPMorgan earnings are reported, investors will want to see fair progress in that direction.

If analyst estimates are any indication, JPMorgan is already finding success with cost-cutting. Right now, the consensus is calling for earnings of $1.37 per share, representing a very slight year-over-year gain. If JPM posts earnings that meet or exceed those expectations, it means a shift in the right direction. ROE, arguably the most important indicator for shareholders, could gradually match JPMorgan’s peers.

Bargain or Not?

The bottom line is this: JPM stock has the potential to become as profitable as, say, WFC Stock. And that makes it an interesting long-term value. If investors were willing to pay the same premium as WFC stock, JPM could be trading 45% higher than it is today.

But in order for that to happen, the cost-cutting process needs to continue enough to inflate earnings and raise ROE.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.