After ringing up an anemic performance in the markets last year, executives at Intel Corporation (NASDAQ:INTC) are anxious to close out a strong 2016. Unfortunately, buyers of Intel stock just don’t share the same priorities.

Year-to-date, INTC is up 1.68%. Although this is a small gain, it remains close to last year’s redline numbers during the halfway point.

With this in mind, many investors wonder: Can the semiconductor giant get out of its rut? Or is INTC stock doomed for another date with mediocrity?

Despite all the terrible things we’ve been hearing regarding the personal computer market, there is some optimism for Intel stock, albeit slight.

Compared to the prior month, one analyst has upgraded their bullishness towards INTC by awarding a “strong buy” recommendation. BlueFin Research Partners took it a step further, noting that the company sits on better fundamentals. Also, the risk of a moribund PC market is already priced in to the current value of INTC stock.

BlueFin brings up an important point in that they estimate INTC has unexpectedly increased production for semiconductor materials. That would put the technology firm ahead of its forecasted schedule. This is especially significant from an on-hand supply perspective. Since the first quarter of fiscal year 2014, days inventory has grown uncomfortably high.

In fact, for the full year 2015, days inventory has grown to the highest level since at least the last ten years. The added production “bonus” should go a long way in stemming this trend.

With earnings results coming up soon for INTC stock, it’s well within the realm of possibility that shares may receive a boost. Intel stock has been putting up consistent numbers, going on a nine-hit streak where it has either met or exceeded consensus expectations. Against a Q2 FY2016 target of 53 cents, the odds favor INTC making the bulls look good.

Profitability margins are among the best in the semiconductor business. Along with ramped up production, INTC sales for Q1 exceeded its year-ago results. That’s something that fierce competitors Advanced Micro Devices, Inc. (NASDAQ:AMD) and Texas Instruments Incorporated

(NASDAQ:TXN) can’t say.

INTC Stock: Weakening Technicals

What AMD and TXN do have over Intel stock is the scoreboard. INTC is unfortunately — and compared to AMD, inexplicably — a classic case of a fundamental winner being a technical loser. However, the reality is a bit more nuanced.

As InvestorPlace contributor Chris Tyler rightfully points out, INTC stock has received some upside bursts due to its inroads towards cloud computing, data centers and the burgeoning Internet of Things. The obvious problem, though, is that these opportunities are not proprietary to INTC. But the deal killer is the company’s complete lack of traction in the mobile space. Intel stock investors don’t want to just hear about potential revenue — they need something right here, right now.

Like so many opportunities these days, the decision to buy Intel stock hinges largely on personal expectations. As a component of a broader portfolio, INTC can do very well. But if you’re looking for a grand slam, that ship has probably long sailed.

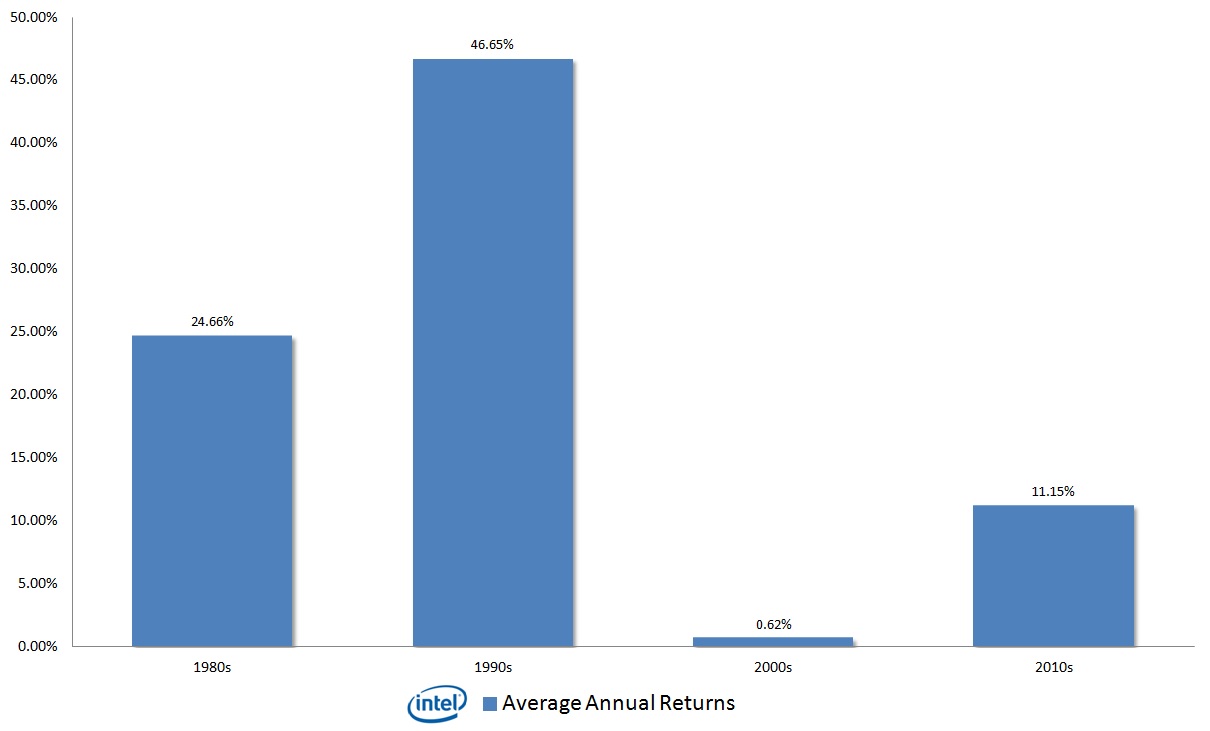

Click to Enlarge

In the 1980s, when INTC stock was first introduced to the markets, shares returned on average 25% every year. The 1990s saw an unprecedented lift in tech stocks, with INTC averaging 47% returns. Even more remarkable, not one year in that decade ended as a dud.

But the 2000s saw a sharp reversal in fortune due to multiple recessions and geopolitical crises, with Intel stock barely moving into positive territory. Emblematically, half of those years ended up in the red by double-digit margins.

In contrast, INTC stock is doing much better this decade, averaging 11% returns inclusive of the year so far. But like an aging superstar athlete, it’s clear that shares don’t have that spring in their steps.

The biggest gain of the last six years was a 45% return in 2014. Compare that to an average high of 114% from the 1980s through the 2000s. You can buy any dips, but its comeback potential has been sharply limited.

Admittedly, Intel stock is a tempting offer. It has been beaten up relative to its competitors, despite management pushing very positive initiatives. But despite being a big-time player, INTC faces big-time challenges. That resistant force has prevented shares from reclaiming former glory. INTC stock is still a solid investment, but that might not be good enough to impress most traders.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.