It’s safe to say Microsoft Corporation (NASDAQ:MSFT) has been on fire this year, up 17% in 2017 and almost 30% over the past 12 months. In a year like this, MSFT stock may seem unimpressive. But for a $560 billion market cap company, that’s a huge move. Despite the stock topping out near $75, there’s still upside to be had.

Last quarter, Microsoft gave investors something to cheer for, beating on top- and bottom-line expectations. The recent results only highlight the importance of Microsoft’s change of leadership a few years ago.

When Steve Ballmer stepped down and Satya Nadella took over as CEO, Microsoft was about to embark on a totally different path.

The Breakdown on MSFT

Mainly, one flying toward the clouds.

E-commerce is definitely a driver behind the stock appreciation in Amazon.com, Inc. (NASDAQ:AMZN). But the company’s robust Amazon Web Services is what really kicked AMZN stock into another gear. The same can be said of its Seattle-based roomie, Microsoft.

Earlier in the month, Microsoft announced a move to cut jobs in its salesforce in order to put more focus on its cloud division. MSFT’s Azure division — a collection of cloud-based services for developers and IT professionals — really lit it up. Last quarter, Azure revenue grew a whopping 97%, outpacing the prior quarter’s 93% growth. Intelligent cloud revenue grew 11% to $7.4 billion.

Are investors underestimating the cloud? Companies like Amazon, Microsoft and Alibaba Group Holding Inc (NYSE:BABA) continue to soar on this rising trend. So long as Microsoft continues to grow its Azure unit rapidly, investors will likely keep paying a premium for its stock.

Azure is key, but it’s not the only thing in Microsoft’s arsenal. Revenue in Productivity and Business Processes was $8.4 billion and increased 21%. However, Personal Computing revenues of $8.8 billion did fall 2%.

MSFT Stock: Catalysts and Valuation

If Microsoft can drive unexpected growth in its sluggish Personal Computing unit, it can drive shares higher. However, in its Productivity and Business Processes unit is LinkedIn, which MSFT recently acquired for $26.2 billion. On the conference call, CFO Amy Hood said the company would continue “making incremental investments in LinkedIn to fuel its continued strong revenue growth.” This too could lead to an upside surprise.

Given that Microsoft beat fourth-quarter earnings-per-share estimates of 71 cents by almost 40%, I think they have leeway to spend a bit more liberally. Also consider that last quarter free-cash flow grew 50% year-over-year. If MSFT drives more revenue growth out of the cloud and LinkedIn, investors could be in for a pleasant surprise.

Given management’s guidance for the upcoming quarter, Productivity and Business Process revenue appears set to accelerate.

In Q1 2017 segment revenues rose 21%. At the midpoint for its Q1 2018 guidance though, management is looking for 22.4% growth. Unfortunately, its growth rate for Intelligent Cloud looks like it will slow from 11% growth to about 9.4% growth. Additionally management does expect gross margin to contract about 100 basis points next quarter.

Is all the good news priced into MSFT stock? Shares already trade with a price-to-earnings ratio of 32 and forward P/E ratio of 20.

It’s certainly not cheap. However, MSFT stock is far cheaper than other cloud plays like Amazon, Alibaba and Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL). In other words, even though MSFT stock isn’t cheap, it’s the cheapest of these four mega cap stocks. It’s got intense growth in the cloud and Nadella continues to find ways to expand the MSFT ecosystem.

The Bottom Line for MSFT Stock

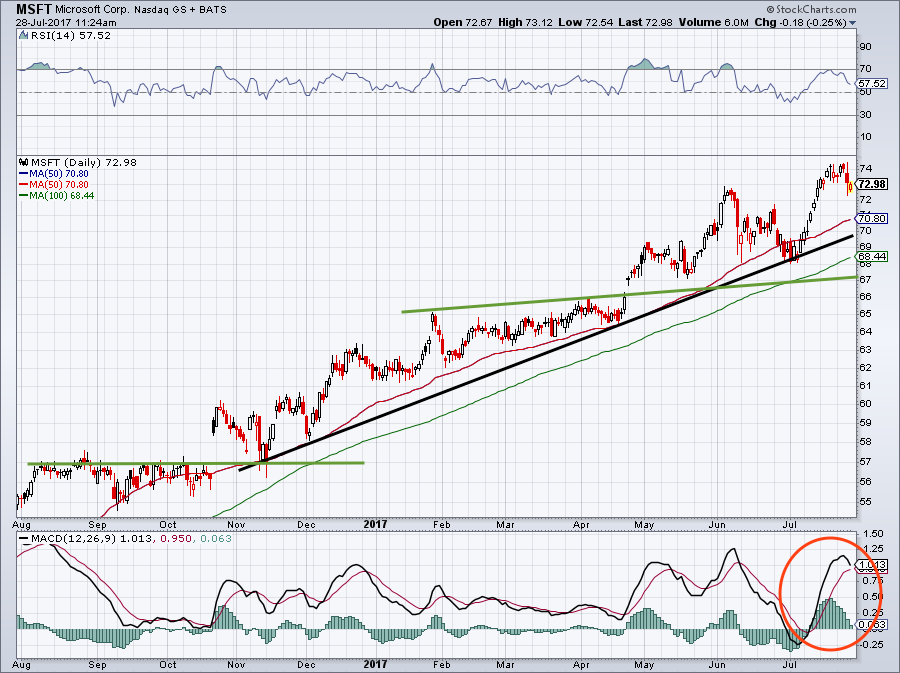

Click to Enlarge

On Friday, I wrote about the possible breakdown in tech stocks. Specifically, the PowerShares QQQ Trust, Series 1 (ETF) (NASDAQ:QQQ) revealed that it’s not immortal. That is an ongoing concern with stocks that are trading above their historical valuation norms.

But that’s what also makes MSFT stock difficult: It’s valuation is constantly climbing. Because the company is fueling faster and faster growth, it’s continually earning a higher valuation from Wall Street. As the little guy, we don’t get to decide what’s fair value. But it’s underlying business still has powerful momentum and there’s little reason to bet against that ending anytime soon.

For investors looking to buy, here’s the game plan. MSFT stock has been on a steady uptrend since November (black line). A retest of that level and the 50-day moving average would put the stock between $70 and $71. Investors could start by buying MSFT in that area. A break below should find support from the 100-day moving average. Additionally, $66 to $67 should have some support.

These levels give long-term investors solid areas to add to their position over time. For short-term traders, they present well-defined risk-reward entries and exits. Additionally, MSFT pays a dividend yield of 2.15% — a payout it has raised for 13 consecutive years.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.