In response to an ugly incident a few weeks ago in which drug company Turing Pharmaceuticals — run by a former Wall Street hedge fund manager, no less — raised the price of a parasitic infection therapy by more than 5,400%, Clinton threatened to take action against “outrageous” price gouging.

The former First Lady and current Presidential candidate apparently has the anti-Midas touch when it comes to digital technology. Her message, delivered via Twitter’s (TWTR) social media platform on Sept. 21, had a swift and powerful impact.

Immediately following Clinton’s tweet, shares of the benchmark exchange-traded fund iShares NASDAQ Biotechnology Index (IBB) rapidly tumbled in the markets, closing down 4.6% against the prior session. Worse yet, the sentiment towards the biotech stocks ETF continued to deteriorate over the next six trading days, dropping an additional 15% of value.

As English playwright William Congreve once wrote, “Heaven has no rage like love to hatred turned, Nor hell a fury like a woman scorned” — especially true when that woman is Hillary Clinton.

The good news for biotech stocks — specifically for those investors who have been sitting on the sidelines — are the attractive price points to which several premium names have fallen. Biotech stocks have ridden an enormous wave of bullishness and a correction at this point is healthy and natural. Even with the recent downturn, the IBB ETF is up more than 250% over the past five years.

The key for investors is to select fundamentally strong biotech stocks which have exciting growth potential. Here are three undervalued biotech stocks that could buck the industry’s trend.

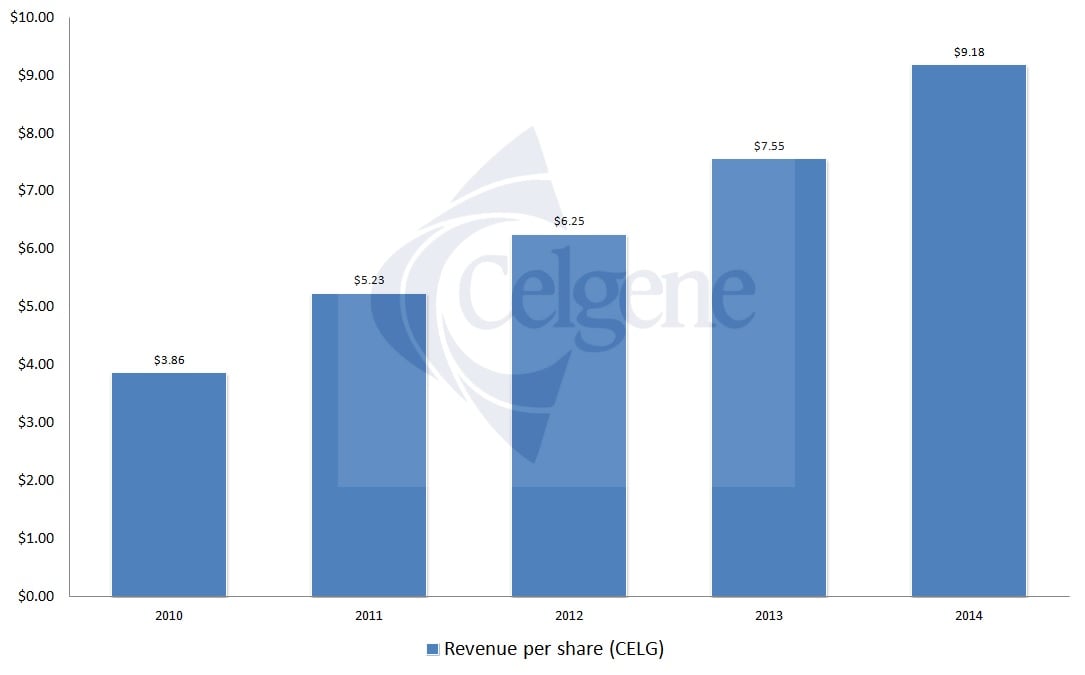

Biotech Stocks to Buy: Celgene Corp. (CELG)

Click to Enlarge

Celgene Corp. (

CELG) is among several biotech stocks actively working to find a cure, and the company has a number of commercial stage therapies that are currently distributed.

On paper, CELG stock is a very solid investment, with a market capitalization north of $90 billion and net income and cash-flow trends deep in the black. However, CELG stock, along with the biotech stocks ETF, tumbled in mid-July of this year as broad market concerns took a bite out of the healthcare sector.

Those that jumped ship are overlooking some key facts. Over the past five years, revenue growth for CELG stock is nearly 26%, while growth in earnings before interest, taxes, depreciation and amortization is 23%. This suggests a consistent retention of profitability margin outside of taxation and accounting procedures that could potentially muddy net income figures.

And while CELG stock’s trailing price-to-earnings ratio of 44.5 is a tad above the industry average, its forward P/E ratio — or the P/E calculation using estimated earnings figures — is 19.6, which is about 15% lower than the industry median ratio of 23.09. Theoretically, this suggests that Wall Street anticipates better-than-average earnings growth for CELG stock, a not unreasonable assumption given its track record in revenue and EBITDA performance.

So don’t fret about CELG stock’s losses in recent months — underneath the hood is a very solid investment opportunity.

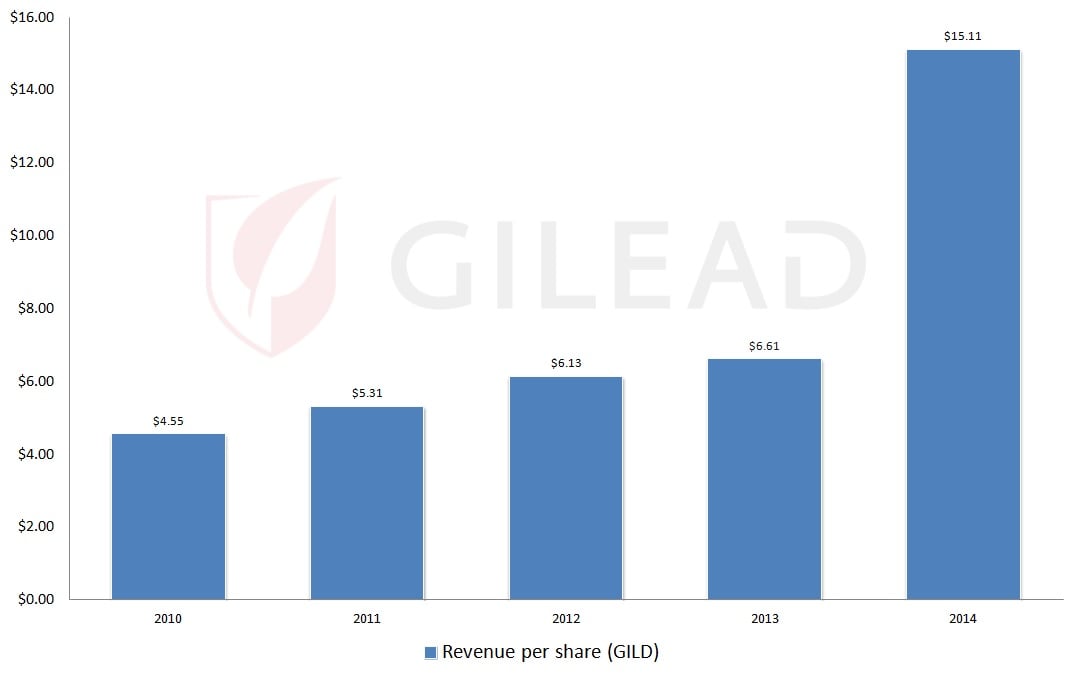

Biotech Stocks to Buy: Gilead Sciences, Inc. (GILD)

Click to Enlarge

Early this year, health insurance provider Aetna Inc. (AET) reached a deal with Gilead to provide discounted Hepatitis C treatments for the former’s 11 million customers. The negotiated cost still proved to be quite lucrative for GILD stock investors, with the pharmaceutical giant raking in $4.55 billion in the first quarter of fiscal year 2015 off sales of its Hepatitis C drug.

While GILD stock almost immediately went on a 17% run up in the markets following the May 1 announcement, shares entered a heavy bout of volatility in late June, eventually losing 16.5% of value from its peak. While GILD stock is still up 9% year-to-date, so far, it’s a story of what could have been.

That should suit investors looking for an undervalued opportunity just fine. GILD stock’s trailing P/E ratio is a mere 10.9, some 71.5% lower than the industry median ratio of 38.3. Additionally, GILD stock’s forward P/E ratio on surface level is an absurdly low 8.7.

However, it’s not so unimaginable when you look at the numbers. Gilead’s management team has been concentrating on profitability, as evidenced by its EBITDA growth rate over the past five years of 27.2%, which in fact is nearly 3% higher than GILD stock’s revenue growth within the same time frame.

The sharp volatility hammering biotech stocks in general shouldn’t affect GILD stock permanently — the pharma company is far too strong fundamentally.

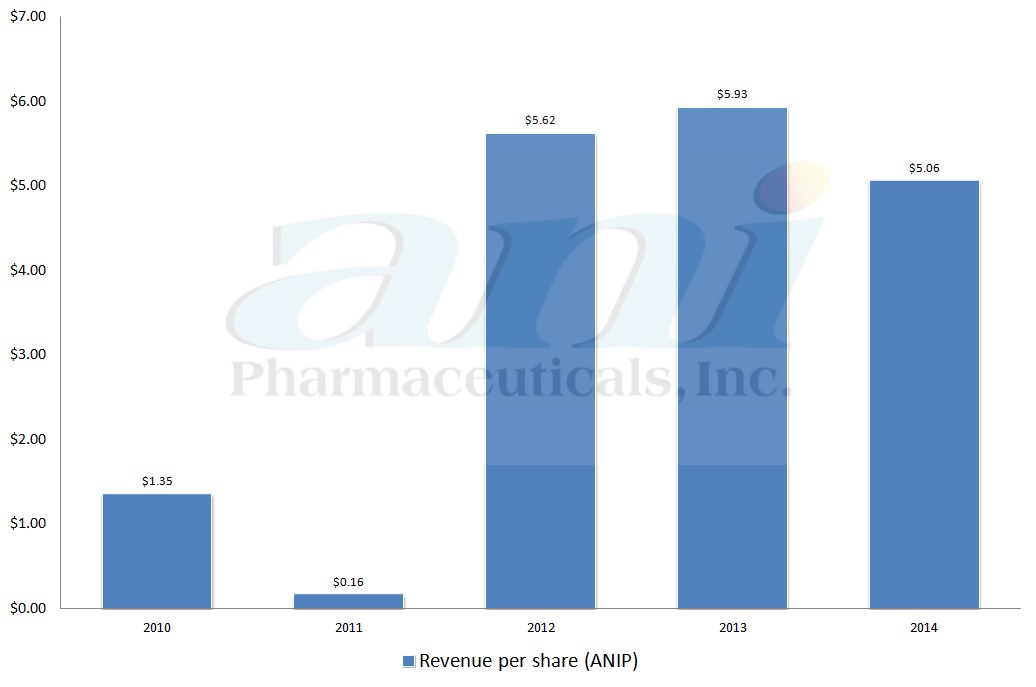

Biotech Stocks to Buy: ANI Pharmaceuticals Inc. (ANIP)

Click to Enlarge

Nevertheless, ANI Pharmaceuticals has a smart business strategy, specializing in both branded and generic prescription therapies. This allows the company to compete in margin as well as volume.

Unfortunately, the diverse income stream hasn’t paid off that much. Throughout the past 52-weeks, ANIP stock has been quite the choppy affair, soaring to a high of $73.54 and plummeting to a low of $26.87. Year-to-date, ANIP stock is down 25%, making it one of the more deeply affected companies from the biotech stocks’ backlash.

However, a robust 6% move on Thursday may turn out to be an early signal of intent. Despite broad ugliness in the markets, bullish investors would point towards ANIP stock’s trailing and estimated P/E ratios — both of which are well under the median for biotech stocks.

In addition, revenue growth over the past five years has been substantial — over 52%. The major sticking point is margin. ANIP stock’s net income was in the red for the first three of the past five years, but especially so for FY 2010 and FY 2011.

Although it’s not completely airtight, ANIP stock is well-rounded for a small cap biotech firm, and those willing to gamble on it could be well rewarded.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.