The broader health care sector is rapidly looking like a case of mismanaged expectations. Although it was bracing for a Hillary Clinton victory, the industry was pleasantly surprised when Donald Trump pulled out the upset. A day after the general election, the benchmark Health Care SPDR (ETF) (NYSEARCA:XLV) jumped to a 3.5% gain. For the year, the XLV is up over 9%. Backed by promises of less-burdensome regulations, health care and pharmacy stocks apparently took solace in their wallets.

But whatever goodwill President Trump engendered is starting to fade quickly. The administration has not been a popular one with controversy after controversy. And now, the pledge to “repeal and replace” the Affordable Care Act hit a snag.

Just days after the GOP proposed the new “American Health Care Act,” it received sharp criticism, especially from moderate Republicans. Senator Rand Paul was particularly vocal in his criticism, dubbing it as “nothing more than a revamped federal entitlement program.”

As a result of the pronounced backlash, several pharmacy stocks saw their upside momentum halted. Chaos in politics, especially as a result of a convoluted health care system, does no favors for the broader industry. But within this rising upheaval, new questions are asked about the necessity of skyrocketing drug prices. In particular, pharmacy benefit managers are under the crosshairs.

Pharmacy benefit managers, or PBMs, are a little known and little regarded industry within an industry. Originally starting off as payment processors, they have evolved into entities that can decide “which drugs insurers cover, what they cost and how much pharmacies are reimbursed for them,” according to USA Today. At first, they probably served a viable purpose. Now, however, many people and institutions are out for their head.

That spells big trouble for pharmacy stocks that promote or are leveraged towards the PBM business. These service providers have responded that pharmaceuticals are mostly responsible for rising drug prices. The PBM, they argue, is just trying to manage a bad situation.

Even if true, PBMs have a tough public relations battle. The accusation that they are leaches of an overweight bureaucracy is very convincing. Furthermore, several companies have reduced their health care costs substantially by cutting out the major PBMs.

No matter what, this battle will turn ugly for pharmacy stocks exposed to this business. Here are three names you should avoid.

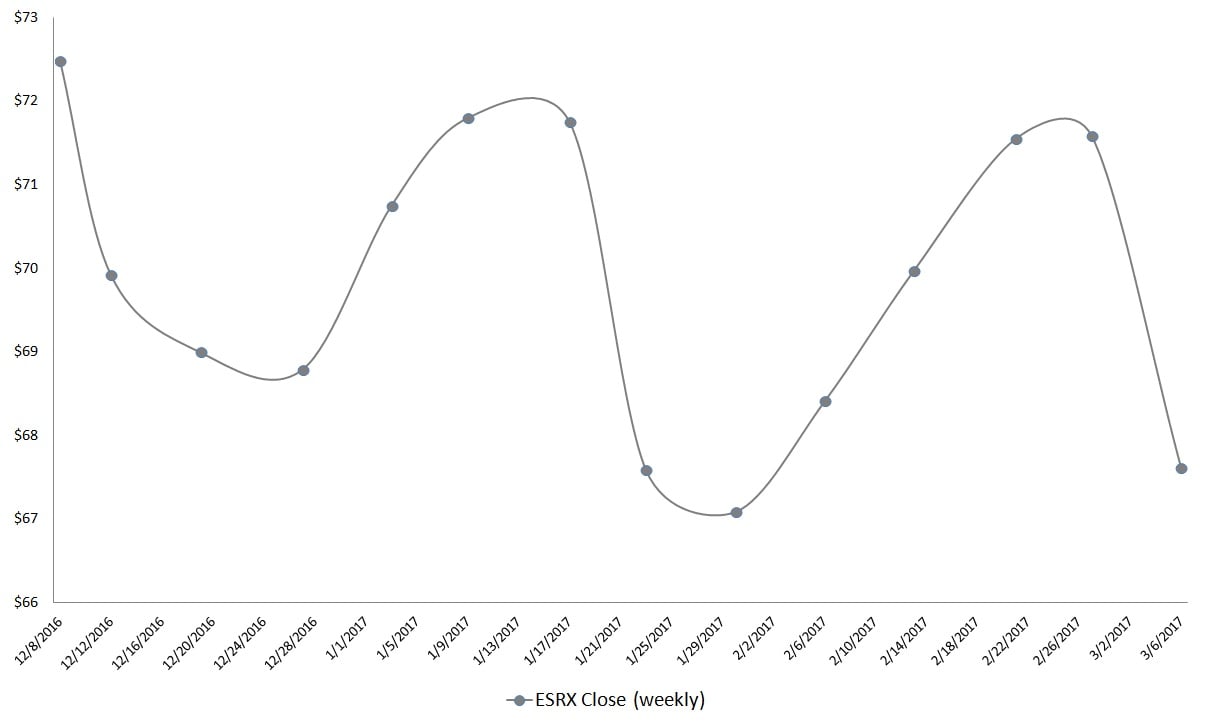

Pharmacy Stocks to Sell: Express Scripts Holding Company (ESRX)

Click to Enlarge

To his credit, Trump took the issue seriously. Late in January, he met with leading pharmaceutical companies, urging them to reduce their pricing. In turn, the pharmaceuticals threw PBMs under the bus. That’s bad news for pharmacy stocks like Express Scripts Holding Company (NASDAQ:ESRX).

ESRX, along with two other competitors, control 70% of the prescription market, according to Pembroke Consulting. Even though Express Scripts makes a case for itself as a prescription benefit plan provider, the optics look terrible. First, there’s the fact that the majority of the industry is dominated by an elite few. Americans have already been burnt by big business, so it’s not a stretch to assume that pharmacies will do the same.

Second, PBMs like ESRX operate in the dark. I’m sure they don’t intend to. However, Express Scripts is in an industry that doesn’t pride itself in clarity and transparency. Furthermore, PBMs involve themselves in contracts that don’t necessarily produce the best prices for clients. That could be the reason why ESRX experienced volatile trading as of late.

If they continue to get thrown under the bus, don’t look for Express Scripts to write itself a doctor’s excuse.

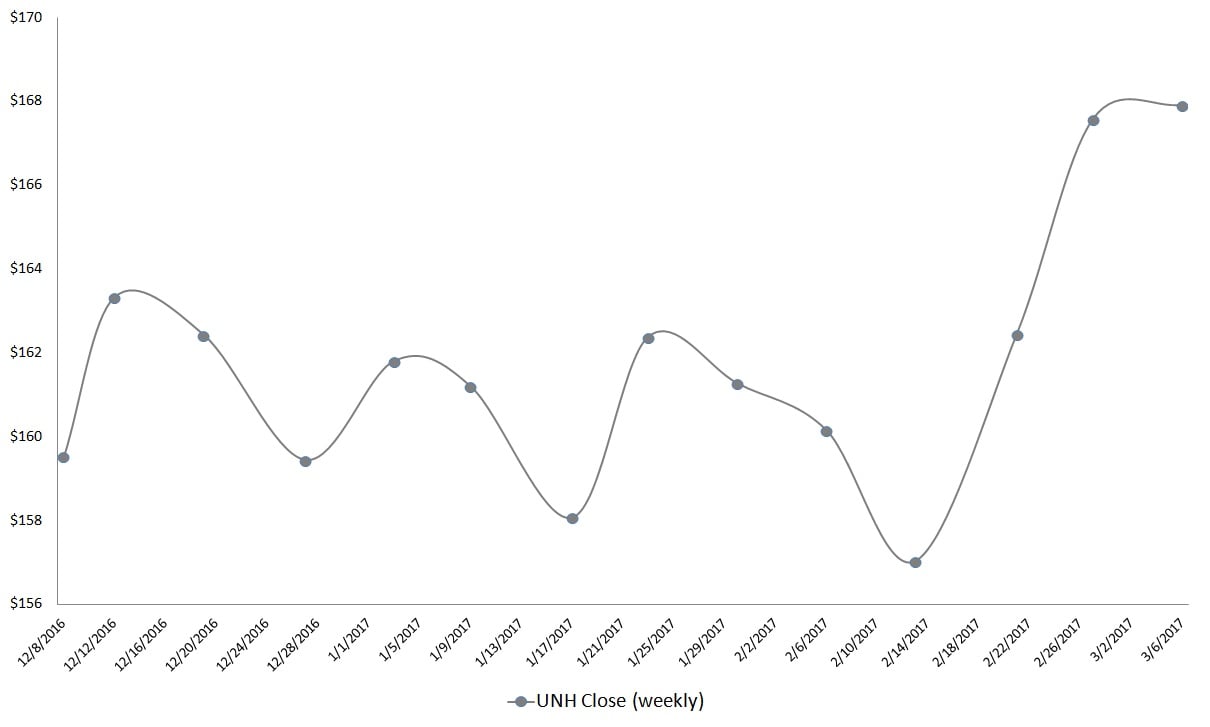

Pharmacy Stocks to Sell: UnitedHealth Group Inc (UNH)

Click to Enlarge

True, it’s not going to sink UnitedHealth, but it’s not doing the parent company any favors.

Whether we’re talking about Donald Trump or eroding geopolitical stability, the markets are contested. If UNH starts to lose sentiment, investors have other pharmacy stocks from which to choose. And the microscope on PBMs has to be worrying for UnitedHealth shareholders. According to MTS Health Partners, $15 out of every $100 spent on branded pharmaceutical therapies is taken by middlemen. PBM advocates argue that these costs are necessary to prevent an even higher surge in drug costs.

Here’s the bottom line — the American people want answers. They’re going to look for the easiest target, and that is the PBM industry. President Trump, buoyed by populist support, isn’t helping matters. He sees things in black and white. Therefore, health care is “good”, and PBM is “bad”. That puts pharmacy stocks like UNH in quite a quandary.

UnitedHealth has enjoyed a stellar run, but it just might get derailed by the Trump train.

Pharmacy Stocks to Sell: CVS Health Corp (CVS)

Click to Enlarge

After all, Donald Trump himself campaigned on the message of drain the swamp. The target was Washington waste, but it could just as easily apply to PBMs like CVS.

What the benefits industry will have to reconcile is the sharp variance between us and the rest of the world. In developed countries, only $4 out of $100 spent on brand-name drugs are allocated to middlemen. From that figure, international PBMs receive a smaller cut. Comparing apples to apples, our developed counterparts have at least a 50% discount on PBM charges. Under Trump’s vision of America, that simply won’t fly. That also means CVS needs to watch its back.

What makes these pharmacy stocks so vulnerable is that several Fortune 500 companies have a proven record of eliminating the “Big Three” PBMs, and saving money. In addition, upstart PBMs are starting to take market share away from CVS and its rivals. Their argument is simple — size and legacy doesn’t matter.

If the “independent” PBMs start gaining traction, that could spell doom for CVS.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.