Dull investments like AT&T Inc. (NYSE:T) can almost always be relied upon as a steady rock during turbulent times. After all, if these boring stocks were volatile, they would certainly not be boring, and few would invest in them. For the telecom giant in particular, the AT&T dividend offers a tangible alternative to the frequently pumped-out “hot picks.”

AT&T stock operated successfully for years under this “steady-as-she-goes” plan.

Unfortunately, the company is experiencing some rare consternation. T stock is down 11% year-to-date. This “performance” is notably better than rival Verizon Communications Inc. (NYSE:VZ), which is down 14%, but it’s never great to compare negative metrics. At this time last year, T was up 18%. The question is — what happened?

Challenges Ahead for AT&T Stock

Earnings season was not a strong point for AT&T stock. Although the telecom firm managed to hit its 74 cent earnings-per-share target for Q1, revenue growth lost momentum. Registering nearly $39.4 billion, this was about 3% down from the year-ago quarter. The figure also missed the $40.5 billion analyst consensus.

Subscriber growth, though, was the big miss for T stock. Instead of reeling in 95,000 customers, the company lost 61,000. The visceral challenge, according to InvestorPlace writer Tom Taulli, is the “aggressive price wars” waged by T-Mobile US Inc (NASDAQ:TMUS),

Sprint Corp (NYSE:S) and smaller, nimbler competitors.

As evidence, Mr. Taulli points towards TMUS racking up 914,000 net post-paid phone subscribers. Furthermore, InvestorPlace’s Richard Saintvilus reports that “T-Mobile also added 386,000 net prepaid accounts and 798,000 branded postpaid phone net additions, which it says captures more than 250% of industry growth.”

These upside challenges for AT&T stock align with an argument forwarded by analyst Aaron Levitt, who stated that telecom firms were all too eager to jump on the mobile bandwagon. Now that this market has matured, the industry must find new avenues for growth.

For T stock, the challenge translated into taking over content creation and distribution. The DirecTV acquisition is the most conspicuous result of this newfound effort. However, acquisitions aren’t cheap, especially of the magnitude of the DirecTV deal. The inevitable jump in long-term debt liabilities has pressured the AT&T dividend.

As Mr. Levitt explains, “Right now, T stock is paying $1.96 in dividends, while the over the last 12 months it has earned only $2.04 in profits. That results in an insanely high payout ratio of 88%. That’s not exactly a recipe for long-term success.”

T Stock Is Still in Good Hands

Let’s be real — without the high-yielding AT&T dividend, the stock loses a significant amount of its shine.

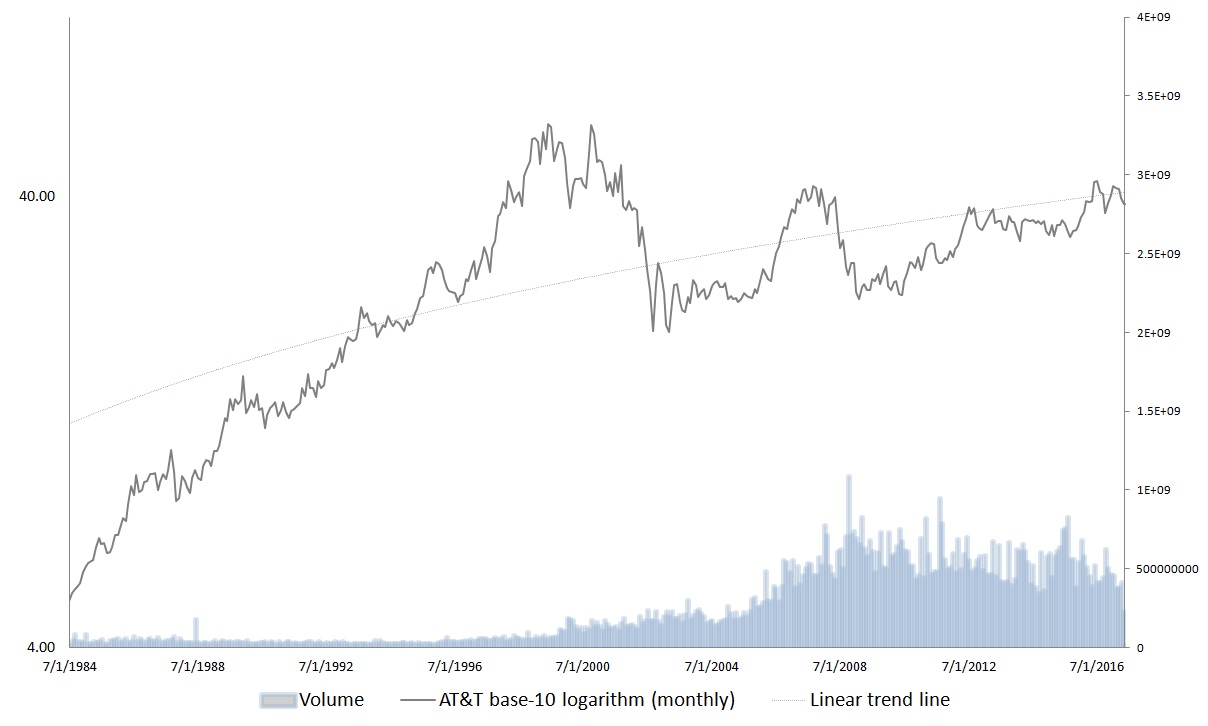

During the 1980s, T shares had average annual returns of 30%. In the following decade, it still returned a lofty 17%. And between 1984 through 1999, the company had 11 years of double-digit market growth. Since 2000, however, long-term investors have only seen 4 years of double-digits.

Again, the AT&T dividend is crucial. Today’s buyers are essentially capitulating to the fact that the telecom firm isn’t going to spark overly positive surprises. In return, they get confidence in capital stability and consistent yields. Currently, those two factors are under attack.

The good news is that the passive income should be safe. Levitt argues that the T stock “dividend might be as good as gold. That’s because most dividends are paid from free cash flows. And luckily for AT&T, it has them in spades.”

As far as the technical risk, that’s admittedly a trickier picture. The earnings results of late April sent AT&T stock sliding. In response, the bulls formed a consolidation pattern, but the movement is largely horizontal. That spells weakness in the recovery, and the stock may face nearer-term volatility.

Click to Enlarge

It doesn’t have the explosive growth potential when it was younger, but we already knew that. What’s more important is the present tendency of AT&T stock. My conclusion is that T is still what most people think it is: A boring stock that won’t let you up, but also won’t let you down.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.