Shares of Oracle Corporation (NYSE:ORCL) have taken a big tumble over the past few days. ORCL stock fell 9.2% in the three days following its earnings report. On Thursday after the close, Oracle beat on earnings per share and revenue estimates, growing sales 7% year-over-year.

So why the big fall?

ORCL stock was trading at 52-week highs prior the decline. However, guidance was the culprit. Management said it expects second-quarter sales to grow 2% to 4%, implying its revenue should come in between $9.25 billion and $9.4 billion. Analysts were looking for $9.56 billion for the quarter. On an earnings basis, management guided for 64 cents to 68 cents per share, vs. consensus expectations of 68 cents per share.

A Deeper Look Into ORCL

Oracle is only one quarter into its fiscal 2018 year. Analysts are apparently a bit too optimistic in the short-term. If that’s the case, it’s possible they are too optimistic for the full-year, too. As it stands though, they are forecasting revenue growth of 4.6% and earnings growth of 6.9%. For fiscal 2019, they are modeling sales and earnings growth of 4% and 8.2%, respectively.

Full-year concerns could be part of the reason behind the larger-than-expected drop over the past three days. Investors aren’t necessarily panicking, nor are they that worried that next quarter could come in a touch below expectations. In my view, they are more worried about full-year numbers being too high. If that’s the case, it means ORCL stock may have too high of a valuation.

In that regard, Oracle does trade at a somewhat reasonable price. At just 15 times forward earnings estimates, ORCL is not priced for massive growth in the first place. At today’s prices, we could be getting a good buying opportunity.

Where Can ORCL Stock Go From Here?

Despite the recent dip, shares are still up 25% for 2017. Further, its trailing price-to-earnings (P/E) ratio is still somewhat high. While its forward-looking P/E ratio is pretty reasonable, its trailing P/E ratio of 22 isn’t exactly a screaming buy. In fact, ORCL stock’s five-year average P/E ratio is notably lower, at just 17.7. Oracle would need to decline about 20% (or see its earnings rise 20% without its stock price moving up) in order to get back to its average P/E valuation.

Oracle’s management has spent a lot of time talking about the cloud and taken several verbal jabs at competitors like

Salesforce.com, Inc. (NASDAQ:CRM) during its conference calls. While its cloud results came up a little short last quarter, the company is looking at this segment to drive significant results in the future. That’s why we’re seeing an acceleration in Oracle’s top and bottom line.

It’s also why I don’t think ORCL stock will trade in-line with its 5-year average P/E ratio, barring a market-wide correction. Because of this stronger expected growth, the stock should have a higher valuation. So that begs the question, where should ORCL trade? Blending technicals with fundamentals is a strategy that has worked well for me. In this case, ORCL stock presents us with a few options. The first involves a further correction down to $46.

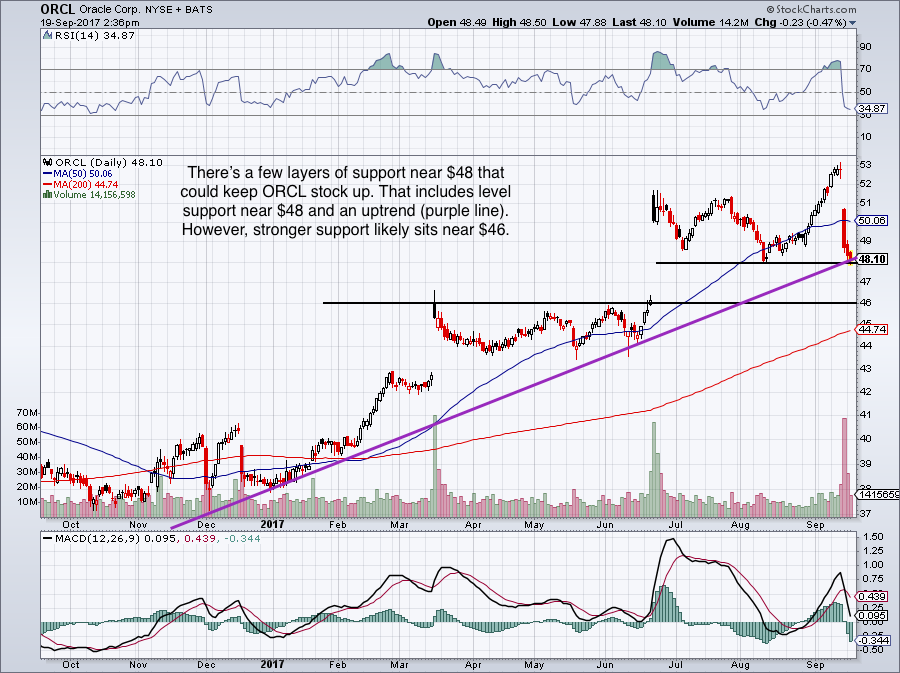

Trading ORCL Stock

Click to Enlarge

Why is this level significant? On a technical basis, $46 should act as support. Not only is it a prior resistance level (which should now act as support), it was a previous breakout level in June. That should increase the odds that it holds should ORCL stock fall that far. Second, the rising 200-day moving average, currently near $44.50, will slowly drift up to that level. It too should act as support.

That’s the technical front. On the fundamental front, it would represent about a 5% fall in the stock. Meaning that its P/E ratio would fall from 21.8 to about 20.5. Not a massive difference, I know. But the closer the P/E ratio gets to 20, the better the odds are that buyers could step in. At $46, not only will ORCL stock be down about 15% from the highs, but its valuation will be more attractive too.

At this level, paying ~14 forward earnings estimates for an 8.5% earnings grower and 4.5% sales grower isn’t too bad, (again, this is provided that analysts aren’t too rosy with their estimates).

The short-term alternative is that $48 holds as support, (see chart for details). Should it fail, $46 looks like a likely destination, though. At least investors who want to take a shot with ORCL now have a line-in-the-sand risk/reward. Either $48 holds and ORCL stock goes higher, or it breaks and likely falls to $46. I’m waiting for the latter as a more lucrative entry point.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.