Oil prices began the year trading in the mid-$50s, but fell to $43 in June. What did this mean for companies like BP plc (ADR) (NYSE:BP), Exxon Mobil Corporation (NYSE:XOM) and others?

Surprisingly, BP stock didn’t do terrible, although it was kept under pressure for most of the summer. Over the last six weeks though, crude oil prices went from $47 to $52 — a 10.6% rally. The had a nice rally of its own in that span, climbing 11.6%.

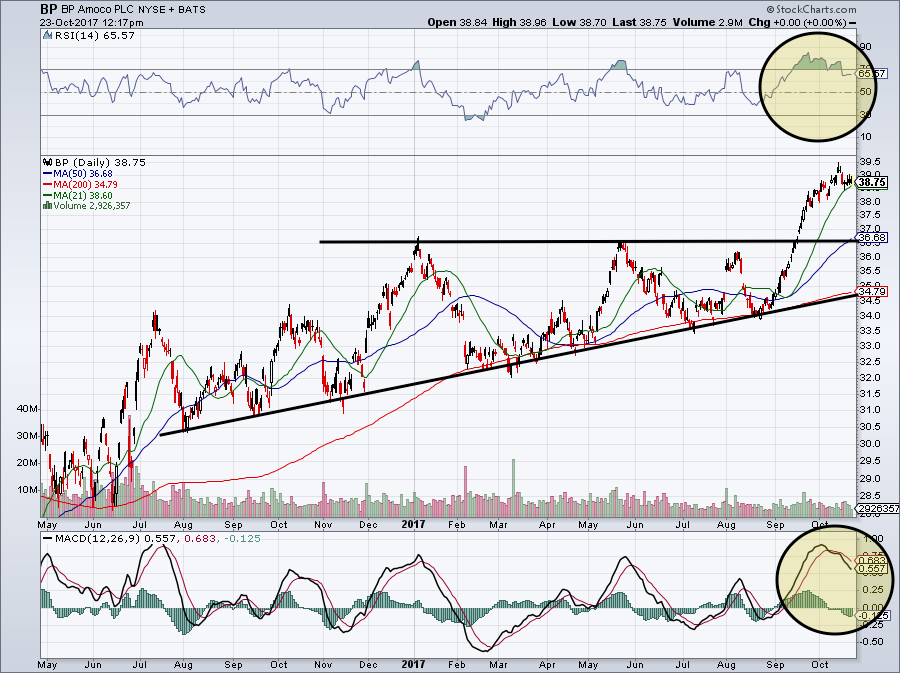

So what do we do now after such an explosive rally? Before we dig into the fundamentals, let’s do a quick run-down of the BP stock price.

Trading BP Stock

Click to Enlarge

For more than a year, the stock had been trending higher — albeit, slowly. Starting in the low-$30s, shares took their time rallying. As the lows got higher, the highs didn’t as BP continually found resistance between $36 to $37.

Now consolidating near $39 though, what should investors do?

Traders can use a close below the 21-day moving average (in green) as their stop-loss. A less-than-$1-per-share move shouldn’t rattle longer-term investors, but short-term thinkers who use discipline will be able to lock in some 12% in gains should they use that particular moving average as their stop.

Generally, I would look for previous resistance to turn into support. In this case, that level is evident on the chart around $36. Now, long-term investors could use this level as their stop-loss, as a break below would be bad news. However, that stop-loss is pretty far away from current prices and I would hate to give up all of the prior gains beforehand. Perhaps a covered call strategy or collar trade would be best in combination with a stop-loss.

For those looking to buy, I would certainly keep an eye on $36 to $37. Should shares pullback that far, this would be an excellent area to start a long position. The risk is limited (as a close below would mark the stop-loss) and the reward is high (about 10% upside to previous highs).

A Deeper Look at BP

Analysts expect sales to grow more than 20% this year to $223 billion. However, keep in mind that the company had continually generated more than $300 billion in revenue leading up to the last few years. It has had a tough go that has knocked its operations down considerably (as have many other energy companies in the Energy Select Sector SPDR (ETF) (NYSEARCA:XLE), though).

However, earnings are improving. Analysts expect $1.72 in earnings-per-share this year, up big from the 84-cents-per-share it made last year. Again, these are sort of “rebound” numbers for 2017, as 2016 was a really bad year for operations. It’s not about what BP, XOM and others did in the past, but what they’ll do in the future.

Analysts expect the company to grow earnings more than 100% from 2016 to 2017, and another 31% in 2018. On a trailing basis, trading at 34X isn’t necessarily cheap. But BP stock trades at just 17x forward earnings. I can get behind that given the robust earnings growth that investors expect over the next few years.

The Bottom Line

One concern? The BP stock dividend. Currently yielding nearly 6.2%, the dividend looks attractive at first glance. It’s the deeper analysis that’s concerning. Operating cash flow remains positive, but it has come under heavy pressure over the last few years. Not surprisingly, this has put a crimp on free-cash flow, which is now negative over the trailing 12 months.

Free-cash flow is generally vital to a company’s dividend. Further, the payout ratio doesn’t make me feel any better about the BP stock dividend. The payout ratio measures how much of the dividend is covered by earnings. So, say a company has a payout ratio of 30%, it means that it takes 30% of earnings to cover that payout. BP has a payout ratio north of 200%.

Yikes. That’s not good.

It’s not the end of the world, but if natural gas and oil prices take a turn for the worse, the dividend could be in trouble. I’m not saying it needs to be cut, I’m only saying that it’s something I would keep an eye on.

For now, I’m a buyer of BP stock on a pullback to $36.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he did not hold a position in any of the aforementioned securities.