Friday was a bad day on Wall Street, but Monday was a really bad day. Specifically, the S&P 500, Dow Jones Industrial Average and NASDAQ 100 fell 4.1%, 4.6% and 3.9%, respectively. Comparatively, Apple Inc. (NASDAQ:AAPL) “only” fell 2.5%, leading some to wonder if now is the time to buy Apple stock.

We already laid out our road map for Amazon.com, Inc. (NASDAQ:AMZN). In a nutshell, as much as we like Amazon stock, we need a bigger pullback. This monster was up more than 22% so far for the year, about four weeks in — before the pullback. We’ve seen violent flash crashes thrash stocks like Amazon in the past, so this is our game plan.

Apple stock is different though — very different.

Unlike Amazon, AAPL stock has a low valuation. It’s a profit-generating machine. This cash cow continues to sell billions of dollars in products per week with fat margins. Most companies find a way to screw up a good thing. Not Apple though. The company has firmly wrapped its hands around the consumer and refuses to let go. Unlike say, BlackBerry Ltd

(NYSE:BB).

The end result? Wild and unimpeded success.

As of the last quarter, the company now boasts cash reserves of more than $285 billion. The figure is almost laughable and it’s one reason Apple’s market cap is swelling to $1 trillion. Though it now stands at roughly $840 billion, the figure was over $900 billion just a few weeks ago. To get there, Apple stock needs to climb to roughly $200.

Let’s take a closer look to see why that can happen.

Valuing Apple Stock

Last quarter, the average selling price (ASP) for an iPhone swelled to $796, up from $695 in the same quarter a year ago. Analysts were only looking for an ASP of $755. They were also looking for China revenue to grow 9.2%, and it ultimately grew 11%.

Services revenue was no joke either, notching 18% growth to hit $8.5 billion in the quarter. Finally, Apple’s install base grew to 1.3 billion users. This should add gasoline to the services-revenue fire. This high-margin segment is a focal point for investors looking for additional growth, on top of the Beats, AirPods, HomePod and Apple Watch sales.

Massive margins are what make this such a well-oiled machine. So what exactly are we paying for this beast? A paltry 13.4 times this year’s earnings estimates. It trades at roughly 12.5 times 2019 estimates, while analysts forecast 25% and 13.5% earnings growth this year and next, respectively.

Apple stock becomes even more attractive when considering it pays a 1.6% dividend yield and buys back a massive amount of stock. Thanks to tax reform, the company recently said it plans to use $163 billion in capital return. That will likely materialize in three forms: buybacks, dividends and M&A.

Apple is the biggest buyer of AAPL stock and that trend is going to continue, keeping a constant bid under this already cheap name.

Trading AAPL Stock

Apple stock hit an all-time high of $180 in mid-January. AAPL stock then fell to roughly $165 before earnings. On Friday February 2nd though — the first trading day following its after-the-close earnings-report — the market got caught up in this violent selloff. That carnage continued Monday, and for all intents and purposes, it’s digesting on Tuesday.

So what should we do with AAPL stock?

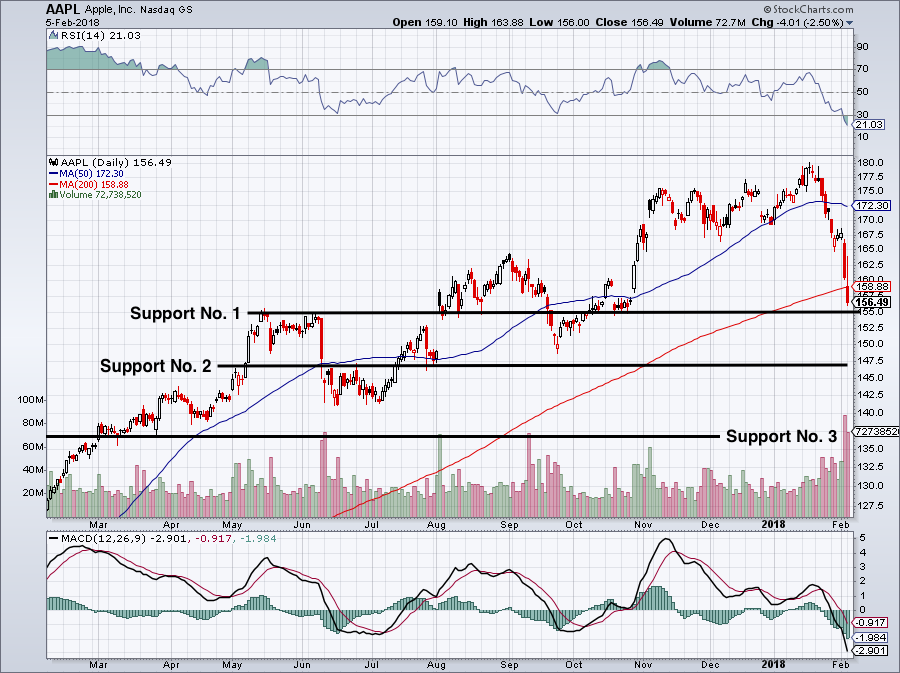

Click to Enlarge

I’m still in the camp that this name sees $200 rather than $100. So with it trading near $155 at the time of this chart, I’m looking for roughly 30% upside. Admittedly, the chart we have here is not overwhelmingly bullish. AAPL stock is now below the 200-day moving average.

It’s not clear what the rest of this week holds. Apple stock is just about at support No. 1. It’s not clear whether this will be the short-term bottom many are likely hoping for. If not, support No. 2 near $147 is in play.

As reckless as it as may sound, Apple is a buy near these levels. Maybe not an all-in buy. But definitely worth biting on. It’s got a fortress balance sheet and wide business moat. Its combination of capital return and a low valuation makes it a worthwhile long-term holding.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.