It may seem outlandish to start talking about first-quarter numbers from Bank of America Corp (NYSE:BAC). After all, the dust is still settling on Q4’s earnings, and we’re closer to BAC stock’s previous report from mid-January than the next one due in mid-April.

On the other hand, this is a market that favors the prepared and rewards foresight from owners of BAC stock (and shareholders of its rivals). Believe it or not, we’re only about three weeks away from the end of the quarter in question, so it’s not too soon to start thinking about the things that went well — and those that didn’t go well — for the bank.

And, unfortunately, there’s a red flag waving as the end of the quarter is now in sight.

An Unfamiliar Problem

Just as a quick refresher, for the last quarter of 2017, Bank of America topped its earnings estimates, but fell short of revenue estimates. The boosters to both were more lending activity and higher interest rates, while the 9% drop in trading revenue took a sizable toll on the top and bottom lines.

Those roles may be reversed when the company reports its Q1 numbers to BAC stockholders a little more than a month from now.

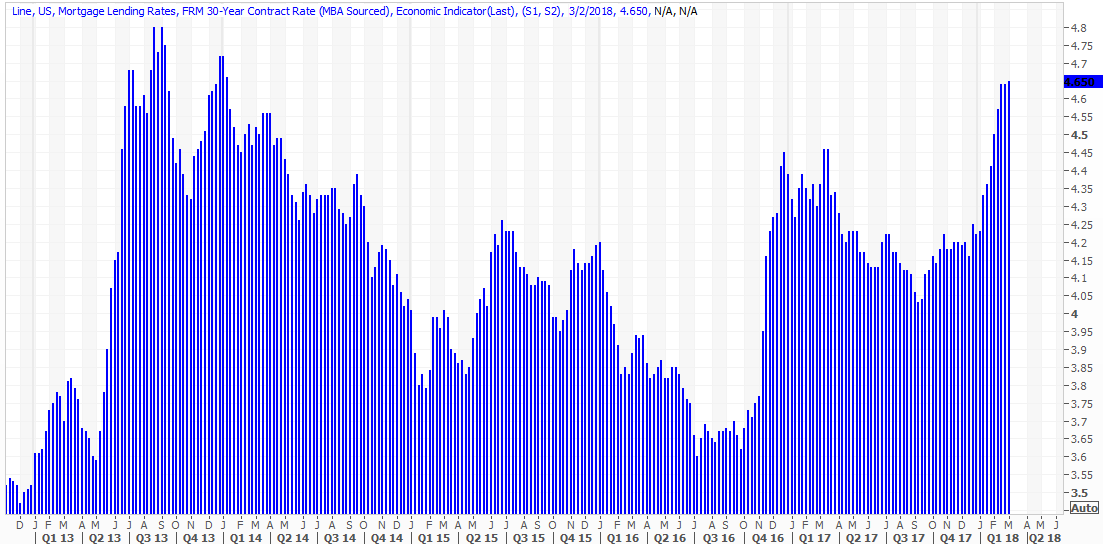

Interest rates have been steadily on the rise since bottoming in mid-2016. That broad uptrend heated up, in fact, in the latter part of 2017, when rising inflation finally forced the Fed to concede three to four interest rate increases were in the cards for the foreseeable future. Through the end of December, though, consumers brushed off higher interest rates (and higher mortgage rates in particular) because they were still quite low by historical standards. Things changed once the current quarter began, though, as the chart of 30-year mortgage rates below shows.

Click to Enlarge

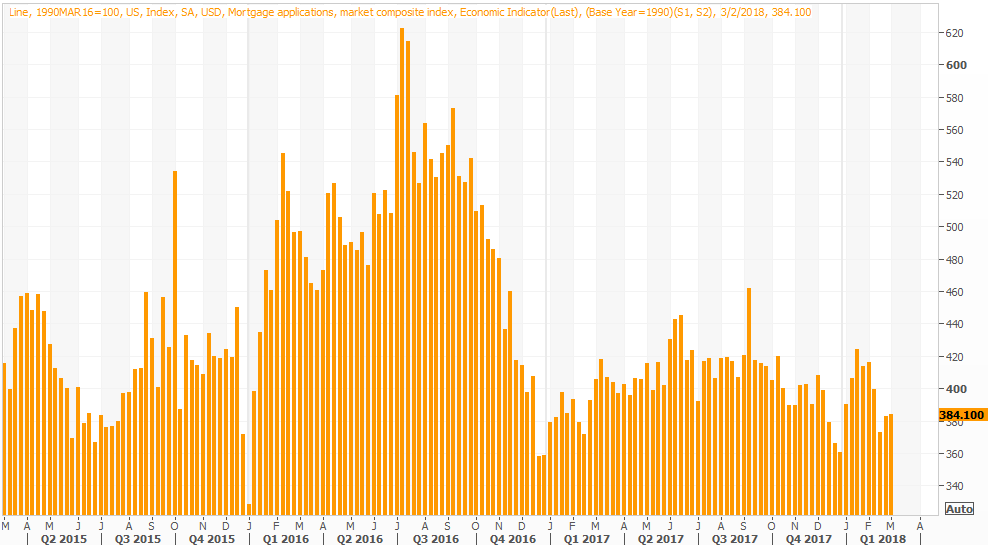

It’s a seemingly small move, but a move that crosses a major line for many would-be borrowers. And, yes, this has already crimped mortgage applications.

Click to Enlarge

It’s not devastating, but at current trajectories, it could be. When the average 30-year mortgage rate reaches 5%, a recent Redfin survey suggests that more than a fourth of people interested in buying a home would likely rethink their plans

. And given the Fed’s plans for later this year, 5% seems almost inevitable.

In its defense, Bank of America offers loans other than mortgages and higher interest rates translate into wider profit margins on things like consumer deposits and CDs, in addition to making lending a more profitable business.

Lending can only be more profitable in a rising-rate environment, however, if consumers and corporations are still borrowing. Though they’ve not stopped borrowing altogether, it’s worth noting that the relatively modest increase in interest rates in just a few weeks likely took a toll on all other lending activities as well. This could prove to be an unexpected drag on the current quarter’s results — and it’s a drag that could linger into 2018 and beyond.

A lack of demand is a problem B of A hasn’t had to deal with in a while, prompting questions about its lending business going forward — and now.

Bottom Line for BAC Stock

To be clear, the lending headwind — to the extent it’s blowing — isn’t just blowing against BofA. Rivals like Wells Fargo & Co (NYSE:WFC) and Citigroup Inc (NYSE:C) are facing the same struggle. I’m singling Bank of America out, however, simply because it’s my favorite name among all the major banks; I’ve pounded the table, bullishly, several times on BAC stock. It would be unfair to not offer this follow-up.

I’ll also add that, despite the headwind, not only is Bank of America still my top banking pick, I doubt a lending headwind will do any grave, long-lasting damage to BAC stock. The economic positives still outweigh the negatives.

Veteran traders know how this works, though. The financial media and its pundits love to write terrifying headlines about the smallest of red flags, and traders are all too happy to respond accordingly. It’s usually a temporary tumble, but a tumble nonetheless.

But knowing it’s possible beforehand makes it easier to ignore when the time comes.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.