Target Corporation (NYSE:TGT) is seeing its stock fall after it reported somewhat disappointing earnings results earlier this week. It’s got investors trying to balance the short-term situation (like comparable-store sales), while also contemplating its long-term outlook. It essentially boils down to: What is Target stock going to do to compete against Amazon.com, Inc. (NASDAQ:AMZN) and the rest of e-commerce?

All in all, Target earnings came up short by a penny per share versus expectations. Analysts were looking for $1.37 in earnings on revenue of about $22.5 billion. The company was able to grow sales 10.1% and beat estimates, hitting $22.77 billion in the quarter.

Further, the company’s 3.6% comparable-store sales results beat estimates of 3.4%. Management said the retailer had a late-quarter boost in sales momentum helping it to beat. Half of that comp number came from the 29% growth in digital sales for Target.

What To Do With Target Stock

Those were the quarterly results — and they were pretty good — but as we said, investors have to balance the short- and long-term strategies. With competitors like Walmart Inc (NYSE:WMT

) struggling with its e-commerce/bricks-and-mortar strategy, despite having deep pockets, how does a company like Target have a chance?

The problem is more about Amazon than any of its competitors. The reason? Amazon can go years without turning a real profit. Even now, its profit margin is a paltry figure just above 0% — and that’s only possible because of its Web Services business.

AMZN going years without profit would usually be a good thing for a WMT or TGT stock. But that’s not the case because Amazon investors shrug off the lack of bottom-line results and instead focus on the top line. In Bezos they trust. So long as Amazon is kicking in the door of its competitors, growing Prime, growing sales and making waves, investors will keep on cheering. Shares now sport a monstrous $745 billion market cap. It basically makes it impossible for traditional retailers to win, because one side of the market isn’t playing by the same rules.

None of that will stop Target, though. The company is upping its free two-day delivery service, pushing forward with store remodels and looking to improve its in-store pick-up and local delivery services.

The question is: Will it work? That’s where cash comes into play.

Target stock only has a $38 billion market cap. Despite this, TGT generates some serious cash, with operating cash flow and free-cash flow of about $7 billion and $4.5 billion, respectively. That’s more than enough to pour into its omni-channel efforts. But it can’t afford many mistakes.

Trading Target Stock

While Target continues to generate strong cash flows, earnings aren’t bad either. Analysts forecast earnings per share of $5.27 this year, up almost 12% year-over-year. That’s despite an expected increase of just 0.6% in sales for the year. But it’s worth noting that estimates call for earnings and sales growth of just 0.6% and 1.7%, respectively, next year.

On a valuation basis, TGT stock is not that bad. In fact, Target stock trades at just 13.5 times this year’s earnings estimates, a rather modest valuation. That’s especially true when considering its double-digit earnings outlook. Also worth considering is its 3.3% dividend yield. It’s not as jazzy as Amazon, but Target stock does have its own positive merits.

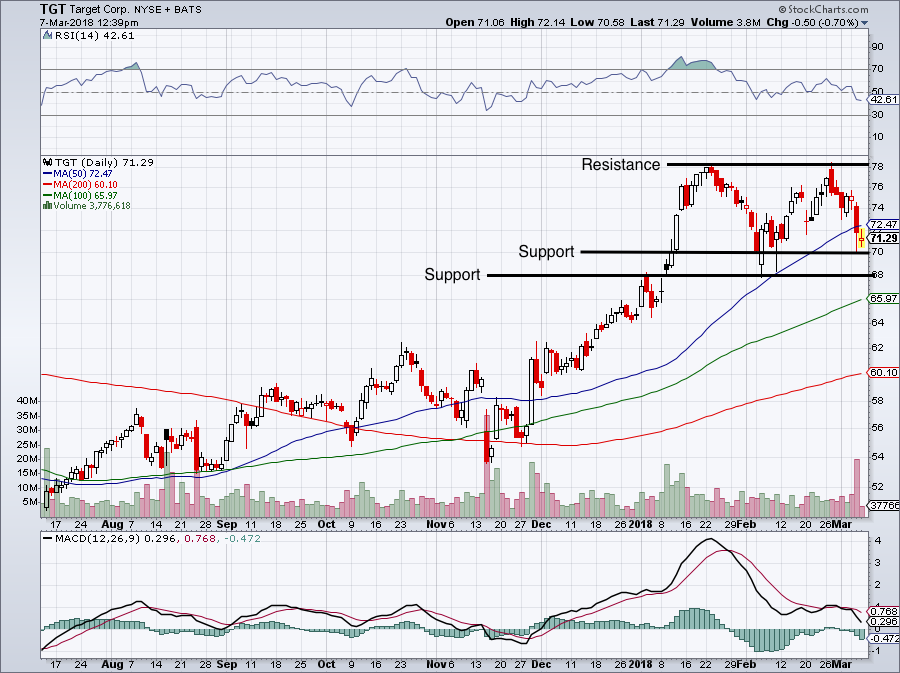

Click to Enlarge

There’s a surprising amount of support resting just below current levels in TGT stock. For instance, two levels of support sit at $68 and $70. Further, near $66 and trending higher is the 100-day moving average. That too should act as support should TGT stock continue to correct. About 10% above current levels rests resistance at $78.

Should all current levels of support fail, look for either the 200-day moving average or $62 to act as support, whichever comes first.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.