Gap (NYSE:GPS) couldn’t repeat the great, post-earnings performances of many of its peers. Whether that’s Macy’s (NYSE:M), Walmart (NYSE:WMT) or Target (NYSE:TGT), the retail sector has been strong this earnings season. Unfortunately for Gap stock though, shares tumbled more than 8.5% on Friday after the company released its second-quarter results.

The question now is, can shares still rally into the vital second half of the year?

As the U.S. consumer continues to do well in the midst of a strong economic backdrop, retailers are clearly mopping up their excess dollars. Will Gap remain a go-to name among shoppers and investors alike?

Gap in the Quarter?

Revenue of $4.09 billion came in $80 million ahead of estimates and grew 7.6% year-over-year (YoY). That helped fuel earnings of 76 cents per share, 4 cents ahead of expectations. Further, Gap reported comp-store sales results of 2%, ahead of the 1.5% estimate.

In fact, that was the company’s seventh consecutive quarter of positive comp-store sales, no easy feat for the retail environment over the last few years. Even though consensus expectations for the year call for earnings of $2.56 per share, management reaffirmed its outlook for $2.55 to $2.70 a share, with a midpoint that’s ahead of estimates.

Old Navy remains consistent but recoveries in Gap and Banana Republic are helping to drive these gains. Gross profit climbed 10% YoY, while gross margins jumped 90 basis points to 39.8%.

So far, it’s hard to see why shares took such a big dive. Maybe operating margins, which fell 220 basis points YoY to 9.7%. However, that’s largely to due to an accounting change that otherwise would have left operating margins practically unchanged YoY.

Valuing Gap Stock

Maybe Gap stock is too expensive, hence the selloff? Try again. Shares trade at just 11.5 times this year’s earnings, which are set to grow 20% YoY. Next year, analysts expect earnings growth of 5%. Not robust by any means, but back-to-back years of positive growth at a sub-12 times earnings multiple is far from unattractive.

Further, analysts expect revenue to grow 4.5% and 2% this year and next, respectively Gap stock also pays out a 3.3% dividend yield.

It may be hard to call the retailer great, but at the very least we can say it’s pretty good. With its low valuation and dividend, investors have a reason to stick with it. Or at the very least, not sell it down by almost 10% on better-than-expected quarterly results. That was undeserving.

Trading Gap Stock

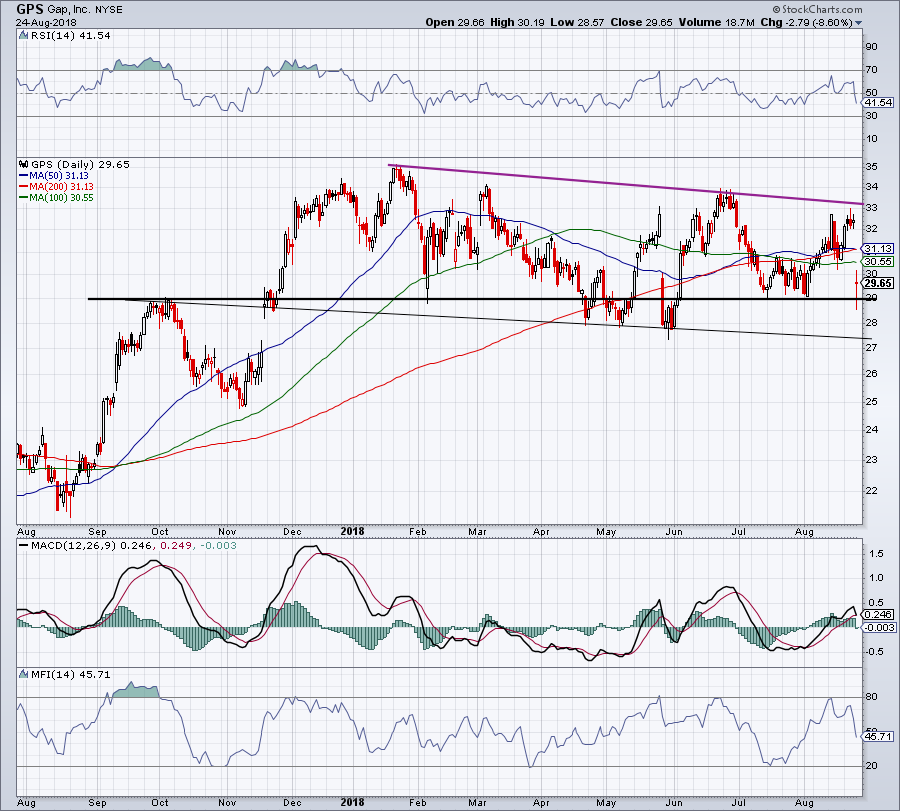

Click to Enlarge

Now below all three major moving averages, it may be hard to see where Gap stock has upside. Over the last 90 days, the average price target is near $38.50, implying more than 30% upside from current levels.

The highest price target (from Jefferies analysts in June) sits at $50, implying almost 70% upside.

Seeing shares hold $29 as support was a good sign. However, a drop to downtrend support near $27.50 would have made for a highly attractive buying opportunity.

Conservative bulls will want to see this $29 level hold, while aggressive bulls may consider using Friday’s low as their stop-loss. Both groups can consider buying if we see a dip to deep support.

In order to see Gap stock climb to those analyst targets though, it will need to close above downtrend resistance (purple line).

Shares rallied hard in the five trading sessions leading up to Friday’s earnings release. Giving up some of those gains would have been acceptable. Nearly gapping below the monthly low and opening below all three major moving averages seems like overkill.

Traders can keep it simple: Over Friday’s high and GPS stock is a long, below and stay away. If we get a rally, look for a gap-fill up to $32.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.