It certainly is tempting to dive into trading CME Group (NASDAQ:CME) stock now. CME stock surged on Thursday, reaching a new 52-week high. It has followed through on such moves multiple times in the past.

This may be a time, however, when it’s smarter to pass up the apparent opportunity. CME stock is overvalued and overbought at the worst possible time. Specifically, its sales and earnings growth are both on the cusp of slowing down. That’s a problem simply because CME’s growth, rather than the valuation of CME stock, has been driving the shares upward for the past couple of years.

Two Charts Tell the Story

In another time and different circumstances, the 3% surge of CME stock would be alluring. CME stock had been working its way higher almost the whole year… even when the rest of the market wasn’t. And with Thursday’s big gain, CME stock seemingly broke out of a mostly-sideways trading range. That kind of move has flagged major advances by CME in the recent past.

Click to Enlarge

Maybe this move will turn out, like the others, to be the beginning of a major advance. The odds of that happening aren’t very high, however, in light of the way that the bulls have overplayed their hand.

CME operates futures and options exchanges. It’s in the capital markets business, like Intercontinental Exchange (NYSE:ICE) and Nasdaq (NASDAQ:NDAQ). But because of CME’s focus on futures, it works more with institutions than “retail” investors. Farmers and oil companies, for example, use futures not so much to speculate, but to hedge against volatile commodity prices. Trading by institutions tends to be a little more predictable and a little less volatile than trading by individuals.

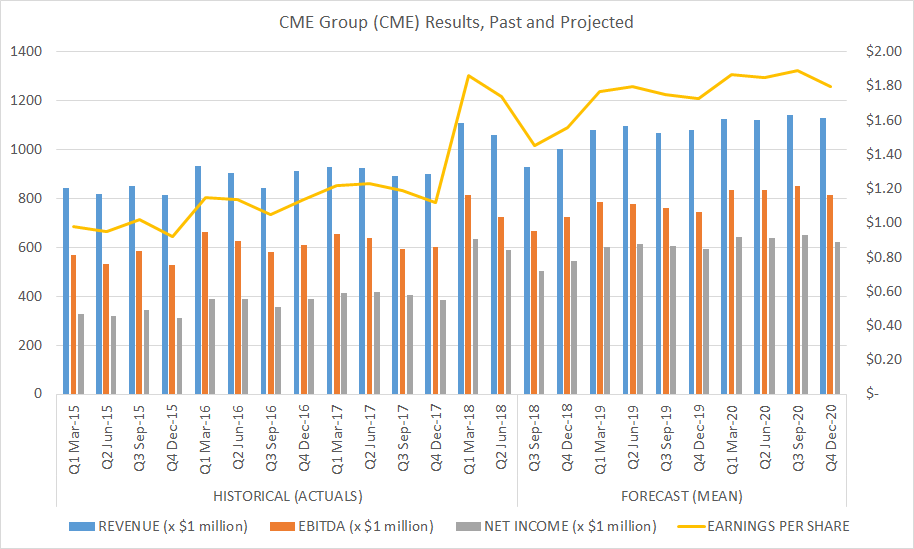

But the problem is that while accelerated economic growth (and uncertainty) since early 2017 has decidedly cranked up trading activity on CME’s exchanges, causing its revenue to rise, that trend probably won’t continue going forward. Most analysts agree with that assessment. The chart below tells the tale.

Click to Enlarge

For the record, the surge in CME’s revenue and profits in Q1 wasn’t helped by an acquisition. It was purely organic growth, largely prompted by a confluence of tariff threats, continued inflation and economic growth.

Notice, though, that CME’s revenue has dropped in Q2, and it doesn’t appear that CME Group is going to report any meaningful year-over-year growth in the foreseeable future. In Q3, total trading activity was down about 1% year-over-year. That lack of growth is strange, given the strong revenue gains in Q1.

And CME stock isn’t exactly priced for just “a little growth.” In fact, CME has a fairly frothy forward price-earnings ratio of 25.4. For perspective, Nasdaq stock currently has a forward-looking price-earnings ratio of just 16.3 and Intercontinental Exchange stock is trading for 19.7 times next year’s projected earnings.

The Bottom Line for CME

Don’t misunderstand my thesis. More economic growth will drive higher trading volume for CME. And, as was seen during the 2008 financial crisis, a faltering economy also spurs increased trading volumes. The 2014-2015 oil meltdown even proved beneficial for CME, as oil companies cashed in their price hedges and sought to prepare for a then-unclear future. Ironically, it’s a meandering, modest, stable environment that tends to be the toughest on CME Group, but that’s the sort of environment we’re in as we near the end of 2018.

That’s not the kind of environment which those who are bullish on CME are seeing, though. They’re betting that tariff wars and inflation will spur even higher trading volumes. As a result, they’re paying too high of a price for CME stock.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.