Even when the internet was no longer new, the idea of multi-user access to the same online document seemed foreign… maybe even a little unnecessary. After all, documents could be readily exchanged back and forth via e-mail. What would be the point?

A little over 10 years ago, Dropbox (NASDAQ:DBX) began to unwind that erroneous assumption.

Now? Mission accomplished.

And yet, not only is Dropbox still a mostly unknown entity, DBX stock still ranks as one of the market’s most overlooked and underestimated opportunities. Three charts should at least start to correct that problem, likely leading investors to wonder why in the world Dropbox stock has been steadily selling off from June’s peak after going public in March.

The Pictures Tell the Dropbox Story

Truth be told, organizations of all sizes could accomplish much of the same functionality as Dropbox using the free Google Drive, from Alphabet (NASDAQ:GOOGL) or paying to use the Office-Online platform from Microsoft (NASDAQ:MSFT). Somehow, though, a dedicated file-sharing platform like Box (NYSE:BOX) or Dropbox seems far better equipped to handle the task. And of the singularly focused platforms, Dropbox is arguably the best when it comes to letting many users view and update the same document. There’s a reason customers are willing to pay for the service.

To that end, the company is still adding paying customers, and at its current rate of growth will soon reach a critical mass in terms of profitability. That’s the part of most interest to investors… not what’s already occurred, but what’s about to happen.

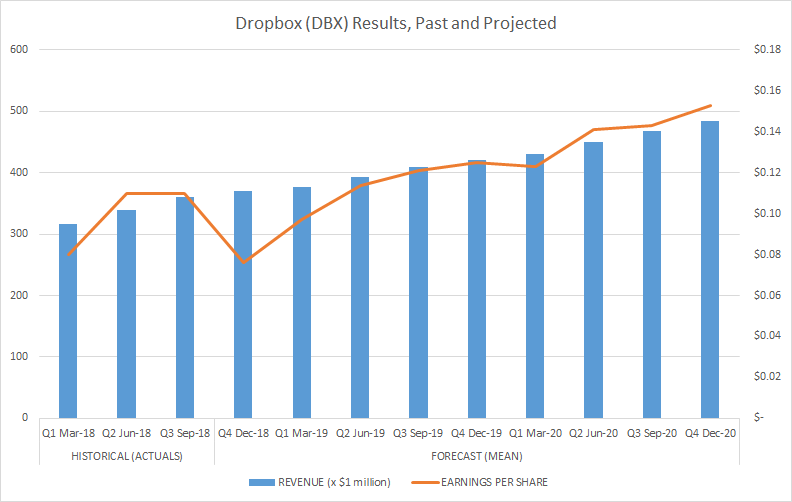

The chart below tells part of the curiously compelling tale. Analysts are only calling for revenue growth through 2020 that extends the trend already underway. Better still, per-share earnings are expected to nearly double between the current quarter and the final quarter of 2020.

Click to Enlarge

It’s hard to doubt the lofty growth targets in light of the fact that Dropbox’s sales are largely recurring revenue. Once a customer is brought into the fold, they tend to stick around. Assuming the company’s fixed costs remain fixed, any scale-up in the top line is magnified on the bottom line.

But does the anticipated sequential drop in per-share profits for the quarter currently underway suggest this year’s swell of earnings was only a temporary stroke of luck? Not really.

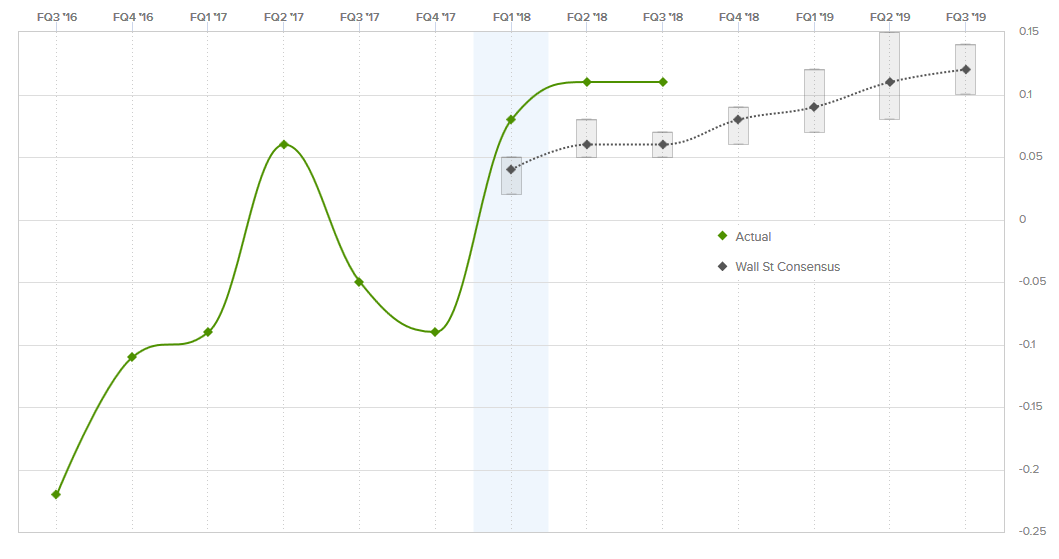

Dropbox is a relatively new stock; since IPOing in March, DBX shares have lost almost 18% versus the Nasdaq Composite’s 6.2% gain. The dozen or so analysts who now follow it have only been tracking and forecasting estimates for three quarters now. And so far, they’ve underestimated how profitable the organization is.

A chart from Estimize, clearly makes the point. Dropbox has handily topped earnings estimates in its past three quarters, in one case more than doubling the bottom line Wall Street pros were modeling. It’s likely the Q4 estimate of eight cents per share once again understates how profitable Dropbox will be… by a lot.

Click to Enlarge

Assuming the company continues to beat estimates, DBX stock is actually priced at only about 30 times 2019’s likely earnings rather than the forward-looking P/E of 55 based on analyst outlooks that are simply too low.

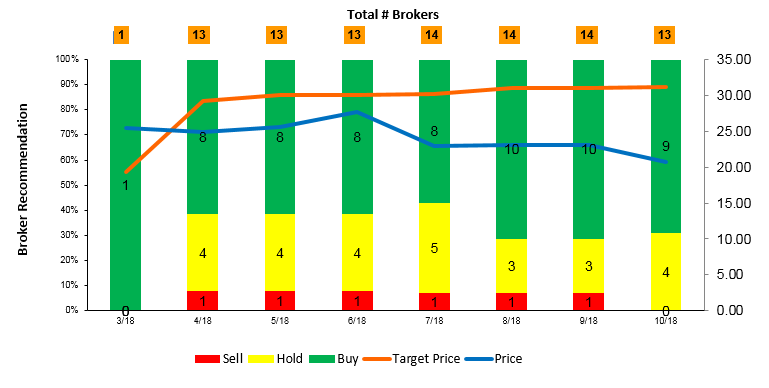

Finally, and perhaps most important, while the equities research community is apt to still be underestimating Dropbox’s profitability, they’ve not been unwilling to maintain lofty target prices on DBX stock even though it’s been trending lower since June. Indeed, the consensus call on the shares has actually become even more bullish in the meantime.

Click to Enlarge

This degree of conviction against the tide (and in the face of criticism) speaks volumes.

Bottom Line for DBX Stock

Does all of this add up to a guarantee that Dropbox has already bottomed and will finally begin to trend higher from here? No, far from it. There are no guarantees in this business, and arguably, investors — and analysts for their part on earnings estimates — should have had their “aha” moment weeks ago. If the crowd has decided it’s going to push DBX stock lower, then there’s little to be gained by fighting the tape.

On the other hand, in the end, fundamentals always win. The game here isn’t figuring out if Dropbox will finally turn. It’s only a matter of when. The company’s clearly doing its part, and it’s not like analysts don’t see it, even if they’re still underestimating it.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.