Some of the concerns surrounding Alibaba (NYSE:BABA) stem from a slowing down of the Chinese economy. The recent figures show 6.6% GDP growth rate in China which is the lowest rate in 28 years. More important, the forward estimates point to a further slowdown in the growth rate to below 5% in the next few years. However, Alibaba stock can still show bullish momentum as the company delivers 40% to 50% revenue growth rate using new services which are added to the platform.

Alibaba stock will also benefit from a shift to organized retail and specifically online platforms in China.

Alibaba’s cloud platform has shown a growth rate of 84% in the recent quarter. The revenue share of this fast growing segment is 6%. Alibaba is also diversifying to other non-core commerce services and is expanding in international regions.

These initiatives should allow the company to report healthy growth rate in the near term. The valuation multiple of Alibaba’s stock is still quite low for a company rapidly increasing the top line and bottom line.

Slowdown in China’s Economy

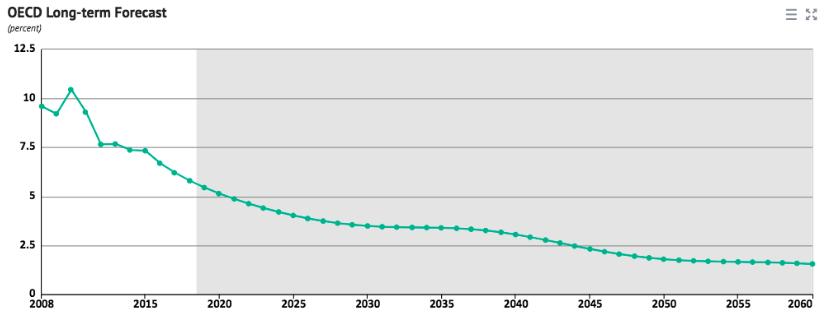

There has been a gradual slowdown in China’s economy in the last few years. The recent GDP growth figure is not surprising as most of the predictions were estimating growth of 6.5%. According to economists polled by Nikkei, the growth rate in 2019 could further fall to 6.2%.

The OECD estimate for China’s economy points to further deceleration. We can see from the above chart that the growth rate falls to below 5% by 2021-2022. This can lead to further concerns about the long term potential of Alibaba stock. However, the company’s growth is quite detached from the growth rate in the broader economy.

The growth in retail consumer goods was 9.0%. In a recent report, eMarketer has forecasted that the retail ecommerce sales will grow by 30.3% in 2019. This will increase the market share of online retail to 35% in the total retail segment.

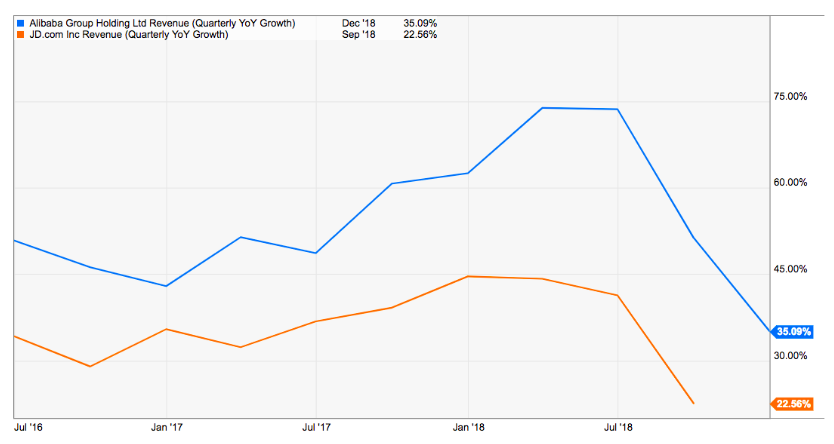

Alibaba’s growth has consistently been greater than JD.com (NASDAQ:JD) which is main ecommerce rival of the company.

Hence, the growth rate of Alibaba should easily exceed the broader online retail sales.

Other Growth Options

Alibaba has been expanding into new services with massive investments. It has built a strong delivery service with Ele.me which competes with Tencent’s (OTCMKTS:TCEHY) Meituan. Meituan has a market cap of $40 billion.

Source: Bloomberg

Source: Bloomberg

Besides food delivery, Alibaba is using the Ele.me platform to add new services. It has recently entered into partnership with Starbucks to deliver coffee. Alibaba has also entered pharmacy delivery segment which should allow rapid increase in transactions and sales.

The international growth is an important part for future growth potential of Alibaba stock. The company has spent billions of dollars in acquiring and investing in different regions.

Alibaba has acquired Lazada and Tokopedia which are the leading ecommerce platforms in Southeast Asia. It is also a major investor in Paytm which is the biggest digital wallet platform in India. In the last funding round in which Warren Buffet participated, Paytm was valued at $10 billion.

Alibaba and Cloud Computing

In the recent quarter, Alibaba’s cloud computing revenue increased to $962 million which was an 84% growth on a year-on-year basis. This also increased the revenue share of cloud computing to 6%. As the revenue base of this segment increases, it will have a bigger impact on the total revenue growth number.

Valuation

Alibaba stock still is quite cheap when we look at the revenue growth rate and future potential in various segments.

We can see that despite trade tensions and tariffs, the forward revenue estimates of Alibaba did not decline significantly throughout 2018. The forward PE ratio of Alibaba stock is close to 30 which should be quite cheap for a company growing its revenue at close to 40%.

Alibaba could also have an upside surprise on margins as the cloud computing segment is currently showing negative 4% EBITA margin. This is quite low compared to Amazon’s (NASDAQ:AMZN) AWS operating margin of 29.3%. As the cloud revenue increases, Alibaba should be able to get better pricing power which can increase margins rapidly.

Investor Takeaway

While China’s GDP growth rate is slowing, Alibaba has a number of growth levers to expand the revenue base as well as margins. Considering this, the valuation multiple of Alibaba stock is quite low. Alibaba should be able to add new services to its delivery platform. The revenue growth rate of Alibaba has been more than its main ecommerce rival, JD.com, for the past few quarters.

A higher market share within the ecommerce space and rapidly expanding services should help in improving the long term growth potential of Alibaba stock.

As of this writing, Rohit Chhatwal held no positions in the aforementioned securities.