Apple (NASDAQ: AAPL) has been ramping up its research and development spending in order to gain a competitive advantage against its rivals.

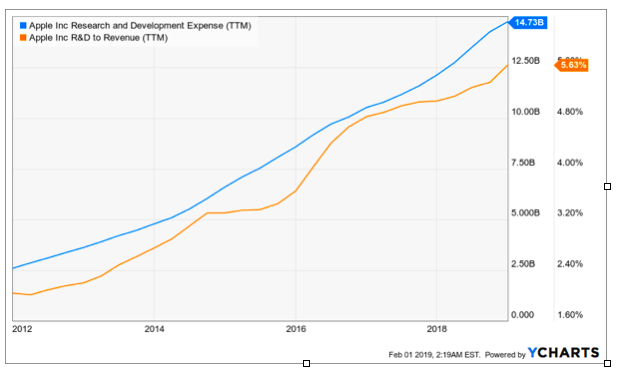

In its quarter that ended in December, Apple’s spending on R&D surged 14.5% year-over-year to $3.902 billion. R&D as a percent of revenue reached 5.63%, up from 2.1% in 2012. The continuous growth of Apple’s R&D, in conjunction with its stagnant or declining revenue base, will hurt its operating margin in the near future.

Declining operating margin is another headwind for Apple stock. The company’s operating margin has declined for 12 out of the last 13 quarters. In the December quarter, its operating margin fell by 2.07 percentage points year-over-year.

The increases in Apple’s R&D spending are definitely positive for the long-term outlook of Apple stock. But AAPL needs to come out with some solid products and services which can meaningfully raise its top and bottom lines.

Another Quarter of R&D Expansion

Fig: Growth of R&D spending under Tim Cook.

There has been a substantial increase in R&D spending since Tim Cook became CEO of Apple. The company’s R&D as a percentage of its revenue has increased from 2.1% to 5.63% during Cook’s tenure. In the past few quarters, R&D expenses have been higher than the total dividends paid on Apple stock, even as AAPL has raised its dividend meaningfully. In 2018, the total dividends paid to the owners of Apple stock came to $13.94 billion, while R&D expenses totaled $14.7 billion.

It can be argued that AAPL is investing in its long-term performance, instead of focusing solely on returning more money to the owners of Apple stock. Although I have an “underperform “rating on Apple stock, the fact that it’s investing more in R&D is certainly positive. However, the other side of the coin also needs to be analyzed. In the past few years, several competitors have closed the gap between their products and those of Apple.

Headwinds in Europe And Other Overseas Markets

Apple’s competition from Chinese OEMs like Huawei, Oppo, and Xiaomi has been especially intense All these players have been able to launch smartphones with low bezel counts and many new features within a short time of the launch of Apple’s iPhone X.

These companies are a big reason why AAPL is having a hard time growing its market share in China and other emerging markets. All these companies are also aggressively trying to improve their market share in Europe.

Fig: Apple’s net sales by regions

Apple’s net sales in Europe declined from $21.05 billion in the quarter that ended in December 2017 to $20.36 in the quarter that ended in December 2018.

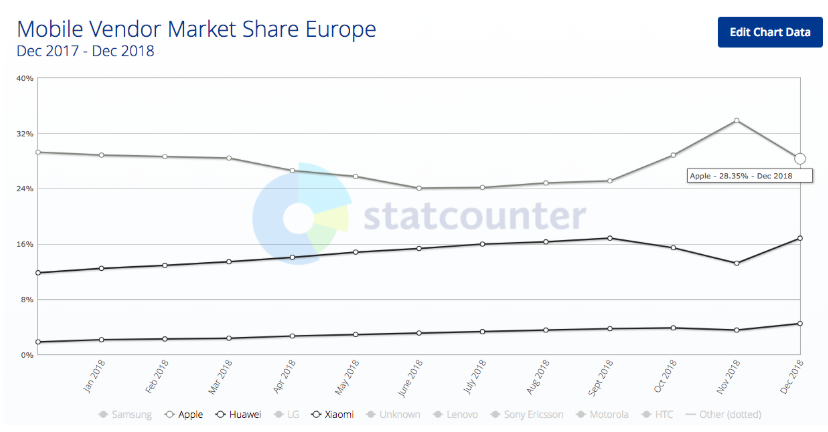

Fig: The market share of Apple, Huawei and Xiaomi in Europe over the last 12 months. Source: Statcounter

We can see from the above chart that the market share of both Huawei and Xiaomi in Europe has steadily risen over the last 12 months. Huawei’s market share increased from 11.8% in December 2017 to 16.9% in December 2018. Xiaomi’s market share has increased from 1.8% to 4.5% during the same period. These companies are increasing their market share in Europe even though the region’s smartphone market has already been saturated. Apple’s European market share, by contrast, dropped from 29.3% to 28.3% during this period.

The European market share of Huawei and Xiaomi can rise rapidly as they launch their 5G devices this year while AAPL delays the launch of its 5G smartphones until 2020.

Europe is a very important market for Apple. It accounts for 24% of the company’s total revenue. The recent decline in Apple’s revenue from Europe shows that AAPL faces headwinds in this region also, along with the difficulties with which it’s contending in China and other emerging markets. Of course, Apple’s struggles in those regions don’t bode well for Apple stock.

The Impact on Apple’s Operating Margin

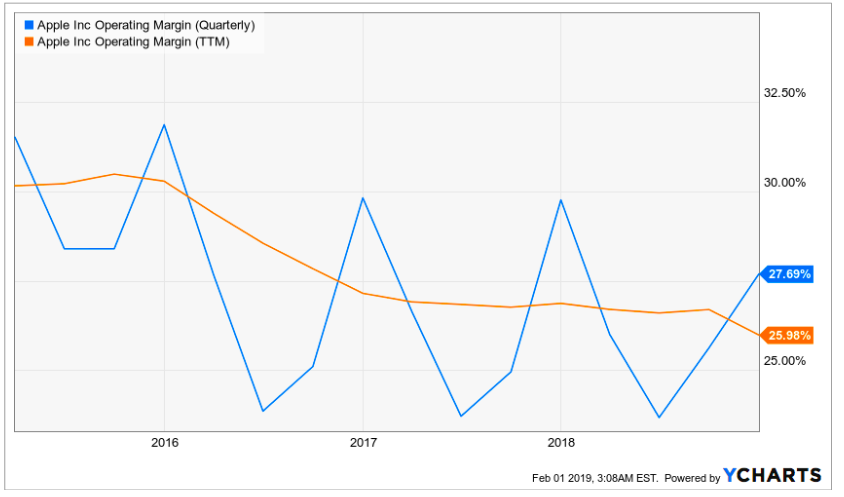

Apple’s operating margin has been declining for quite some time.

The company’s annual operating margin declined from over 30% in 2015 to 25.98% in 2018. The company’s operating margin declined from 29.76% in the quarter ended in December 2017 to 27.69% in the quarter ended in December 2018.

A major reason for that decline is the fact that, in order to sell more iPhones, AAPL has been forced to offer higher discounts on the devices . Unless the company can come out with a revolutionary product or service, its operating margin will probably decline further in the near-term.

Due to Apple’s higher discounts and the increases in its R&D spending, the company’s annual operating margin could decline to a range of 20%-22% by the end of 2020. As a result, the company’s net-income growth, which has been supported by lower taxes, will face a major headwind.

Within the next few quarters, earnings per share of Apple stock will be negatively impacted by this trend. Even if AAPL buys back a huge amount of AAPL stock, its rapidly declining operating margin will inevitably hurt its EPS growth. Investors who are looking to hold Apple stock over the long-term should take this into consideration.

The Bottom Line on Apple Stock

Apple has been increasing its R&D spending for the past few years. In 2018, the company spent close to $15 billion on R&D. At the same time, Apple’s market share in China and Europe is eroding as Chinese OEMs are closing the gap with Apple’s iPhone. Meanwhile, the company’s operating margin has declined as its discounts and R&D spending have increased.

Unless AAPL can come out with a hit product or service, its margins will continue to erode, hurting Apple stock.

As of this writing, Rohit Chhatwal held no positions in the aforementioned securities.