It’s anything but a traditional investment because World Wrestling Entertainment (NYSE:WWE) is anything but a traditional company. Wrestling in well-conceived costumes … ’nuff said. But for investors that don’t have to plug into orthodox opportunities, WWE stock may offer surprising potency.

That’s because next year’s big projected revenue growth is expected to translate into even more profit growth.

And, MKM Partners analyst Eric Handler thinks the company will be able to meet those lofty targets for four very specific reasons.

Without detailing exactly why, the analyst community as a whole seems to agree that this one-of-a-kind company is on the verge of a big growth spurt.

Beaten But Not Broken

It may be the premier (and arguably only) name in wrestling. But like other entertainment organizations, WWE had to contend with increasing competitive pressures.

Those threats include a universe of video content from Netflix (NASDAQ:NFLX), an ever-growing Walt Disney (NYSE:DIS) and ultra-realistic video games from the likes of Activision Blizzard (NASDAQ:ATVI). Plus, the associated rise of e-sports tournaments offer a nearly-identical experience to WWE events.

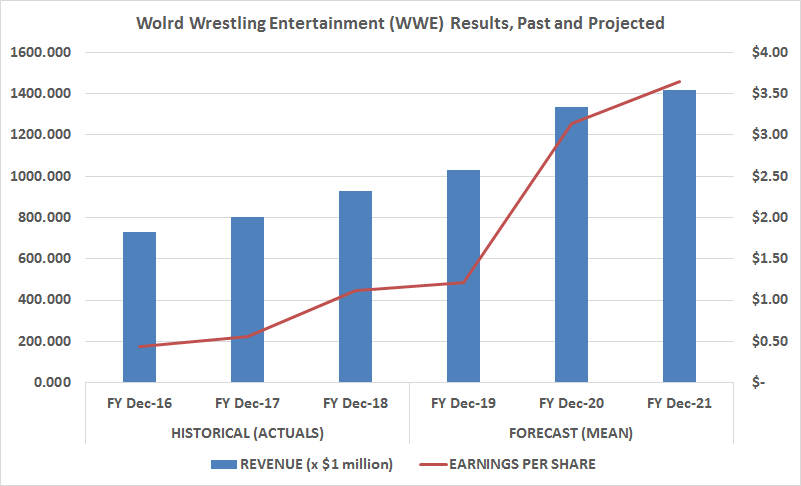

Those distractions didn’t crimp revenue when they seemingly should have. World Wrestling Entertainment managed to grow its top line quite measurably between 2014 and 2018. Keep in mind that was when competition was at its fiercest.

That’s not the case for

income, though. Profits began to deteriorate in 2012, and turned convincingly negative in fiscal 2014. Back then, the organization booked a loss of 40 cents per share of WWE stock due to an unexpectedly unfruitful deal with broadcast partner NBCUniversal for that year.

That was the same year WWE attempted to deliver a standalone streaming version of its product. However, they found a lackluster response from consumers who had myriad alternatives like new video games and streaming video options. The web has democratized distractions.

Matters have taken a turn for the better in the meantime, with World Wrestling Entertainment swinging back to profitability. In fact, the bottom line has never been better. But it’s about to explode, however, if MKM Partners’ Eric Handler’s outlook is on target.

Catalysts Ahead

In a note penned and posted earlier this week, Handler explained: “In our view, WWE has the most financial upside potential over the next 3-5 years, relative to expectations, within our coverage universe.”

It wasn’t a mere gut feeling, either. MKM’s Handler cited four specific catalysts that could accelerate revenue and profit growth for the timeframe in question.

One of those catalysts is a trio of new international TV deals in China, the Middle East and India. Whereas wrestling may be reaching a peak in the United States, it’s just entering a high-growth pace in other parts of the world. To spark further interest, organizers feature home-grown wrestling stars on the WWE circuit.

Handler also sees World Wrestling Entertainment as having a better feel for how to create and monetize content. The analyst believes the company will reboot the WWE Network in the foreseeable future. In the meantime, management might start to use the third filmed hour of its popular SmackDown events that only air two hours of content. That might add about $50 million in annual revenue.

Click to Enlarge

Other analysts that follow the company don’t disagree with MKM’s enthusiasm either, if their collective outlooks are any indication. The professionals ultimately expect to see earnings of $3.64 per share in fiscal 2021. This would extend an earnings recovery that’s been underway for a while now.

Bottom Line for WWE Stock

It’s still a name many investors refuse to own, simply given the concept. It’s miles from being an “old school” blue chip. Eventually, the rest of the world will grow tired of men – and women – in colorful tights pushing each other around.

Or, maybe the world won’t tire of it at all.

World Wrestling Entertainment has been around since 1979. The league has found a way to grow its audience for forty years, while keeping fans interested and engaged. If it was going to flame out, it likely would have done so by now. Indeed, with the international community just now opening up in earnest to WWE, it may easily have many more years of runway to move along before saturation becomes a threat to growth.

In that light, investors may want to mull a position in WWE stock, disregarding how its profits are produced. Instead, they should focus on the fact that it’s capable of growing the bottom line when other traditional names can’t. There’s a reason it’s been able to keep audiences interested in a sea of alternative entertainment.

Analysts say WWE stock is worth $96 per share, up more than 10% from the current WWE stock price. As shares gain in value though, the consensus target will likely grow.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.