Back in late January, chipmaker Intel (NASDAQ:INTC) reported ugly fourth-quarter numbers and delivered below-consensus guidance, all against the backdrop of a global economic slowdown. The implication for Intel stock was clear.

Alongside the global economy, the global semiconductor industry is cooling, and that is creating a drag on Intel’s growth rates which will last for the foreseeable future. Investors weren’t too happy about the news, causing Intel stock to drop from $50 to $46 in a few days.

That selloff of INTC stock was a buying opportunity. Ever since, the shares of Intel have rallied in a nearly straight-line fashion towards $53, mostly because global economic and semiconductor fundamentals have shown signs of improvement over the past several months.

As a result, it looks like, despite the bad guidance that INTC provided back in late January, it will actually report not-so-bad first quarter and 2019 numbers. Investors are consequently repricing the shares, and INTC stock is in rally mode.

But the growth of the semiconductor market is still normalizing lower, and will likely continue to do so for the next several years as supply builds and global economic expansion slows. Consequently, although INTC’s fundamentals are improving, it will remain a stable but low growth company for the foreseeable future.

A stable but low-growth trajectory isn’t priced into Intel stock. Yet. But investors will start to question the valuation of INTC stock above $55. As a result, I like Intel stock until it reaches $55. If the stock pops significantly above that level soon, I’ll look to do some profit-taking.

INTC’s Fundamentals Are Improving, But Not Tremendously

The fundamentals underlying Intel stock have materially improved over the past several years.

For starters, although the yield curve has inverted, the global economy has actually shown signs of bottoming and improving in 2019, led by a China rebound, less severe trade and foreign-exchange headwinds, continued strong labor markets, and the recovery of U.S. consumer confidence, housing data, and financial markets. Those economic improvements have helped stimulate demand in the semiconductor market.

Meanwhile, it appears that some chipmakers aggressively cut prices in Q1 to accelerate inventory clearing, and consequently, many believe that the global semiconductor supply glut of late 2018 is already coming to an end. Indeed, industry sources are saying that NAND flash prices will fall at a slower pace in the second quarter than in previous quarters, implying that the market has already bottomed and is now starting to rebound.

This is all good news for INTC. Furthermore, Intel finally has a permanent CEO in former CFO Bob Swan, has landed some big deals with professional soccer clubs, and is making aggressive pushes on the 5G front.

All together, the fundamentals supporting Intel stock have dramatically improved over the past several months. Having said that, the fundamentals of Intel stock still aren’t super rosy. The global semiconductor is due for a downward correction, based on

historical sales trends,. Moreover, with the global economy slowing, it looks like macro growth going forward will be slower than what we’ve seen over the past few years.

So INTC looks poised to be a slow and steady grower over the next several years. That growth trajectory isn’t priced into INTC stock. Yet. But the valuation of Intel stock is starting to look somewhat full.

The Long -Term Growth Trajectory Supports a $55 Price Tag

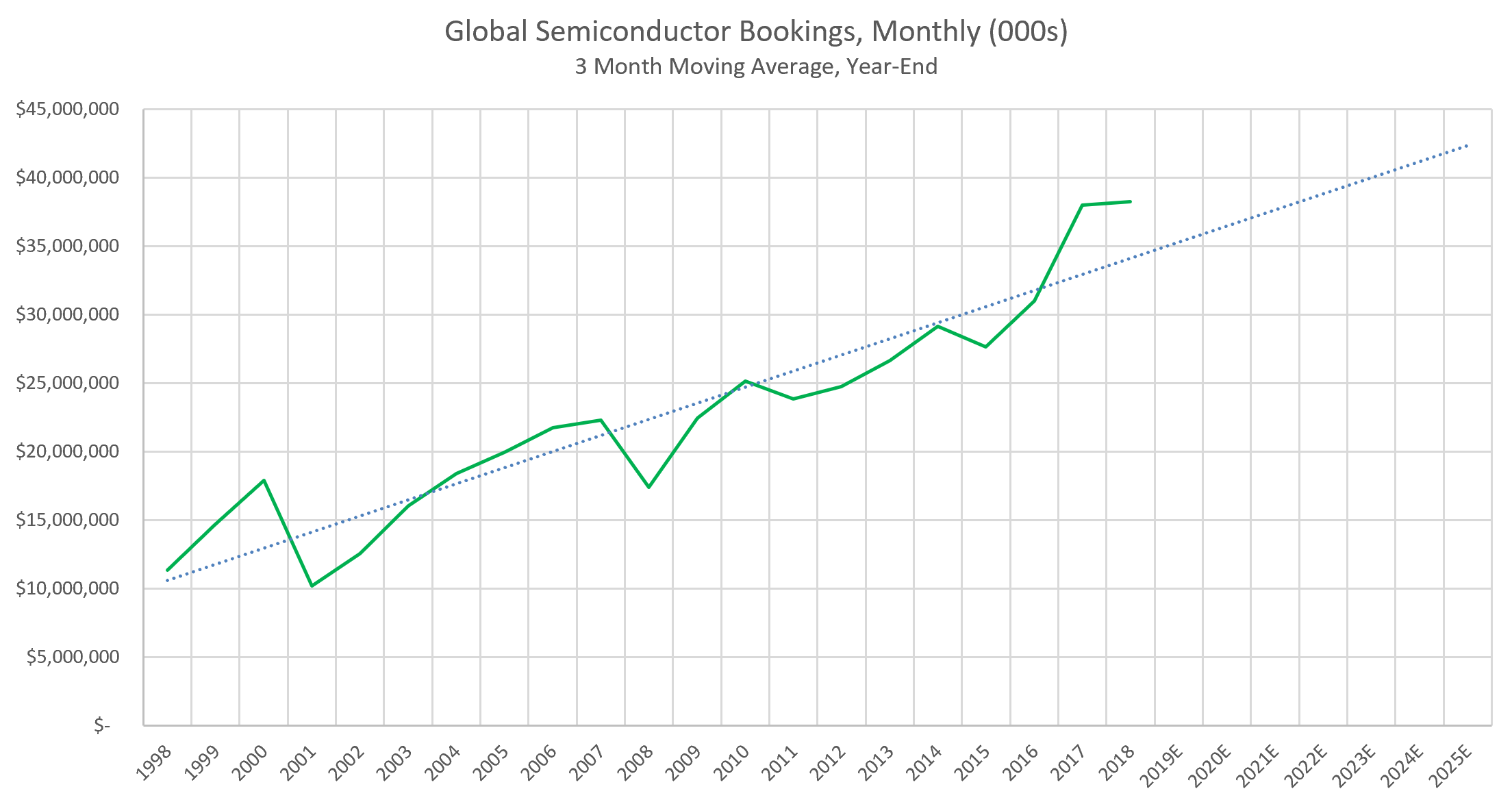

According to numbers from the Semiconductor Industry Association, global semiconductor sales have risen at a 6% compounded annual growth rate over the past 20 years. During that same stretch, Intel’s sales have risen at a 5% compounded annual growth rate, or roughly the same pace.

Moreover, after running simple trend-line analysis on SIA’s numbers, it’s easy to see that the growth of the semiconductor market is currently higher than average. This makes sense. The market has benefited from strong demand tailwinds in AI and data over the past several years, and those strong tailwinds have combined with limited supply to create strong growth. AI and data demand tailwinds will persist. But, inevitably, supply will pick up, and that will provide a drag on growth. Demand will also be somewhat weighed down by slowing global economic expansion going forward.

Consequently, assuming the semiconductor market normalizes back to trend, then sales across the whole market should rise roughly 1.5% per year into 2025. Intel, with its leadership position in important markets like data center and Internet of Things, should be able to grow revenues at roughly the same rate as the overall market. So Intel projects as a 1.5% annualized revenue grower over the next several years.

Assuming gross margins continue to gradually expand alongside the company’s data-centric pivot, and its operating-expenditure rates continue to fall slightly as it grows, then Intel should be able to generate earnings per share of about $5.75 by fiscal 2025. Based on the average forward price-earnings multiple of semiconductor stocks, which is about 14, that implies a reasonable fiscal 2024 price target for INTC stock of over $80. Discounted back by 7.5% per year (2.5 points below my normal 10% discount rate to account for the stock’s stable dividend yield), that equates to a fiscal 2019 price target for Intel stock of just over $56.

The Bottom Line on Intel Stock

Intel stock is a long-term winner, thanks to the company’s leadership position in important, continuous- growth markets. But even long-term winners become overvalued from time to time. If Intel stock continues on its upwards path, then it will start to hit valuation friction north of $55. Consequently, the best plan of attack with Intel stock is to trim as it passes above $55 and add if it comes back down to $50 or lower.

As of this writing, Luke Lango was long INTC.