While we’ve seen a robust recovery in the stock market, many investors expected more out of big tech. Companies like Apple (NASDAQ:AAPL), Amazon (NASDAQ:AMZN), Alphabet (NASDAQ:GOOGL) and Microsoft (NASDAQ:MSFT) have done well, certainly, but they have not been the market leaders many would have thought on a ~20% rebound in the S&P 500. While Amazon is up about 24% in that span, AAPL, GOOGL and MSFT stock are up about 18% apiece.

Again, that’s not bad. But we’re seeing FAANG and Microsoft simply match the market’s performance, not lead it higher like we’ve seen in years past. That could either bode quite well for investors as a rotation into these large-cap names could drive even more upside. On the downside, if these names continue to track the S&P 500 and Nasdaq,

it could spell trouble moving forward.

Finally — and, admittedly, this is a bit of speculation on my end — these names could act as a “source of funds” when some of the larger IPOs come down the road later this year. Investors may not need to sell Apple or Microsoft stock to free up extra funds for Lyft. But what about fund managers looking for a $1 billion+ stake in Uber, which is likely to eclipse the $100 billion market cap threshold when it debuts?

What about Airbnb and Palantir, two names that could easily push past $40 billion (the latter already has). There’s a number of $5 billion to $10 billion names in the pipeline too. It doesn’t mean big tech will get hit, but it’s something to think about.

Valuing Microsoft Stock

Some people may be turned off by Microsoft — which is quietly holding the top spot as the most valuable publicly traded company — because of its seemingly high valuation. But I don’t think that should be the case. The company is incredibly consistent and has several additional assets that warrant a premium.

First, analysts expect double-digit sales growth for the rest of this year and next year. Estimates call for 12.4% growth this year and 10.4% in 2020. The same can be said for earnings growth, with estimates calling for 14.2% growth and 12.6% growth this year and next, respectively.

Based purely on the growth, some might argue that MSFT stock is not worth 25 times this year’s earnings. But then you consider the fact Microsoft has beat earnings estimates for 14 straight quarters. Or the fact that it has $127.6 billion in short-term cash and investments vs. just $4.9 billion in short-term debt. Or that its total current assets outweigh total current liabilities $156.8 billion to $50.3 billion. Then, one realizes just how powerful this company is from a balance sheet perspective.

While free cash flow has stagnated over the last 12 months, the trailing 12 months of operating cash flow (OCF) has solid growth. Up about 10% over the past year, MSFT has more than $46 billion in trailing OCF. That figure is up almost 45% over the past three years.

Microsoft has become a cash-flow giant with a massive balance sheet and solid growth. Plus, it’s not afraid of M&A. This tech titan will be around for a while and deserves its blue-chip premium.

Trading MSFT Stock

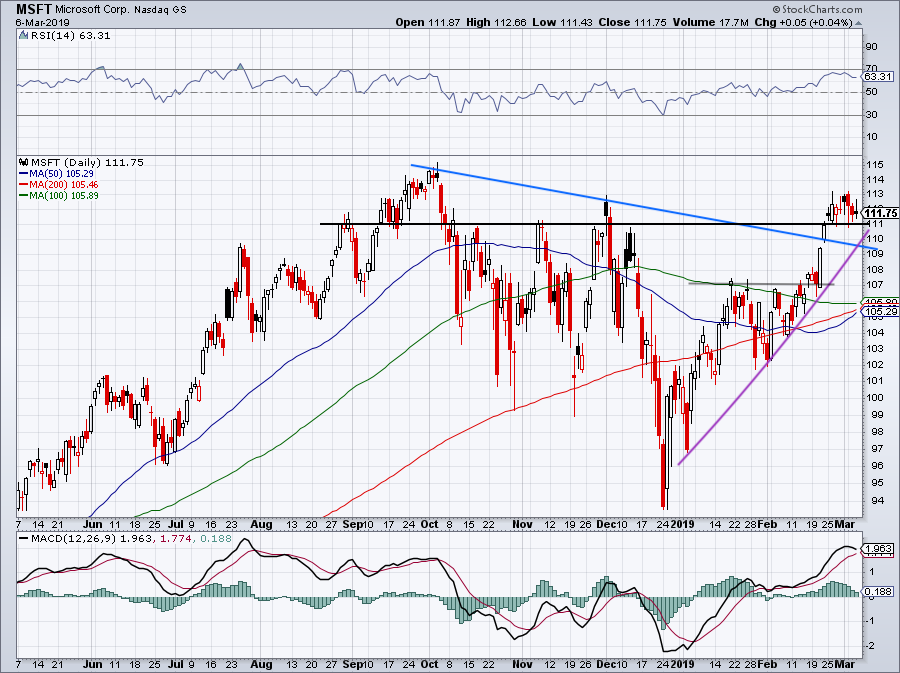

Click to Enlarge

On the charts, Microsoft stock made a beautiful mid-February break higher. After coiling under $107, shares burst higher and ran to $113. Now consolidating, investors would love to pick this name up on a discount.

We’re not likely to see $94 on MSFT stock again, but a decline into this $108 to $109 area wouldn’t be bad. If it holds as support, it validates that prior downtrend resistance (blue line) is now acting as support and can give buyers comfort that more upside could be on the way.

If the markets are entering a pullback phase, though, MSFT stock may not hold up at this level. If that’s the case, a dip to the $104 to $105 area would likely be met with a bevy of buyers. With the 50-day, 100-day and 200-day moving averages all within 40 cents of $105.50, it’s hard to imagine Microsoft stock not finding support — at least temporarily — in this region.

Either way, until the technicals change, I remain bullish on MSFT stock.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL, AMZN and GOOGL.