The stocks of Chinese e-commerce firms like JD.com (NASDAQ:JD) naturally interest many investors for an obvious reason: they’re based in China. With a population over four times the size of the U.S., the Asian juggernaut has the world’s largest consumer base. That alone makes JD.com stock intriguing.

But more recently, JD.com stock has pleasantly surprised both speculators and casual onlookers.

In 2019, JD.com stock has skyrocketed nearly 54%. In contrast, our own Amazon (NASDAQ:AMZN) is up over 25% year-to-date. While that’s not a bad haul, JD stock has gained more than twice as much as venerated AMZN this year.

Additionally, several other Chinese companies have rallied by similar amounts this year. For instance, Alibaba (NYSE:BABA) is up 38% YTD, while Momo (NASDAQ:MOM) has gained a whopping 76% so far in 2019. The U.S.-China trade war, which might end soon, initially dampened the Chinese economy. However, it appears now that we’re in the middle of a Chinese economic renaissance.

Obviously, that has positive implications for JD.com stock. But President Trump has never truly eased his aggressive stance toward China. As a result, many American firms are rethinking their dependence on Chinese customers. Yet despite these fundamental headwinds, JD and many of its peers continue to thrive.

Thus, many investors think that JD.com stock can clearly rise further. If the company didn’t crumble under the frustrating geopolitical pressures, it probably won’t do so now. Plus, it’s in the interest of both the U.S. and China to resolve the trade dispute.

And from a technical standpoint, the momentum of JD.com stock is very strong right now. Currently, JD stock is facing some resistance at the $32 level. But if JD gets past that level, it’s conceivable that the e-commerce giant could eventually hit $40. Perhaps JD.com stock will even hit record levels soon.

But despite the temptations, now is the time to be cautious about JD stock.

JD.com’s Growth Is Slowing

Invariably, whenever people discuss JD.com stock, China’s population and population growth will come up. I’ve referenced that growth before, and really, how could I not? Over the next six years, several experts predict that China’s middle class will grow to about 780 million.

However, it’s rare that a publicly-traded company will continue to rise based on a macro trend like that. And if you expect JD.com stock to be an exception, I have bad news for you: it won’t be.

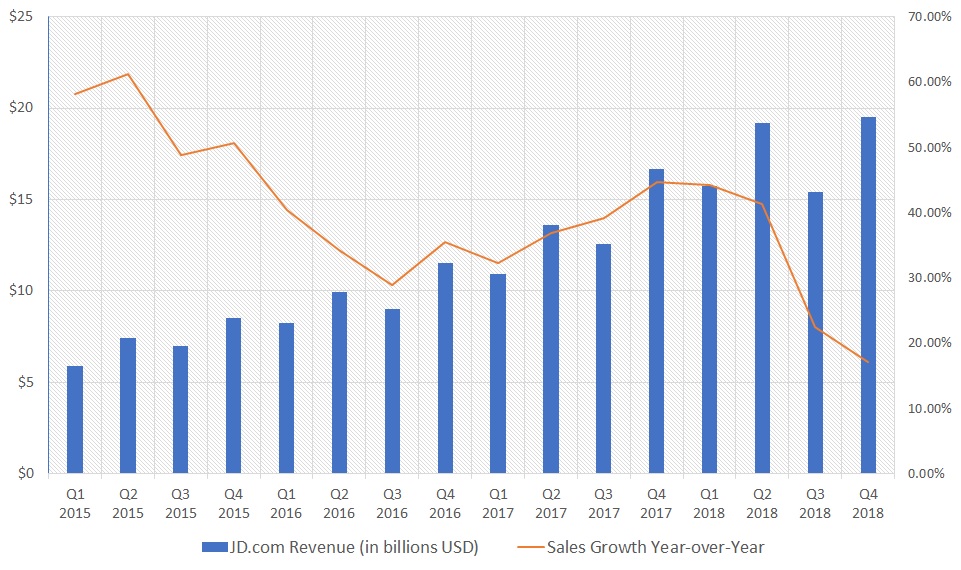

Click to Enlarge

But just one year later, its quarterly YoY growth averaged only 35%. In 2017, that metric improved, but only slightly, to 38%. Last year, the growth metric again slipped, reaching 31%.

In Q4 of 2018, the company generated $19.5 billion of sales. However, JD’s top line grew just 17% YoY, the lowest top-line expansion that JD ever reported.

Of course, as a company increases in size, it becomes harder for it to achieve dramatic growth. But in this case, it’s likely that the pain of China’s consumers is responsible for the slowing of JD’s growth. Throughout 2018, China’s retail sales noticeably deteriorated. Consequently, anyone buying JD.com stock at its current levels is taking a risk.

Additionally, I’m not sure if the outlook of Chinese consumers will improve unless the U.S. and China ink a trade deal. While the Chinese middle class gets the glory, America’s middle class is the unsung hero. After all, someone has to buy the stuff that the world’s second-biggest economy exports.

In other words, without us, there is no Chinese middle class.

JD Has Challenges in Another Market

A counterargument to my point is that, since JD’s management team realizes that it can’t beat Alibaba on their home turf, JD is looking elsewhere for opportunities.

As InvestorPlace feature writer James Brumley noted, JD has made significant inroads into Indonesia. On the surface, that’s a very smart and potentially lucrative strategy. Because Indonesia is a genuine emerging market, it offers JD first-mover advantage and tremendous growth opportunities. Brumley wrote:

Of the country’s 264 million residents, only 195 million of them currently use smartphones, and only 30 million of them are online shoppers. The figures leave room for rapid growth, not unlike the evolution China’s consumers made just a few years prior.

But for now, Indonesia’s growth is largely more a matter of potential than reality. For one thing, the country’s wealth gap is atrocious. An Oxfam report declared that Indonesia’s “four richest men now have more wealth than 100 million of the country’s poorest people.”

That might work for JD stock if the underlying company specialized in exclusive, luxury goods. But it’s striving to build a platform for the masses. And recently, the masses aren’t buying with the same fervor as before. Thus, I’d approach JD.com stock with some caution right now.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.