Is Micron (NASDAQ:MU) stock finally a must-own name? This name has become a battleground, with bulls insisting that MU stock is too cheap to ignore. Bears counter with the fact that DRAM demand has slowed and that Micron will head lower as a result.

The bears have been right so far, as Micron has fallen precipitously from its highs last summer. However, we’re starting to see a turn take place and that bodes well for the memory maker.

Is now the time to get in? Let’s examine.

Micron Is a Second Half Story

At the Goldman Sachs Technology conference on Feb. 12 CEO Sanjay Mehrotra said that Micron should see a stronger second half in 2019. He noted that DRAM demand remains healthy and that the company is working through its higher inventory levels.

We knew these inventory levels would be bloated, as management for companies like Cisco Systems (NASDAQ:CSCO) said they intentionally pulled forward future orders as tight DRAM markets continued to push pricing higher. It was a smart move by Cisco, while Micron and others manufacturers are now paying the price.

Anyway, last month Mehrotra again reiterated that outlook when Micron reported its fiscal second-quarter results. While the company beat on lowered earnings and revenue expectations, Q3 guidance came up short for both metrics. In short, Micron is still struggling to work through its inventory, but that doesn’t mean a H2 2019 recovery is off the table.

Now we’re seeing it in other places, as semiconductor stocks are getting a boost with expectations for a stronger second half too. Taiwan Semiconductor Manufacturing Company (NASDAQ:

TSM) is seeing strong order growth for its 7nm chip, while sources are saying Advanced Micro Devices (NASDAQ:AMD) will see a “significant” boost in second-half sales.

This bodes well for Micron too.

Valuing Micron Stock

One of the main catalysts for Micron stock has always been the valuation. How does a stock with such profitability trade with such a low valuation? Well, Micron hasn’t always been this profitable, but it has always been prone to booms and busts.

When we’re in the boom phase, life is great for the bulls, as Micron is printing money and its bottom line continues to swell. During the bust phase though, revenue is under pressure, inventories are bloated and margins take a beating.

Because of the volatility in the business cycle, MU stock garners a lower valuation than the rest of the market and many of its peers in tech. Case in point, analysts expect the company to earn more than $7 per share this year. With the stock price near $44, that values Micron stock at just over 6 times earnings. What a paltry multiple!

However, consider that revenue is forecast to fall almost 20% year-over-year in 2019 and another 1.5% next year and it starts to make sense. Further, earnings are expected to fall 40% this year and another 18% in 2019. Who’s going to pay a premium for that?

That’s always been the issue with Micron stock. Even though the company churns out strong free cash flow and is healthily profitable, it’s prone to these wild swings. Investors with a strong gut and a long-term outlook can justify a long position in this name when the right price presents itself.

Trading MU Stock

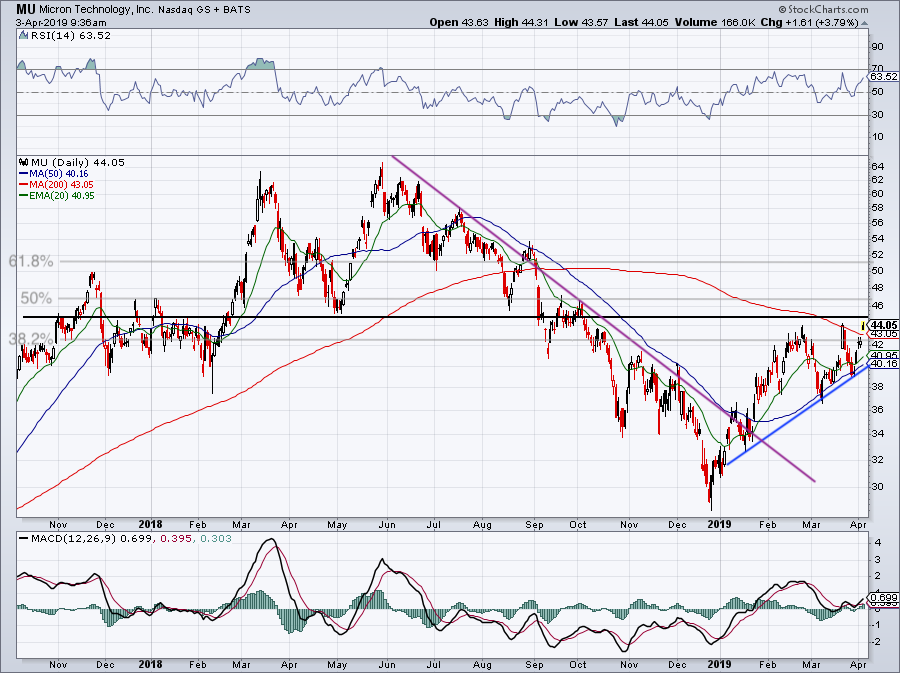

Click to Enlarge

Micron stock is moving nicely, now over the 200-day moving average and knocking on that $44 to $45 resistance zone once again. The stock has met this level twice in as many months and has put in a higher low each time after its test. That bodes well for bulls, as the more times a level is tested, the more likely it is to give way.

It helps that MU is trending higher and with the latest move, is trading above all three major moving averages. That said, should MU stock pullback, it still looks healthy so long as it holds uptrend support (blue line) and the 50-day moving average.

If investors really start to gobble up Micron on the belief that the second half will mark a turnaround in its business, we need to see it close above $45. If it can, that opens up the door to a few upside targets.

The first isn’t very high, at just $46.61 where the 50% Fibonacci retracement stands. However, a rally up to $50 would be attractive, with some follow-through potential to ~$51 to possibly $52, the former of which is the 61.8% retracement.

On the downside, MU stock will need to reset should uptrend support and the 50-day not buoy the stock price.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.