If you were looking for confident guidance for the markets, JPMorgan Chase (NYSE:JPM) just threw a monkey wrench. Generally speaking, folks on the street have a cautious approach to investing right now, and for good reasons. The U.S.-China trade war didn’t enjoy the promised quick resolution. Moreover, this is the longest bull market in history. Yet here we are with JPM stock up over 21% year-to-date.

Can we trust this big bank to continue delivering the goods? If you’ve been around the markets for a while, your instincts will almost surely tell you no. As any expert will tell you, a healthy, stable rally will always have a few corrections. This is merely to work out the kinks in the system, to keep the juices flowing. So, where’s the correction in JPMorgan stock?

Even more confusing, JPM gives the appearance of firing on all cylinders. As our own William White reported, the financial giant had a strong showing for its first quarter of 2019. Indeed, I’d say that JPM stock obliterated expectations. Against a consensus earnings-per-share target of $2.35, the banking firm delivered $2.65.

Let’s put that into perspective. In the year-ago quarter, JPMorgan managed an EPS of $2.37. This time around, covering analysts expected two pennies lower. Instead, they received a positive surprise of nearly 13%.

Not only that, JPMorgan stock received a boost from the revenue haul of $29.12 billion. In Q1 2018, the company rang up $27.91 billion. Plus, expectations heading into the most recent quarter was $28.44 billion.

JPMorgan CEO Jaime Dimon cited a strong U.S. economy and robust labor market, among other metrics countering current geopolitical uncertainty. Yet despite this outward appearance, you should trust your instincts regarding JPM stock. The devil is really in the details.

JPM Stock Is Moving Higher for the Wrong Reasons

Earlier this month, I pegged JPMorgan stock as a risky name to watch during earnings season. In hindsight, my many critics — thanks for the viewership and engagement, by the way! — may mock my cautiousness. Sure, I look like an idiot now, but here’s the kicker: I’m still leery on the big bank.

The main reason is that the much-discussed revenue growth represents the wrong type of growth. Because of that, JPM stock is moving higher for the wrong reasons. Allow me to explain:

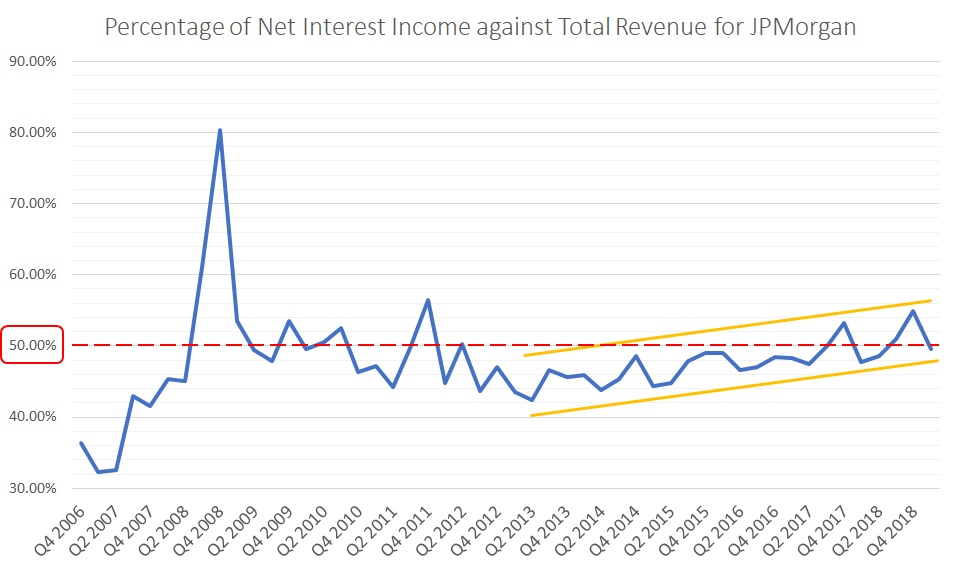

When management reported its $29.12 billion revenue, almost half of that was net interest income. This metric is exactly what it sounds like: revenues generated from a bank’s funds on its balance sheet. In other words, these are sales that JPMorgan makes from merely existing.

And if net interest income is nearly half of total revenue, that means non-interest income is barely over half. This segment represents sales from activities such as lending, advising and consulting. Stated different, these are sales from actually doing something.

In a truly healthy economy, you need non-interest income to be significantly higher than net interest income. This would indicate true economic growth: businesses are borrowing money from banks, which then circulate throughout the country in the form of wages and commerce.

Click to Enlarge

But that’s not what is happening. Instead, the allocation of net interest income has steadily increased over the years. Between Q1 2013 through Q4 2015, net interest income relative to total revenue averaged 45.7%. From Q1 2016 to now, this allocation averages 49.4%. If the trend keeps going, net interest income will represent the majority of total revenue for JPM stock.

Why is this granular detail so critical? Because during the Great Recession, net interest income ballooned to 80%! It’s just common-sense reasoning, folks.

Keep a Cautious Eye on JPMorgan Stock

But to further drive home my point, let’s consider the revenue allocation prior to the 2008 meltdown. In 2007, net interest income was only 37.3% of total sales. Recall that the troubles really started to unravel in the second half of that year.

Again, it’s just common sense. If an economy is truly robust, a banking bellwether’s sales should come from business activities. Right now, it’s coming from financial engineering, and that’s not stable ground for JPMorgan stock.

So why are shares flying? JPM stock is like no other investment. While other heavyweights like McDonald’s (NYSE:MCD) or Boeing (NYSE:BA) clearly represent specific industries, JPM represents us all. If it’s suffering, it usually means that a large, negative catalyst exists.

I’m not trying to be conspiratorial. Still, it’s a bad look for everyone if JPM stock starts crumbling. Therefore, an incentive exists to keep shares on the up and up.

But as much as I’d like to join the party, I can’t. We have a student debt crisis, along with an opioid epidemic and startling levels of homelessness. Yet in this harsh backdrop, JPMorgan shares are soaring? As it turns out, your instincts are correct, even if it’s not reflected in the charts.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.