Editor’s note: This article is a part of InvestorPlace.com’s Best Stocks for 2019 contest. John Jagerson and Wade Hansen’s pick for the contest is Adobe (NASDAQ:ADBE).

Since December 2018, we have been recommending Adobe (NASDAQ:ADBE) as a long position because its fundamentals are undervalued. ADBE’s market position is dominant in its media products and the company has been steadily growing by adapting its Creative and document management solutions to mobile. We feel that these factors will protect the company from the emerging economic headwinds both in the U.S. and outside.

From a technical perspective, ADBE has been able to outperform its benchmark indexes and most of its peers despite a choppy year for stocks so far. Now that we have another two quarters of data since we began recommending ADBE stock, it’s time to revisit our analysis and see if we can still make the same judgement.

Valuing ADBE

We believe that ADBE’s ability to grow its profit margins has positioned it well in each of its three main segments: Digital Media, Digital Expertise and Publishing. The media segment includes their Creative products like Photoshop and their document services, which accounts for more than 70% of their revenue.

The most recent quarterly report on June 18 showed Creative revenues were up by 22% on a year-over-year basis. The emphasis on services and subscriptions has increased ADBE’s gross margin to 85% and net margins are at 23% over the same period. The company did suffer a little over the last two quarters due to adverse currency conversion rates, but to put it in perspective, from a margin standpoint, ADBE is outperforming Apple (NASDAQ:AAPL), Netflix (NASDAQ:NFLX), and Amazon (NASDAQ:

AMZN); it’s also just behind the most recent report from Microsoft (NASDAQ:MSFT).

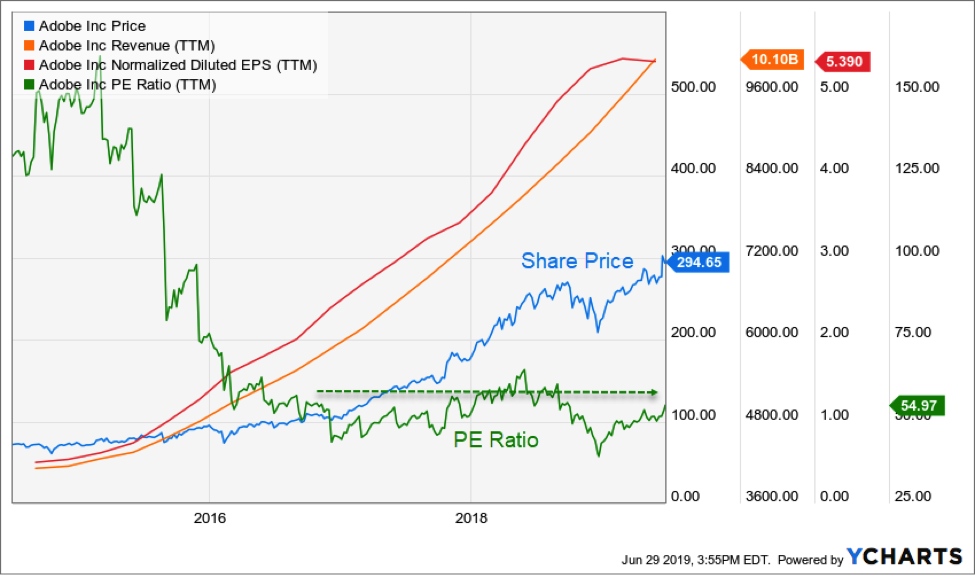

Besides the favorable comparison between ADBE and their peers, we believe the company’s growth has not been fully priced into the stock. As you can see in the following chart, revenue and EPS have been rising with the stock’s price, but its earnings multiple remains near historical lows. If we were to adjust the EPS line to use constant dollars, the trend of the P/E ratio and EPS would be even more impressive.

The point behind a value-price comparison like this is to determine if investors are paying more, or less, for each dollar of earnings than they have in the past. Because growth is still strong, paying less for the stock now indicates the likely probability that the shares are still undervalued.

Technical Position

Like the stock averages themselves, ADBE’s share price drew down in April and May as traders worried about the impact of slowing economic growth and the trade war. Total revenue from the Europe Middle East Africa (EMEA) region was 27% in the most recent quarter and 15% was from Asia. Outside the US, economic performance and stock markets haven’t recovered from the bear market of late-2018 to the extent the U.S. has, and we feel this has also dragged on ADBE’s share price.

However, ADBE’s current technical breakout following their earnings report from an inverted “head-and-shoulders” pattern looks to be a strong bullish momentum signal. This stock tends to have reliable technical patterns which we have been commenting on in our previous recommendation updates including the double bottom in February, bullish diamond in April, and the double-bottom retest at the beginning of June.

In the short term, a Fibonacci-based target of the inverted head-and-shoulders pattern would indicate an upside target in the $313 per share range. Historically, patterns like this can play out very quickly, but 60-days is closer to the long-term average.

A Few Issues to Watch for Adobe

As previously mentioned, a quarter of Adobe’s sales come from Europe. Adobe may see its revenues softening, especially in document services if the European economy continues to weaken and the Brexit outlook gets worse due to new conservative leadership in the U.K. Adobe’s continual investment in developing end-to-end document signing and processing puts it at the forefront of the global supply chain. However, recent trade wars could stall that income growth in the short term.

The company has placed an emphasis on lower-end media solutions and document management that are focused on mobile users which should help insulate the company from some economic issues because these products are broadening their customer base. We believe the long-term impact of this focus will be similar to what happened when the company shifted to cloud-based services and will increase margin growth.

As noted in ADBE’s recent earnings release, a rising dollar was a negative for earnings. The Fed is hinting at a strong possibility of interest rate cuts in the short term, which could help weaken the dollar and improve performance. However, even with the Fed’s potential cuts in July and December, the battle for a cheaper currency may be tough to win against the European Central Bank (ECB) which has promised to be ready with easing of its own if market conditions worsen in Europe. This is a systemic issue that will affect most large companies but is something to keep your eye on this summer.

InvestorPlace advisors John Jagerson and S. Wade Hansen, both Chartered Market Technician (CMT) designees, are co-founders of LearningMarkets.com, as well as the co-editors of Strategic Trader, a trading service designed to help you make consistent options income in any trading environment. Get in on the next trade today by clicking here.