Among investment categories, the semiconductor group finds itself in an awkward situation. And within this sub-segment, traders are attempting to decipher Micron Technology (NASDAQ:MU). On one hand, MU stock has performed well following the truce in U.S.-China trade war tensions. On the other hand, the company faces fundamental challenges that could hurt its equity value.

Of course, the biggest hurdle impacting Micron stock is the computer chip market; specifically, pricing for flash-memory NAND chips and so-called “volatile” DRAM chips. Currently, the semiconductor market is experiencing a lull. For instance, DRAM chips – which largely service PCs and data servers – plummeted nearly 30% in the first quarter of 2019.

Obviously, that does no good for the MU stock price. After all, Micron specializes in producing both NAND and DRAM chips.

Even worse, many experienced analysts in the semiconductor space believe that the DRAM market is still vulnerable to further corrections. That puts investments like Micron stock, as well as broader competitors like Intel (NASDAQ:INTC) and Nvidia (NASDAQ:NVDA) on notice.

Here’s the problem: NAND is a type of memory that is particularly useful for smartphones and mobile devices. But a time when even Apple’s (NASDAQ:AAPL) once-dominant iPhone is experiencing

lagging sales, NAND presents less of an opportunity. Thus, semiconductor firms’ hopes rested on DRAM, and for good reason.

Based on DRAM’s unique architecture — a densely structured chip that allows for billions of memory cells crammed into a small space — it’s best suited for data servers. Due to the burgeoning data center evolution, Micron can feed this growing demand. That benefits MU stock, provided that demand sustains itself.

Evidence suggests that it’s not, drawing questions for Micron stock.

Complicated Narrative Surrounds MU Stock

Before we dive in, you should know this: semiconductor firms ebb and flow with the underlying chip market. And whether for better or for worse, the chip market is incredibly volatile. Moreover, research firm Gartner (NYSE:IT) predicted two years ago that 2019 would be a downturn for DRAM.

So far, that prediction has proven prescient. Naturally, it presents a worrying case for MU stock.

Now, some investors have a tendency to ignore such high-level analysis as not being in touch with the ground floor. However, if you’re thinking about buying Micron stock, you should at least understand the risk: historically, MU’s pricing is intricately linked to the memory-chip market.

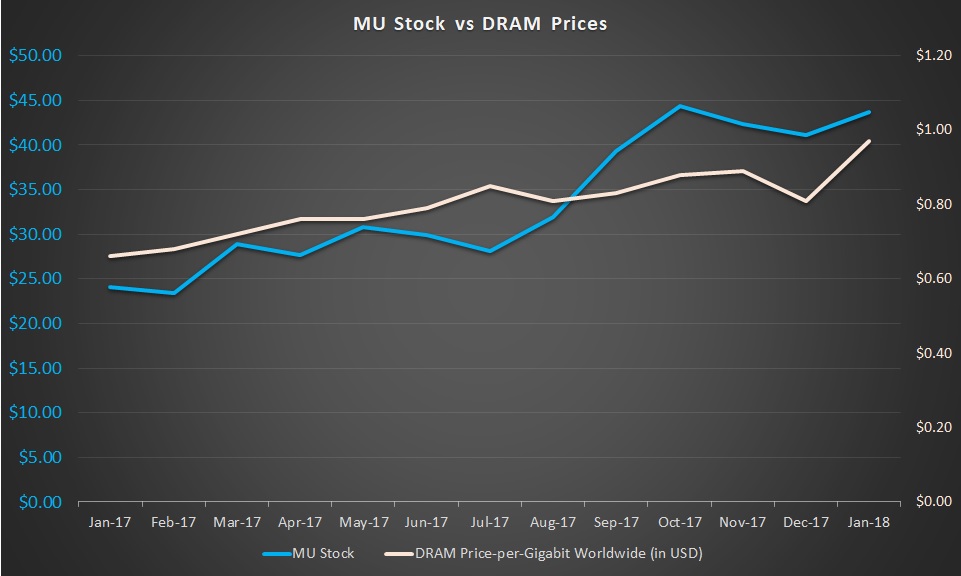

Click to Enlarge

For instance, from January 2017 through the end of January 2018, DRAM’s price-per-gigabit increased from 66 cents to 97 cents. Along the way, the pricing experienced some twists and turns.

Over the same period, the MU stock price increased from $24.11 to $43.72. Like the underlying DRAM market, Micron did not have a straight shot skyward. Shares moved almost in lock-step with DRAM prices, with a correlation coefficient of 84%.

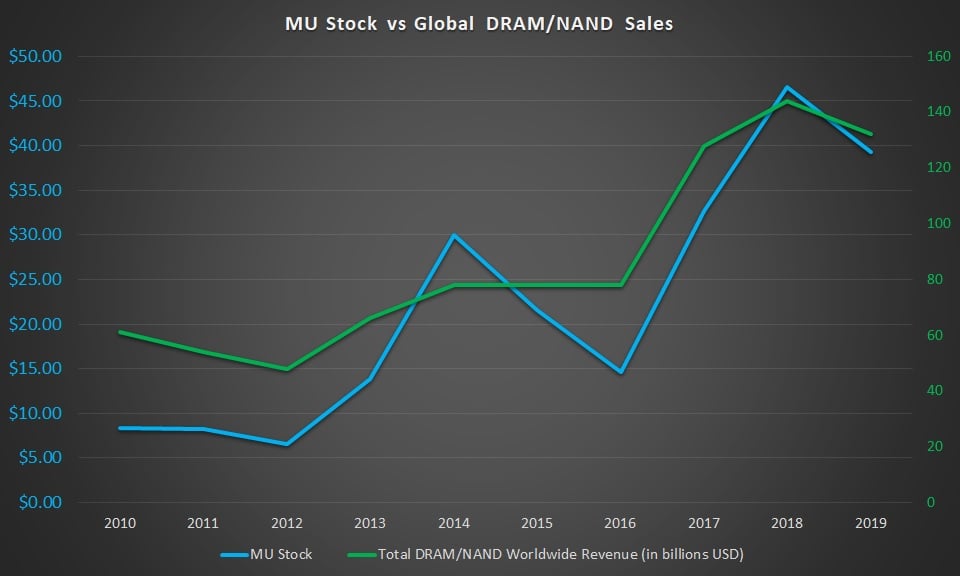

I note a similar trend comparing Micron stock with total DRAM and NAND global revenues. As chip sales increase, so too does MU shares. Unsurprisingly, when chip sales stall, shareholders are taken on an unpleasant ride.

Click to Enlarge

Admittedly, I’m charting the obvious. However, this data also confirms that MU stock rarely moves against the grain. So if DRAM is about to tumble deeper, it might be time to hit the exits.

But that’s only true if the forecasts of doom are valid. From the numbers I’m seeing, data centers have strong tailwinds. For instance, demand for cooling equipment necessary to keep data-server chipboards at optimal temperatures is increasing. That doesn’t make sense unless data centers are likewise rising.

Long-Term Picture Remains Bullish for Micron Stock

Logically, if the tides shift positively for DRAM, MU stock stands to profit handsomely. Especially at these undervalued prices, contrarians may want to consider picking up some shares.

That said, it’s always difficult predicting nearer-term swings. Sentiment could turn negative on absolutely silly reasons. And that could end up making me look silly as well.

But where I’m more confident is the longer-term picture. In this context, I think President Donald Trump’s trade war with China is the perfect tailwind, and not a dark cloud. I say this because for years, perhaps decades, American tech firms have not operated on level ground with the Chinese.

Generally, Americans played by the rules. The Chinese have not. This strange, uncontested dynamic allowed the Asian juggernaut to harmfully troll the tech space.

But the Trump administration is putting a hard-stop on China’s shady business practices. And while the trade war hurts now, it’s incredibly beneficial for our semiconductor industry’s long-term, sustained growth. Bring in the DRAM factor and you have a case here for a deeply profitable discount in Micron stock.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.