As one of the most powerful names in business, Apple (NASDAQ:AAPL) always generates headlines. This time, however, a lot of the news is casting a negative light on AAPL stock. With shares up 28% year-to-date, but having gone nowhere since late April, it’s a good time to reassess the situation.

Things took a turn for the worse when Rosenblatt Securities analyst Jun Zhang downgraded shares of the consumer tech giant to a “sell.” Citing a pressured environment for the company’s flagship iPhone, Zhang forecasts headwinds against total revenue growth. As a result of the bearish note, the Apple stock price closed down 2% to start the week.

Specifically, Zhang called out the iPhone XS, fearing that it could be “one of the worst-selling iPhone models in the history of Apple.” Moreover, Apple’s other hardware products, such as the iPad and HomePod, may not provide meaningful revenue support. Obviously, this was a rough Monday for AAPL stock.

And Zhang isn’t incorrect to bring up these concerns. For instance, Apple’s iPad, while a cute toy to play around with, hasn’t truly resonated with consumers. Sales for the iconic tablet peaked in 2014. Additionally, Samsung was neck-and-neck with Apple in terms of global smartphone market share earlier this decade. However, the latter took the lead and never looked back.

Dependency on the iPhone was a strong suit for Apple stock. Now, it’s a liability.

At the same time, Chinese consumers still love their iPhones. And Wedbush analyst Dan Ives argues that 60 to 70 million customers could need an upgrade soon.

Is it premature to go bearish on AAPL stock?

The Growth Narrative for AAPL Stock Appears Stretched

Before we dive into the above question, let’s take care of some housekeeping. First, don’t misunderstand the broader point: AAPL stock isn’t a convincing bearish trade. It’s very close to a $1 trillion market capitalization. Plus, the company is overflowing with cash.

In other words, management has many levers to lift the Apple stock price should the need arise.

But it’s also fair to point out that AAPL stock doesn’t have a convincing bullish argument at the moment, either. I agree with Ives that the Apple brand resonates with Chinese buyers

. It was an underlying narrative a few years ago, and it remains intact today.

However, I’m more interested in the stories that the numbers weave. Here, the hard data confirms Zhang’s “sell” recommendation. No matter how you look at it, iPhone sales have matured. Any further progress will require a costly investment. Unfortunately, even with China in the picture, the Asian juggernaut can’t support Apple stock, let alone skyrocket it.

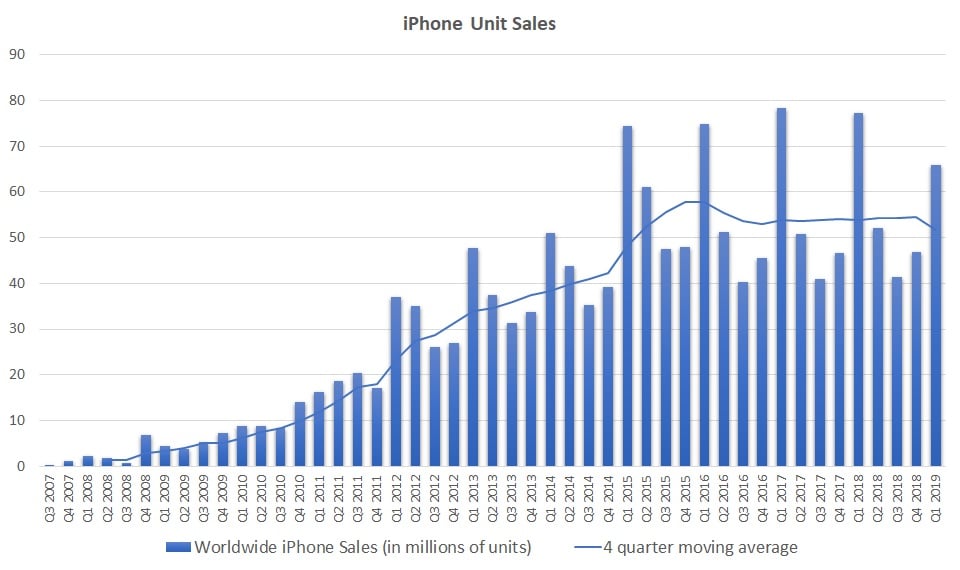

A helpful illustration is the business growth curve, or S-curve. In a nutshell, massive growth occurs in the infancy and expansion stages. Later, in the maturation phase, growth slows due to a lack of new customers.

Click to Enlarge

It’s exactly what we’re seeing now with iPhone unit sales. From the third-quarter 2008 through Q3 2009, year-over-year (YOY) iPhone sales growth averaged 303%. From Q4 2009 through Q2 2012, that growth rate remained a very respectable 88%.

But from Q3 2012 onward? Shockingly, growth slipped to just under 12%. We’re also at a point where we’re seeing negative growth in some quarters on a YOY basis. That tells me that the party is over for the iPhone; hence, Zhang’s downgraded expectations for the Apple stock price.

Historical Leverage to the iPhone Haunts Apple Stock

Many bulls might counter that the iPhone tells only chapter of the story. Obviously, Apple has many other products and services. Thus, it’s not all doom and gloom for AAPL stock.

I’ll reiterate that doom and gloom isn’t my agenda at all. Rather, I’m just approaching Apple from a rational perspective. In the analyst sphere, we have two competing perspectives. I believe that one side has the better argument and evidence.

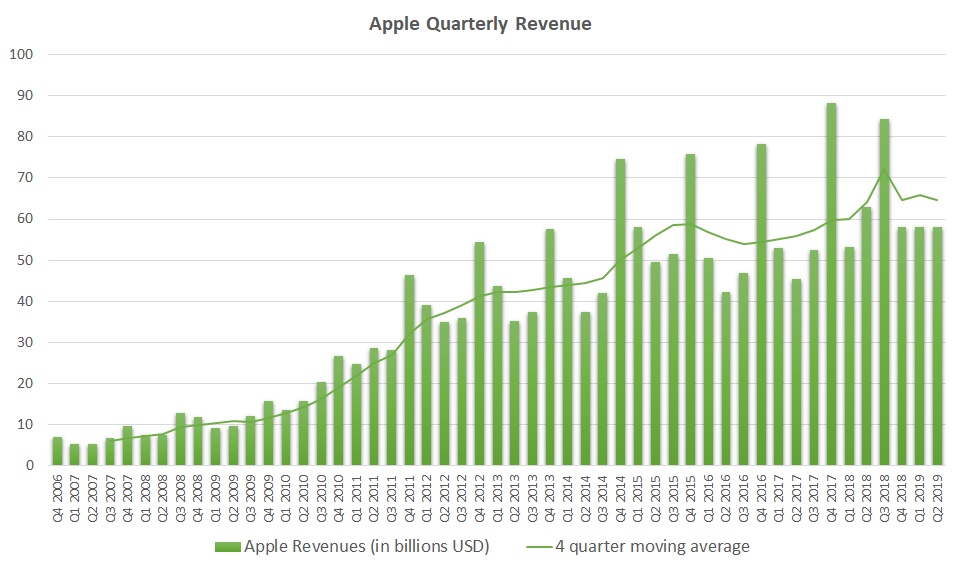

The other reason to not dive too deeply into AAPL stock is the revenue allocation. In recent years, the iPhone represented roughly two-thirds of total Apple revenue. That has dipped significantly but nevertheless, the flagship smartphone still accounts for the majority of sales.

Click to Enlarge

Under this context, it’s no surprise that Apple revenues have also hit the S-curve’s maturity phase. Earlier this decade, quarterly sales witnessed YOY growth that hit strong double digits. Now, the growth rate risks falling toward single digits.

While Apple was busy producing the next iteration of the iPhone, they should have conceived a viable alternative product. That they failed in this endeavor is the real reason why the bears hold their negative perspective. The Apple stock of old is nothing like it is today.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.