For me, very few companies are as compelling as they are frustrating like Rite Aid (NYSE:RAD). As a speculating day trader, you love the volatility inherent in the RAD stock price. On any given day, you can churn out a massive profit by playing both sides of the fence. However, it’s also incredibly difficult to chart out a reasonable pathway for Rite Aid stock.

Fundamentally, the pharmacy giant operates under a contradictory environment. On one hand, the company’s main industry should support the RAD stock price. After all, everybody gets sick or injured at one point. Further, when folks encounter such troubles, they usually prefer access to a 24-hour pharmacy for immediate treatment or medication. That helps on the competitive front, where rivals like Walmart (NYSE:WMT) and Target (NYSE:TGT) usually have limited store hours.

On the other hand, the hard numbers betray the positive implications for Rite Aid stock. Despite secular demand, the pharmacy has posted flat to declining revenues over the past few years. Earnings typically print red ink, resulting in negative free cash flow.

I personally know how frustrating it is to make intelligent forecasts on the RAD stock price. Back in August of this year, I supported the speculative case for shares because of Amazon’s (NASDAQ:AMZN) Counter program: essentially, the partnership would bring high-dollar clientele into Rite Aid stores.

Shortly after publication, Rite Aid stock tanked.

In September, I noted that RAD stock had accelerated dramatically. Therefore, it was time to sell

. And what do you know? I ended up calling the top, a price that wouldn’t be breached until this month.

With shares having jumped dramatically in recent sessions, what’s the game plan now?

The Difficult Long-Term Thesis for RAD Stock

Some of the enthusiasm for Rite Aid stock centers on the underlying company’s surprisingly robust earnings report for the quarter ending Aug. 31. RAD beat convincingly on per-share profitability but dipped slightly against revenue expectations.

Another factor lifting the RAD stock price is the change at the top. New CEO Heyward Donigan brings with her expertise on modernizing healthcare-related businesses. Certainly, Rite Aid could use a lot of that.

However, the biggest area where the pharmacy must improve is revenue efficiency. In order to achieve this lofty goal, management must redistribute their physical footprint in the most effective manner possible. As it stands, Rite Aid is leaving a lot of money on the table, invariably hurting RAD stock.

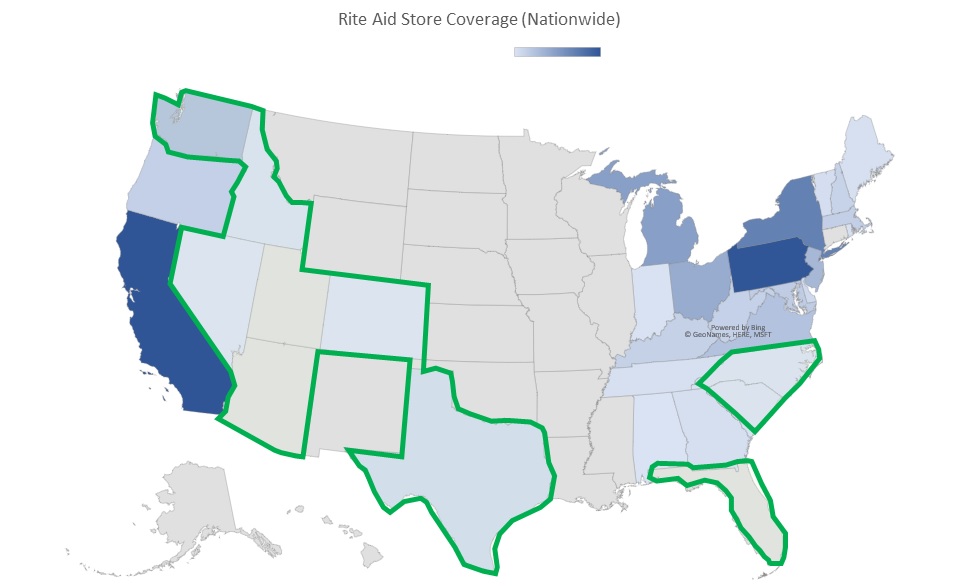

According to the company’s website, Rite Aid has 3,022 stores across 30 states. Based on the latest U.S. Census estimates, these 30 states combine for 235.1 million residents. Thus, the maximum efficiency rate for Rite Aid is one store for every 77,798 people.

Click to Enlarge

However, 14 states have a lower-than-average efficiency ratio, averaging one store per 1.18 million people. Even worse, many of the states that have low efficiencies are some of the fastest-growing states in the U.S.

And parallel to those woes, Rite Aid has “excessive” efficiency in low-demand states. For instance, the pharmacy has a disproportionately high 68 stores in West Virginia. Against a 1.8 million population size, that’s one store for every 26,556 people. That’s just ridiculous when California has one store per 73,118 people.

Additionally, California is the fifth-largest economy in the world. Rite Aid needs to divert its resources to the areas that truly matter. That also includes getting out of Pennsylvania, where the company has one store per 23,761 residents.

A Good Trade but Difficult Investment

Of course, divesting resources isn’t easy. But if done smartly, Rite Aid has the opportunity to make their overall business more efficient.

In the above picture of Rite Aid’s store coverage in the U.S., I outlined in green the top ten states that have the highest population growth. Basically, these high growers are located to the east and south of RAD’s strongholds.

Not surprisingly, many of these states are also popular with millennials. Thus, the pathway for a sustainable rise in Rite Aid stock is clear: the company must prioritize a higher presence where people, especially millennials will go.

Because whatever longer-term positives RAD hopes to gain from its Amazon partnership won’t happen unless they’re in relevant areas with growing millenial populations. I’m sorry but Pennsylvania – other than being the birth state of Taylor Swift – isn’t as relevant an area compared to more popular states.

However, with Rite Aid’s difficult financial situation, this strategy will be nothing short of grueling. Thus, I view Rite Aid stock as a viable trade because of its volatility. But as an investment? Unless you’re playing with “dumb money,” I’d pocket my profits now.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.