For incredibly satisfied shareholders, Apple (NASDAQ:AAPL) is the gift that keeps on giving. In the past month, Apple stock delivered right around 14%. In the trailing three-month period, shares have jumped nearly 33%. And last year, the equity almost doubled in market value. That being said, though, it begs the question: how long can this rally last?

Ordinarily, I assume that most stakeholders would take the money and run. Based on the cyclical nature of the stock market, you’d expect an overheated asset to correct. And technically, that’s what Apple stock is. If you look at traditional metrics such as the relative strength indicator, they’re telling unequivocally to pocket your profits.

However, Apple stock is anything but ordinary. No matter how overbought the technical charts look, the fundamentals seemingly give a very different picture. Obviously, the biggest overriding tailwind is the substantive progress in U.S.-China relations. Recently, the world’s two biggest economies signed a “phase one” trade deal. This helps set the stage to finally end the tit-for-tat tariffs, and cool longstanding suspicions.

Admittedly, the freshly inked deal doesn’t resolve everything. As The Wall Street Journal’s Josh Zumbrun and Anthony DeBarros noted, “most Chinese imports are still subject to U.S. tariffs.” But as of now, this is the most significant sign toward a finalized deal.

Just as importantly, Apple’s iconic iPhone has experienced a resurgence in sales, particularly in China. Based on analysis from Credit Suisse, December 2019 iPhone shipments to China jumped nearly 19% from the year-ago period. Better yet, the shipment surge contrasts sharply and favorably with disappointing October and November results.

Thus, despite the technical warning signs against Apple stock, the fundamentals suggest buying the momentum. So, should you listen?

Longer-Term Outlook for Apple Stock Is Suspect

Personally, I don’t like to buy into such extreme momentum. However, from a nearer-term perspective, the idea of gambling on Apple stock is quite compelling.

Previously, I’ve criticized Apple for not coming up with game-changing ideas. However, their current-generation iPhone is firing on all cylinders– and one of the most visible innovations is the new iPhone’s advanced camera lenses.

My “alma mater” Sony

(NYSE:SNE) provides the sensors for the iPhone and other smartphone brands. Even with running factory capacity at full blast 24/7, they haven’t been able to keep pace with demand. And honestly, that’s brilliant news for both stocks.

Furthermore, Apple’s upcoming first quarter of 2020 earnings report should deliver wickedly strong comparative results. Therefore, I don’t want to jump in front of this moving train.

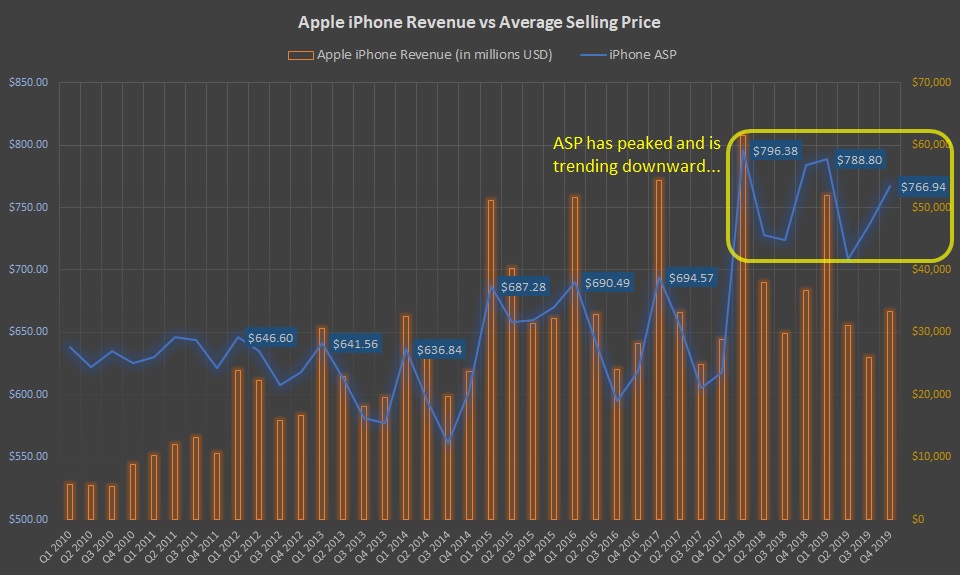

But, if you decide to buy Apple stock, I’d have an exit strategy already in place. While the iPhone momentum represents a source of tremendous confidence, I’m not sure if it will hold longer term. I say this because the smartphone’s average selling price (ASP) has consistently failed to break the $800 level.

Click to Enlarge

In the first half of last decade, the iPhone’s ASP averaged $619. In the latter half, this metric increased noticeably to $691.45. A good part of the change stemmed from Apple’s experimentation with premium-level smartphones as a distinguishing attribute.

On the surface, it’s not a bad idea. The smartphone market is saturated with look-a-like competitors. By going premium, Apple can rise above the industry’s commoditization.

Unfortunately, the iPhone’s ASP peaked in Q1 2018 at $796.38, and has subsequently drifted lower despite reaching right around $785 to close out 2018 and begin 2019. What that tells me is that the premium brand strategy has reached its limits. If they want to sustain revenue, Apple must lower their prices — and lowering prices ultimately leads to commoditization.

A True Trade Deal Not Yet Finalized

One of the counterarguments about the declining ASP is that they don’t fully reflect the new path forward from the recently signed trade deal. Once the U.S. and China settle their differences, we could see continued outstanding iPhone sales results.

While possible, I’d also bring up the point that the phase one deal has yet to scratch the surface. According to Benn Steil, director of international economics at the Council on Foreign Relations, declared that, “China is set to do little more than restore agricultural purchases and offer some nice words on financial services and intellectual property.”

That’s not a resounding show of confidence.

Further, the almost two-year long trade war stunted what was once surging Chinese consumer sentiment. If we have any hiccups in the future with U.S.-China relations, consumer sentiment can again falter. And that doesn’t bode well for Apple or Apple stock, especially as it’s trying to sell increasingly expensive devices.

As of this writing, Josh Enomoto is long SNE.