Commonly referred to as the Netflix (NASDAQ:NFLX) of China, video streaming platform iQiyi (NASDAQ:IQ) enjoyed a profitable but turbulent 2019. Getting off to a meteoric start within the first two months of last year, IQ stock plummeted into early October. But as the U.S.-China trade war pressure eased, sentiment for shares resumed. Now, prospective buyers all have the same question: can this momentum carry throughout 2020?

I don’t think it’s a stretch to assume that most folks view IQ stock in a positive light. As a Chinese company, iQiyi suffered significant pressure from the trade war. While the specifics of the trade dispute didn’t directly impact the streaming company, it conspicuously hurt China’s consumer sentiment.

From early 2016 through late 2017, the Asian juggernaut’s consumer confidence index skyrocketed. However, the index’s progress came to a grinding halt in 2018 as the U.S. and China ramped up their sharp rhetoric. As words transitioned to tariffs, consumer confidence largely flatlined.

And because iQiyi depends on people’s discretionary spending – streaming is entertaining but it’s not a necessity – the prospects for IQ stock turned rather cloudy.

Fortunately, then, shares now have a geopolitical tailwind. With the world’s two biggest economies signing a “phase one” trade deal, China’s consumer confidence index will likely move higher. Although the deal doesn’t resolve every issue, it at least mitigates the net impact of the issued tariffs.

In turn, this should translate to a recovery in China’s labor market, which suffered during the trade war. Simply, more people having jobs equates to a larger discretionary income pool. Based on iQiyi’s popularity, investors may see greater demand for IQ stock.

Still, caution is warranted and here’s why.

Fiscal Concerns Remain for IQ Stock

One of the oft-cited bullish arguments for iQiyi is that the company resonates with its core audience. You’re not going to get a dissenting comment from me. The streaming firm consistently grows its active user base across multiple mediums

. Furthermore, nearly all its total subscribing members are paying members.

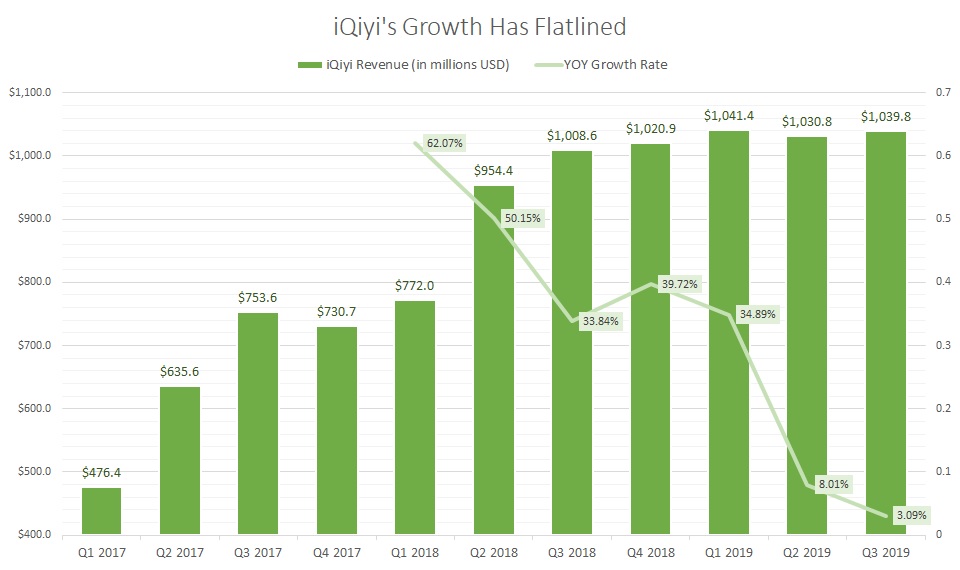

However, where the counterargument lies is in the financials. Given iQiyi’s immense popularity and influence, this dynamic should convert to meaningful fiscal momentum. Certainly, revenue growth in past years have excited buyers of IQ stock. But now, this narrative just doesn’t exist anymore.

In the first quarter of 2018, iQiyi reported $772 million in top-line sales. One year later, management reported slightly over $1 billion in revenue, up nearly 35% year-over-year. Over the five quarters in that time frame, the average sales growth rate equaled over 44%.

That’s the good news. But in the last two quarters (Q2 and Q3 2019), that growth rate has dipped to an average of 5.6%.

Click to Enlarge

Granted, that by itself is not a reason to hit the panic button. However, net income losses continue to widen. As the company grew, so too did its costs and expenses. And because the losses are relatively steep, it’s hard to imagine a road map to profitability without a paradigm-shifting event.

Interestingly, in iQiyi’s Q3 2019 disclosure, management noted that its advertising revenue dropped a sizable 14% YOY. Citing a “challenging macroeconomic environment in China” as one of the contributing factors, management let slip a key vulnerability for IQ stock: shares need a strong Chinese economy to justify their elevated market value.

I wouldn’t be concerned if the phase one trade deal was a comprehensive one. But with several geopolitical experts blasting the deal, iQiyi isn’t out of the woods yet.

Ambiguous Environment Makes iQiyi Risky

According to The Wall Street Journal, “…most Chinese imports are still subject to U.S. tariffs, and many trade issues remain the subject of sharp disagreement.” Let’s be honest: the present U.S. administration isn’t what you would call diplomatic. And Chinese leaders hate losing face.

In other words, the signed trade deal is more gesture than substance. Unfortunately, that leaves IQ stock hanging in a very ambiguous environment.

Sure, prospective buyers can take heart in its recent rally. At the same time, though, IQ has been incredibly choppy following its initial public offering. Realistically, speculators should expect more of the same until we get a true trade deal on the table.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.