Halliburton (NYSE:HAL) stock has a high dividend yield — it’s around 9.5% as I write this. That is usually a sign that the company can’t afford the dividend. Investors assume that the dividend is in danger of being cut.

Maybe that will happen in this case. It certainly looks like Halliburton might not be able to afford the dividend. But on the other hand, Halliburton has a very strong business in the oil and gas sector.

I think it is possible that Haliburton’s cash flow will come back after the economy rebounds from the coronavirus downturn. That is because the pickup in growth after economies get back to work is bound to push up oil prices.

And if that happens, then Haliburton could withstand the downturn with its ability to pay its present dividend intact. Let’s look at this closer.

Halliburton’s Revenue Will Be Weaker But Could Rebound

Over half of Halliburton’s 2019 revenue came from building and completing wells on behalf of oil companies. You can see this in the chart the company produced in its annual report (page 2).

The pie charts show the breakdown of Halliburton’s revenue. It has two main segments. The largest, completion and production of wells, is lower as a percentage of the total in 2019. But it still represents 63% of Haliburton’s revenue.

The point is that, once economic activity picks up, the number of wells that the company services will likely pick up as well. That does not downplay the fact that Haliburton will experience a deep downturn.

For example, last year the company had lower revenue, especially in the U.S. Its U.S. and North American revenue portions fell 17.7% to $11.9 billion. Moreover, the U.S and North American segment fell to 53% of revenue from 60% a year earlier.

But my point is that once the price of oil starts to pick up, the U.S. revenue segment, Halliburton’s bread and butter, will likely climb as well.

So much of the bad news for Halliburton’s revenue and cash flow is already foreseen by the market. In fact, if we look at cash flow, the dividend does not look that expensive.

Halliburton’s Free Cash Flow Can Support The Present Dividend Cost

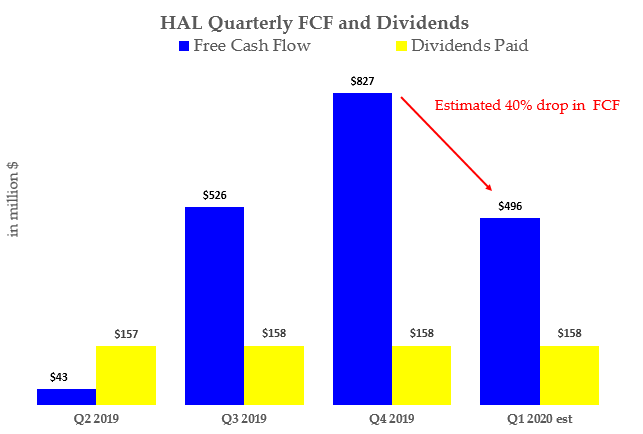

If you look at the table I prepared below, you can see that Halliburton’s free cash flow (FCF) covers the quarterly cost of the dividend. In fact, the chart I have reduces the estimated level of FCF by 40% from the prior quarter.

Click to Enlarge

Even in that situation, the present 72-cent-per-share annual dividend, which costs $158 million every quarter, is still well below the funding source.

The estimate for free cash flow for Q1 2020 is $496 million. That is over twice the cost of the dividend.

What this implies is that FCF could fall much further before the dividend would not be affordable.

And don’t forget that Halliburton’s FCF is a function of how much it spends on capital expenditures. Halliburton can easily reduce its capex spending, and probably has done so.

What Should Investors Do With Halliburton Stock?

Halliburton is coming out with its Q1 2020 earnings on April 20. So you are going to want to wait and see whether the company will cut the dividend you might wait until then. You have little to lose, since, on the one hand, if it cuts the dividend, Halliburton stock will likely fall.

But, on the other hand, if it doesn’t cut the dividend, it is not too likely that the stock will rise. Investors are pricing in very negative oil and gas forecasts. They will be surprised that the dividend wasn’t cut, but they might continue to expect it. For example, Daniel Thurecht on Seeking Alpha automatically assumes that the dividend will be cut.

So, I expect the patient investor will do well with Halliburton stock. One thing is for sure. The stock price seems to expect that the oil and gas situation as it looks today to continue for a long time. That is likely to be an overly pessimistic outlook.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here.