In my last article on Halliburton (NYSE:HAL), I said if it kept the dividend, the yield on HAL stock would be very attractive. My stance was both right and wrong, but nevertheless, this stock still represents good value.

The dividend was cut on May 20, to just 18 cents annually, down from 72 cents annually, a 75% drop. So, I was wrong about the dividend not being cut. Today the stock has a 1.5% dividend yield.

But, guess what? HAL stock is up since then. At the time of my article, the stock was at $10.29. Today, the stock trades at $11.90, up 14.1%.

I suspect a good part of the reason is that the price of oil has risen during that period. Today it is at $35.32 per barrel on a spot basis. On May 12, the price was at $26.33. So, it has risen 34.1% in less than one month.

Halliburton’s Actions Should Ensure Positive Cash Flow

In its press release about the dividend cut, the company said it had already cut expenses by $1 billion and reduced capex by 50%. The company said the dividend cut represents a “reasonable payout.” It also helps them to “deliver shareholder returns, while maintaining a strong liquidity position.”

Let’s look at that more closely. Analysts at Seeking Alpha predict the company will have negative earnings for both this and next year. But that does not mean the company will have negative free cash flow (FCF).

For example, in the 12 months ending in March, the company had a loss of $2.3 billion. But its FCF over the year was still positive at $1.4 billion. This allowed Halliburton to pay dividends costing $631 million.

Going forward, the dividend will cost just $158 million annually. I suspect that it will be easily affordable. For example, in the quarter ending in March, Halliburton made an adjusted net income of $270 million

, or 31 cents per share. This was before impairments and other charges and a loss on the early extinguishment of debt. Including those charges, net income was negative $1 billion for the quarter.

Moreover, the free cash flow last quarter was still positive at $12 million. So you see my point, the net income can be at a loss, but free cash flow can be positive. That should bode well for HAL stock over the next year if oil continues to rise.

What About Halliburton’s Dividend Yield?

I think the company will make efforts to increase its dividend fairly aggressively over time if the price of oil keeps rising.

For example, Halliburton increased the dividend per share from 36 cents in 2012 to twice that level by 2019. That represents an average annual compounded increase of 10.4% over that 7 year period to the end of 2019.

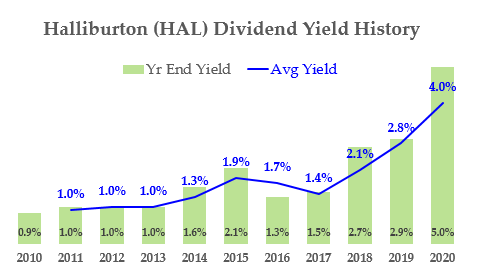

Click to Enlarge

Moreover, look at the chart I have prepared at the right showing HAL stock’s historical dividend yield, using data from Seeking Alpha. You can see that only after 2017 has the stock’s dividend yield been rising.

Prior to that time, for example, the average dividend yield for the stock for the seven years ending 2017, before the yield took off, was 1.33%. For most of that period, the dividend per share was fairly stable.

So this implies the stock fell a good bit. Nevertheless, the 1.33% dividend yield seems like a reasonable target yield for the stock.

A Target Price for HAL Stock

Therefore, one way to value HAL stock is to take today’s dividend and divide it by the average dividend yield from 2010 to 2017. So, 18 cents per share divided by 1.33% derives a target price value of $13.53 per share.

That price target represents a potential gain of 15.1% for HAL stock. That assumes that the price of the stock assumes an average dividend yield of 1.33% over time.

Based on this, I think there is still room for HAL stock to rise over time, even if the company’s cash flow and dividend do not rise for a while. For most patient investors, it looks like a reasonable yield play.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide, which you can review here.