Are we getting another wave of the novel coronavirus? If so, Alibaba (NYSE:BABA) stock and the rest of the market may quickly come back under pressure.

Texas just recorded its worst one-day rise in Covid-19 cases. Florida had its worst seven-day stretch of new cases too. California’s not doing well either, recording higher hospitalizations in nine of the last 10 days and at the highest level since May 13th.

As a result, the S&P 500 dove 5.9%, the Dow shed almost 7% and the Nasdaq dipped 5%. The markets don’t like these reports and it shows just how much sentiment drives equity prices. If there’s a whiff that Covid-19 is rising back up, stocks may head back down.

If that’s the case, consider Alibaba stock one to buy on the dips.

Coronavirus vs. Commerce

If the coronavirus outbreak taught investors anything, it’s that the stocks that can survive will do OK, but those that thrive can hit new highs.

Look at Chewy (NYSE:CHWY), Amazon (NASDAQ:AMZN), Netflix (NASDAQ:NFLX) and

Zoom Video (NASDAQ:ZM). All of these companies benefit from coronavirus, as bad as it sounds to say that. The rationale is simple. Even though many of these companies experience rising costs, demand goes through the roof.

Alibaba shouldn’t be exempt.

It’s by far the largest e-commerce player in China, which boasts more than 1.3 billion people in the second-largest economy in the world. While most of its revenue comes from e-commerce, Alibaba also has other revenue streams, including digital media and cloud computing.

In a way, it’s reminiscent of Amazon, isn’t it? While Amazon has built out a powerful ecosystem, it’s set up in a similar manner.

Let’s put it this way, consensus estimates call for Alibaba to grow revenue by 30% this year. Forecasts call for another 25.5% growth next year. These are robust numbers, particularly for a company with a $600 billion market cap.

When it comes to the bottom line, most companies are feeling a coronavirus-related pinch. Alibaba stock is no different. Estimates are falling over the past few months, but still call for growth of 13.5% this year. In-line results has Alibaba earning about $7.50 per share this year. Next year estimates call for 26% earnings growth.

It ultimately leaves Alibaba stock trading at about 28.5 times this year’s earnings, which is reasonable for a company with solid growth, with or without a second wave of Covid-19.

Alibaba will continue to drive sales higher, both now and in the long term. That has me interested.

Trading Alibaba Stock

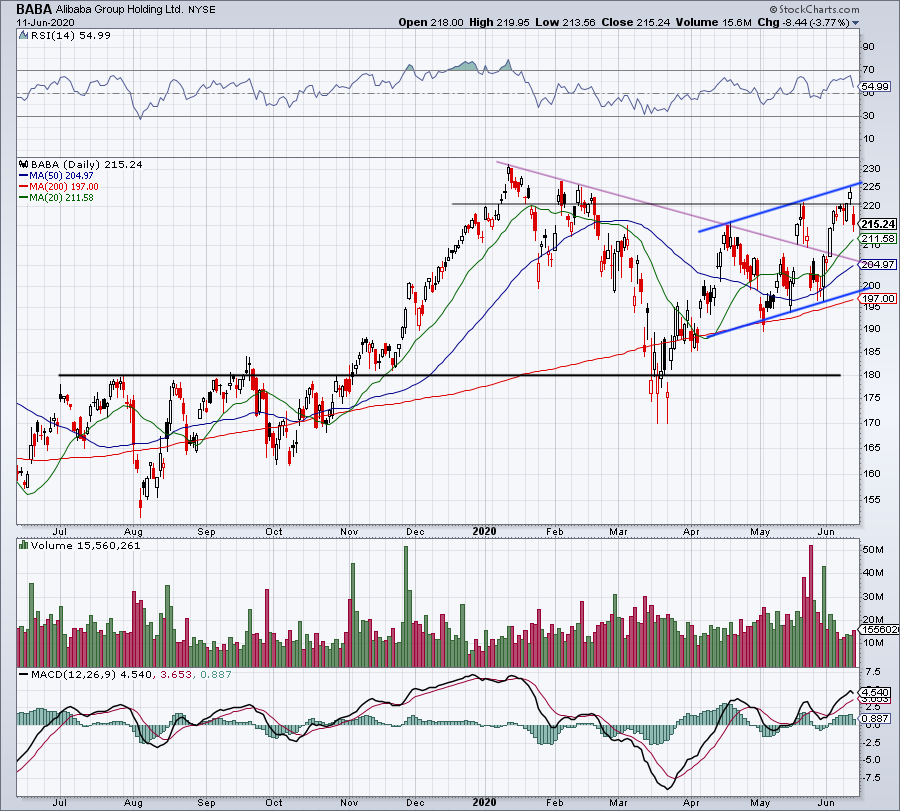

Click to Enlarge

For some investors, Alibaba being a Chinese equity makes it a liability. That’s with the U.S.-China trade war dragging on and with issues Chinese equities listed in the U.S. However, Alibaba is not Luckin Coffee (NASDAQ:LK).

Still, some investors may feel more comfortable with Amazon or other mega-cap U.S. tech giants. For those that like Alibaba though, the fundamentals check out. It’s a strong, diversified conglomerate with plenty of runway. But how do the technicals look?

Shares have been trending higher in a rising range (blue lines), as the 200-day moving average continues to act as support. Further, despite Alibaba stock falling almost 4% on June 11th — outperforming the broader U.S. stock markets — shares are above all the major moving averages.

As attractive as a dip down to the 50-day moving average and backside of prior downtrend resistance (purple line) would be, I prefer a slightly deeper dive. Specifically, I’d like a drop down to range support and the 200-day moving average.

Below puts $190 in play, but until support begins to break, I want to look at Alibaba stock as one to buy on the dip. Should support give way, then that thesis changes. For now though, I am cautious as equity markets show signs of a potential dip, even though Alibaba has strong fundamentals and technicals.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he did not hold a position in any of the aforementioned securities.