When the novel coronavirus first began disrupting the U.S. economy, the argument for energy companies like Marathon Oil (NYSE:MRO) was an easy one: just sell, baby! With the Covid-19 pandemic again rearing its ugly head, the story is still the same. Don’t get cute with MRO stock and avoid it like the plague.

In a bull market, the risk-reward profile for the crude oil industry is much more palatable. Even if the sector encounters a wave of volatility, demand should eventually pick back up. Before the paradigm-shattering event of the coronavirus, unemployment stood at multi-year lows. Additionally, Wall Street was enjoying record-busting valuations.

At the time, I was optimistic that big oil firms like Exxon Mobil (NYSE:XOM) and Chevron (NYSE:CVX) could turn investor sentiment positively. I know I would have been bullish on MRO stock if I were covering it during the period before everything changed. Now, the fundamental argument for oil is risky and flawed.

Primarily, in order for me to feel comfortable with Marathon or any industry player, I’ve got to see the demand picture improve. Essentially, this means a return to full-capacity automotive traffic. However, when I analyze TomTom.com’s traffic index, I notice that major U.S. cities still lag their year-ago traffic levels by a wide margin.

To be fair, traffic has been growing significantly since the March and April lows. Further, positive economic data, particularly the May jobs report, boosted sentiment in MRO stock.

Still, I was

skeptical about Marathon and its ability to thrive under a pressured environment. Frankly, I’m glad I was because shares turned volatile. And now, with the coronavirus reminding us of its presence, Marathon seems like a lost cause.

The High-Risk, High-Reward Argument for MRO Stock

If you’re someone who prefers as much predictability in their portfolio as possible, you’re going to want to sit out MRO stock. Basically, that goes for all other oil-based companies. There’s nothing here that won’t cause some stomach-churning trades.

But if you live for the trade or can handle a long-term investment with wild gyrations, MRO stock could be a surprisingly profitable platform. It all comes down to the math.

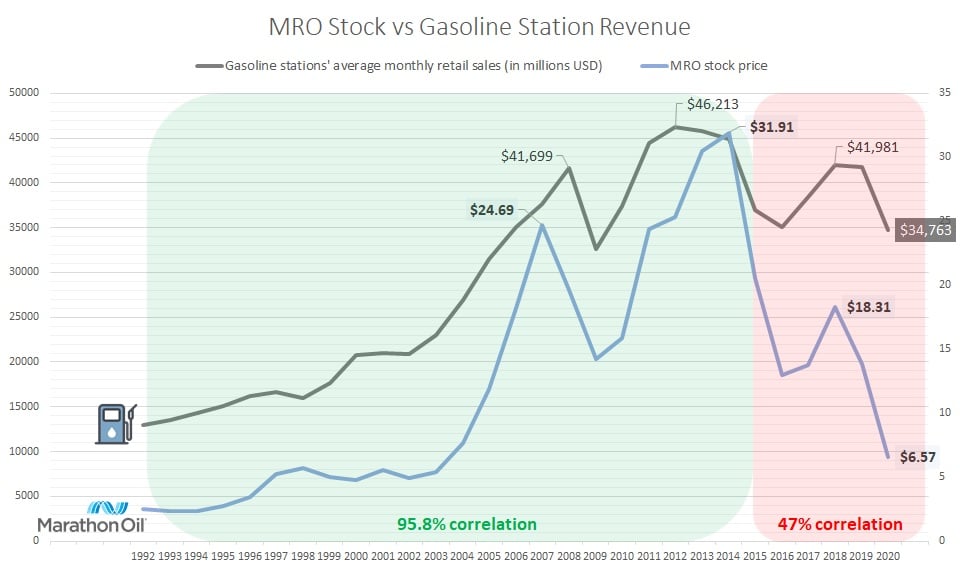

As you might suspect, Marathon Oil’s equity valuation features a strong direct relationship with retail demand for gasoline. From 1992 to May 2020, the correlation coefficient between the Marathon stock price and the monthly average sales of U.S.-based gas stations is 90.5%. Put another way, as gasoline revenue goes up, so too does MRO.

Interestingly, though, the correlation coefficient incurred a substantial disruption in 2015. From 1992 through 2014, correlation strength between the aforementioned metrics was 95.8%. But from 2015 onward, the coefficient dropped sharply to 47%.

Click to Enlarge

In my opinion, a 47% coefficient represents a “decent” relationship – a relationship exists but it’s not very convincing. As you can tell from my chart, MRO stock suffered a severe downfall starting from 2015, a descent much more brutal than what retail gasoline stations suffered.

Also intriguing is that MRO has charted a pattern similar to a head-and-shoulders formation. But monthly average gas station sales have instead charted a rising flag pattern. If I apply traditional technical analysis to this dynamic, gasoline sales are apparently signaling a “buy.”

Of course, that’s up to interpretation. However, what is a statistical fact is that MRO suffered much more sharply than its underlying industry. Theoretically, then, Marathon should revert back to its original relationship with gasoline retail sales, creating an opportunity gap you could exploit.

Some Additional Context

Before you jump aboard MRO stock on the basis that the math is good, let me share a warning. Yes, the math is good, but it’s only so for the framework that I have arbitrarily defined. If reality contradicts, so to speak, my framework, it doesn’t matter how good the math is, you’re going to take a loss.

In other words, you can exploit the opportunity gap I mentioned only if demand for oil-based products increase significantly. However, if the coronavirus has other plans, guess what? Marathon stock could again tumble back into the doldrums.

At the same time, from this new angle, shares are tempting from a dumb speculation perspective. For one thing, at the time of writing price below $6, we haven’t consistently seen these levels since the 1990s. And you’ve just got to wonder how low MRO can go. It’s not as if oil is completely useless.

So, I’m going to watch this name very carefully. Obviously, I’m most worried about the coronavirus and how it could destroy consumer sentiment. But if we can somehow avoid serious repercussions from this resurgence, perhaps MRO stock could win out. Just be extremely careful because Marathon is a low-confidence idea.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.