Netflix (NASDAQ:NFLX) stock has been hot over the last few months. It hasn’t taken a rocket scientist to realize that the novel coronavirus is driving new subscriptions and that is fueling the company’s growth. However, Netflix stock dove almost 10% at one point after the company’s Q2 report.

Is the growth story over?

Not exactly. Netflix reported a solid quarter, but given the run we’ve seen in the stock price, some air needed to come out of this balloon. Ultimately that’s good for the bulls, though. We don’t want to see stocks run indefinitely, with rallies going unchecked. That’s not healthy. Pullbacks are healthy and that’s exactly what we’re getting with Netflix stock.

Netflix Earnings

The company reported earnings of $1.59 per share, missing estimates by 22 cents. Revenue of $6.15 billion grew 25% year-over-year and eked past expectations by $70 million. That’s despite the company adding more than 10 million new subscribers in the quarter, crushing expectations of 7.5 million.

Recall that last quarter, Netflix added almost 15.8 million new subs vs. expectations of 8.5 million. So now we’ve seen almost 26 million new signups in the last six months. Talk about impressive!

By and large, the quarter was very good but perhaps one would hesitate to call it great. That’s particularly true as management guided for Q3 subs of just 2.5 million vs. expectations that are north of 5 million. That said, they also guided conservatively for Q2 too, but that’s besides the point.

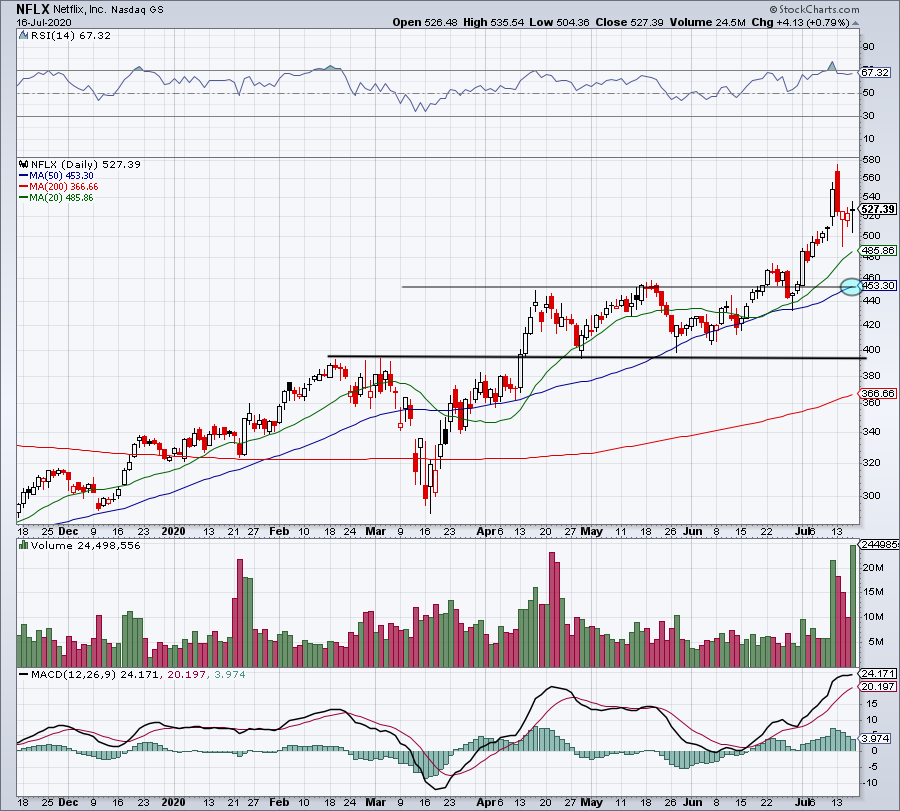

What we’re seeing is a rebalancing of expectations. Despite the recent dip, Netflix stock was up 23% over the past month ahead of earnings. Shares were up 32% from the May low and more than 80% from the March low.

If Netflix was down 110 points over the past month ahead of the print vs. up 110, we would likely be seeing a different reaction.

The Long-Term Thesis Is Unchanged

Bears love to hate on Netflix because it doesn’t have the traditional financials of a regular company. Therefore, it doesn’t follow traditional valuation metrics, which when applied, make the streaming company’s stock look completely overvalued.

But simply put, these valuation metrics don’t apply. The same can be said for stocks like Amazon (NASDAQ:AMZN), Tesla (NASDAQ:TSLA) and Salesforce (NYSE:CRM).

Some will argue that that statement is true, “until it isn’t.”

Perhaps they are right and Netflix stock will face its day of reckoning to the valuation overlords. But in the meantime, the stock has risen 355% over the past five years and 3,000% over the last decade. If bears can live with the risk of 3,000% upside, then bulls should be able to live with the downside risk of 100%.

When it comes to the long term, Netflix should keep on winning. The company is nearing 200 million subscribers and every quarter it keeps adding to that sum. This equates to monthly cash flow — a subscription model — that continues to grow over time.

Further, this cash flow is virtually recession proof. When people lose work, they don’t stop craving entertainment. Cable at $50 to $100 a month may not make the budget, but $10 for Netflix just may.

Obviously the company spends a lot on content, as it’s now in fierce competition with other streaming platforms. Surprisingly though, this added competition may work in Netflix’s favor. With more streaming options than ever before, more consumers may be willing to cut the cord. That doesn’t guarantee that Netflix will be purchased, but there’s a solid likelihood of it happening.

Bottom Line on Netflix Stock

Click to Enlarge

While shares dipped slightly ahead of earnings, Netflix stock was simply too high for anything less than a blowout result. In the minutes after the company first reported, Netflix dropped toward $450 before bouncing.

There it found the 50-day moving average. That may be a reasonable buying spot for investors, should that level be retested in the coming days or weeks. Below that and look for a retest of prior range resistance, just below $400.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.