Honeywell International (NYSE:HON) has basically been flat for the past year. This is despite the fact that HON stock is up over 41% in the past six months. Still, don’t wait around for this stock to suddenly pop.

For one, analysts expect earnings to rise by just 13.5% next year. They have an average earnings estimate of $7.82 per share for 2021, vs. $6.89 EPS forecast for 2020, according to data on Seeking Alpha.

That is nothing to get really excited about. Moreover, since HON stock was trading at $168.70 on Sept. 18, the price-to-earnings ratio was 20.95 for 2020 and 21.83 times for 2021.

This implies very little upside for the stock because Morningstar shows that Honeywell’s average P/E has been 27.9 in the past five years. So, theoretically, at 27.9 times earnings for 2020, the stock should be at $192.51 and $218.48 for 2021. The average of these two prices is $205.50. That represents a gain of just 21.8% over today’s stock price.

That is not a bad return. But it is nothing very exciting, either, especially since there are plenty of other tech stocks that are likely to do much better than that.

Business Is Solid

Despite the valuation issues mentioned above, Honeywell is a solid cash-generating technology company, with a diversified revenue business. For example, it makes money in aerospace, building technology, smart energy products and safety products, including PPE (personal protection equipment) products.

For example, last quarter the company produced $1.253 billion in free cash flow (FCF). This represents a reasonably good 16.8% of its $7.477 billion in sales. In other words, the company produces solid FCF, even though this was down 17% from last year.

By the way, Honeywell likes to talk about its “conversion” ratio. I want to explain what this is and why you shouldn’t even bother with it.

Honeywell defines its conversion ratio as free cash flow divided by net income, not including certain types of adjustments. For example, the company said that its “adjusted” FCF conversion ratio was 140% in Q2, up 40% from last year.

What does that mean? FCF was higher than net income by 40%, so the ratio was 140% in Q2. But here is what really is happening.

Net income typically includes all sorts of non-cash items. One of the biggest items is stock-based compensation expenses (SBC). However, FCF does not include any of these SBC and non-cash expenses that result in cash expenditures by the company. So naturally, FCF will “convert” into a higher number than net income.

In essence, there is nothing special or exciting about a greater than 100% FCF conversion ratio. In fact, if a company does not have a greater than 100% conversion ratio I would be concerned. It is much more important to simply measure how fast FCF grew or to measure the FCF margin (i.e., percentage of sales) than its conversion ratio.

Where This Leaves HON Stock

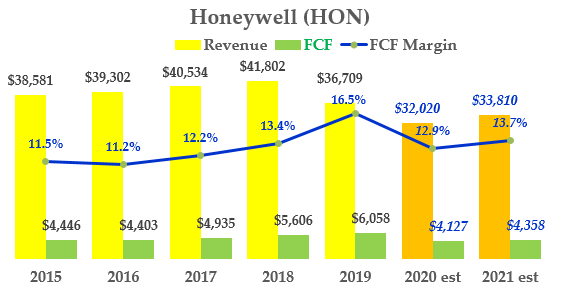

Honeywell is expected to make FCF margins of 12.9% this year and about 13.7% next year. This is slightly below its historical average.

Click to Enlarge

You can see this in the chart I have put together above. Sales have dipped but the company is still producing high levels of FCF, albeit at lower margins. You can see that over the next several years, it is likely to recover.

In other words, Honeywell is a solid earner. But the problem, as I showed earlier, is that much of this is already baked into the HON stock price valuation.

Moreover, some of its competitors have cheaper valuations. For example, 3M Company (NYSE:MMM) trades for just 20.6x 2020 forecast earnings, as well as 18.6x 2021 estimated EPS.

By comparison, as shown above, HON stock trades at 24.9x earnings for 2020 and 21.6 times for 2021. That is 20.8% higher than MMM stock for 2020 and 16.1% higher for 2021. Moreover, both companies have similar revenue levels — $32 billion to 33 billion per year.

In addition, Emerson Electric (NYSE:EMR) is also cheaper than HON stock, although not as much as MMM stock. The point I am making is that investors in Honeywell have good choices in terms of valuation.

Therefore, you have a tradeoff with Honeywell. On the one hand, Honeywell’s fundamentals are very solid. On the other hand, HON stock trades at a relatively high valuation. In other words, there seems to be a low margin of safety.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide, which you can review here.