In the last few months, AT&T (NYSE:T) formed a downtrend as its dividend yield rose. Shareholders braced for the worst ahead of its third-quarter earnings report. Instead, AT&T stock bounced back sharply from the yearly low to close to $27 today.

Besides the generous dividend yield in the 7.5% range, investors may resume accumulating shares despite its other risks.

In the third quarter, AT&T posted impressive subscriber growth in wireless and fiber broadband. This lifted cash flow and reaffirms the company’s financial strength continued in the period. The telecom giant added over 5 million domestic wireless accounts.

Within that, it added over 1 million postpaid customers and 245,000 prepaid net additions. The net churn of 0.69% is a sharp improvement from 0.77% last year.

The entertainment group fared well, as AT&T added 357,000 Fiber customers. Still, premium TV losses are troubling but expected.

A Closer Look at AT&T Stock

WarnerMedia’s domestic HBO and HBO Max subscriptions were 38 million and 57 million globally, respectively. Importantly, AT&T noted that “Domestic HBO and HBO Max subscribers do not include customers that are part of a free trial.”

Investors should not take the small detail of including trial users lightly. Once the trial ends, the user base may either fall sharply or not grow as much as the numbers imply.

The company did not specify how much it lost from the Warner Bros. film and television unit. Still, its expenses fell to $36.2 billion, compared to $36.7 billion last year. Turner programming costs rose as it shifted sports programs from the earlier part of the year.

Apple’s (NASDAQ:AAPL) iPhone launch is a positive catalyst for driving subscription growth in wireless. For example, customers need a low band spectrum to penetrate inside buildings. So, as it continues to upgrade its network, it will promote the iPhone launch concurrently. This will lead to low churn rates, thanks to the satisfied customer base.

AT&T is managing its cash flow well, despite the potential headwinds from its media division. It did not give guidance on its capital spending plans yet. When it does so later on this year, investors will have a better idea of how it manages to spend against cash flow. The current financial strength suggests that the dividend is very safe.

If AT&T modifies any of its spendings, it is more likely to buy back more stock or raise its dividend slightly. This would signal the confidence it has in its balance sheet.

Income investors would accumulate more AT&T shares. Furthermore, the very low-interest-rate environment would encourage investors to hold its stock than to stay in cash. For AT&T, the low rates will decrease the cost of interest on debt upon its renewal.

Fair Value

Click to Enlarge

On simplywall.st, the estimated fair value is $70. This is based on its future cash flow discounted to present value.

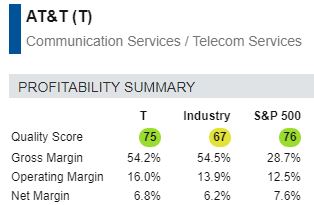

Conversely, the company has strong profitability characteristics. Look at the gross margin, right. It is on par with the industry and above that of the S&P 500 index:

To reach its full value, AT&T still needs activity from the Warner unit recovering. The Covid-19 environment hurt the business earlier this year.

Although infections are on the rise again, Warner has around 130 productions up in running. By comparison, it had 180 productions active in Feb., before the pandemic hit.

Chances are high that California and New York will face increasing restrictions because of the pandemic. Beyond the holiday and winter season, the virus spread may ease.

Plus, the government will approve a vaccine by then, further lifting restrictions. In this scenario, investors should buy AT&T and hold it for the long-term. This is the lowest risk way of playing the re-opening of studios and movie production activity.

Disclosure: On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article.