About a month ago, I stated that while Nio (NYSE:NIO) had more room to run, shares appeared to be in bubble territory. Therefore, at some point, speculators ought to consider an exit plan. That’s not to say that NIO is a terrible investment. But everything has its price and currently, the fundamentals may not justify the Chinese electric vehicle manufacturer’s lofty premium.

From the onset, this might not sit well with those who are bullish on Nio shares for reasons other than gambling on collective emotions. I concede that there are fundamentals that are positive for the EV maker. First, China has become the world’s biggest market for virtually everything, including of course automobiles of every stripe. Second, the Asian juggernaut has handled the novel coronavirus pandemic well, even though the virus originated from China.

But the latter also feeds into why I believe investors ought to be cautious about NIO. As the National Interest asserts, China is still dependent on exports. True, finance professor at Peking University Michael Pettis notes that China has been “pursuing a strategy of boosting domestic consumption for years.” However, those efforts have been unsuccessful. Further, there are other challenges at play:

Pettis says that to rebalance the economy to give consumers anything approaching a normal share of the benefits of the economy would require shifting 10% to 15% of GDP away from businesses, the wealthy and government to households. ‘Rebalancing involves a massive shift of wealth—and with it political power—to ordinary people. This will not be easy.’

He notes that China’s export strength, on display in the latest trade figures, depends on the workforce receiving a very small share of what they produce, either directly through wages or through the social safety net.

‘China can only rely on domestic consumption to drive a much greater share of growth if workers begin to receive a much higher share of what they produce, so the very process of rebalancing must undermine China’s export competitiveness.’

In other words, weakness in the export market – due in large part to record-breaking coronavirus cases in the U.S. as well as a second wave in Europe – means that China must rely on domestic resilience to bolster its broader economy. But such efforts have faltered in the past nor does this time look any different.

Consumer Fundamentals Don’t Make Sense for Nio Stock

At the end of my article last month, I stated that China’s consumer economy needed to be more robust for NIO to be credible at its present premium. Here, I referenced data that suggests Beijing’s GDP per capita was $24,479, much lower than Los Angeles’ GDP per capita of around $69,000.

Long story short, the income threshold in China’s biggest cities needs to be much higher for Nio’s sales narrative to comfortably make sense. For instance, when Tesla (NASDAQ:TSLA) has massive sales in California, I believe it: the Golden State’s major metropolitan areas are collectively loaded and can afford luxury EVs.

Having looked into the consumer sustainability issue, I’m even more skeptical about NIO indefinitely maintaining its growth trek. According to AverageSalarySurvey.com, the average income in Beijing is equivalent to $44,570

. Again, that’s very low when you’re talking about Nio’s economy model coming in at a pre-subsidy price of roughly $54,000.

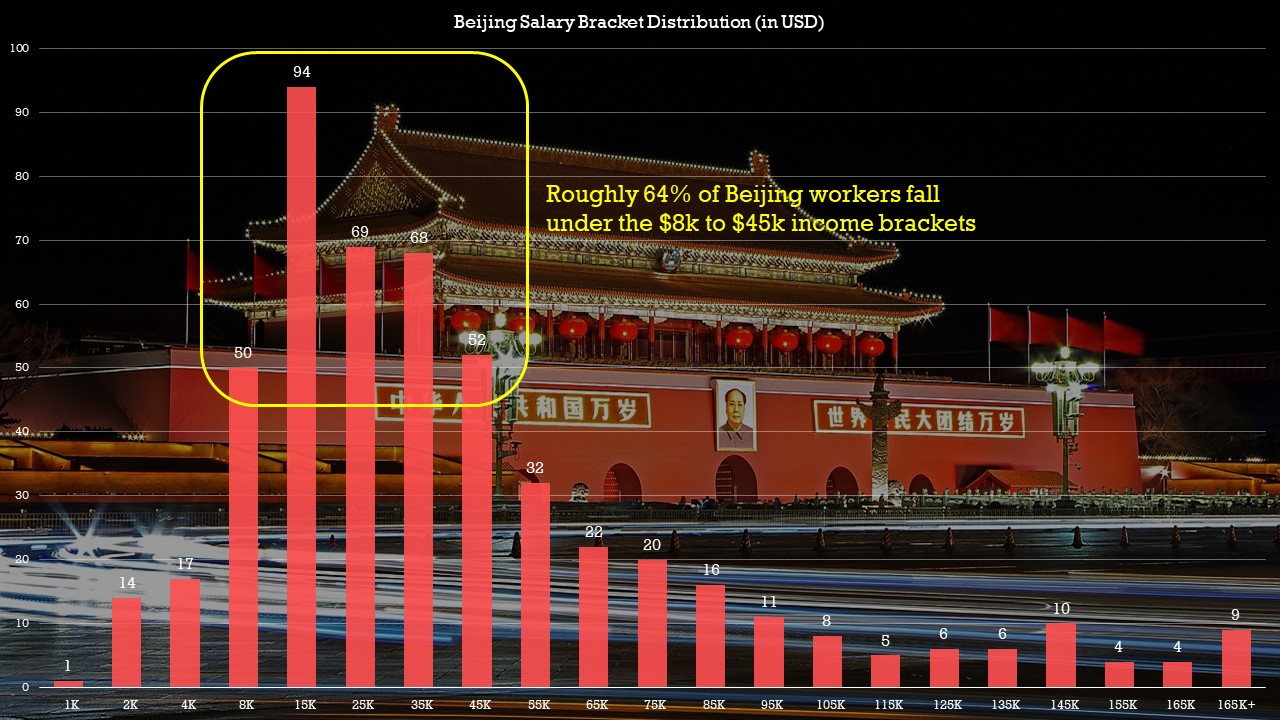

But the income distribution is where things get shakier. The majority of Beijing residents (or 18%) have an income level in the $15,000 bracket. Moreover, 64% of residents earn income between the $8,000 to $45,000 bracket. That’s not going to cut it for a $54,000 car.

Click to Enlarge

True, many Chinese workers are high-income earners. But realistically, those that can afford the lowest-cost Nio car represent only about 12% of Beijing’s labor force. Granted, NIO may have jumped higher because the underlying company executed well in its marketing message to its core customers.

But you know that phrase, the good news is priced into the stock? What if the tremendous sales growth narrative has already been accounted for?

I’ll repeat, I’m not suggesting that NIO is a bad investment. Moreover, I get that China is the world’s biggest automotive market. But that status isn’t exclusive to premium luxury cars. For EVs to be truly viable, the burgeoning market must be accessible to middle-class earners. A vehicle that costs above $30,000, let alone $50,000 is not it.

China Doesn’t Have a Covid-19 Reprieve

With President-elect Joe Biden winning the contentious 2020 election, the Chinese government must surely have breathed a sigh of relief. After all, the outgoing Trump administration was promising nothing short of hellfire and fury to hold the country responsible for the coronavirus pandemic. At least on paper, a Biden administration would seem more approachable for a less draconian policy.

But whatever happens next, the National Interest noted that international bitterness against China remains. It’s not hard to see why. The coronavirus originated from China while its government, along with the bumbling World Health Organization, concocted an arrogantly maddening defense of the Chinese initial response. Now, the world suffers while China enjoys a robust economic recovery.

Well, for those who believe China should get slapped with some karma, payback might be coming. As I mentioned earlier, China depends on its exports. If the international economy falters, there’s probably no way that the Chinese can get away unscathed.

Moreover, the Chinese consumer response to the initial pandemic has been deflationary “because households have responded to the surge of unemployment following the coronavirus outbreak by slashing consumption and redoubling their savings.”

Put another way, China might not get a second wave. But its consumer economy will likely feel the pain as everybody else suffers. And that probably won’t be to NIO’s favor, necessitating at least the idea of formulating an exit plan.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.