Other than a short-lived spike to $67 earlier this year, Tilray (NASDAQ:TLRY) stock gave nothing but grief and losses for shareholders.

On the bright side, TLRY livened up recently, closing its acquisition of Aphria on May 3.

With consolidation lowering costs and revenue rising, what is the upside potential on Tilray?

When Tilray and Aphria announced the closed merger the press release claimed it was a global cannabis leader, which seems unwise given that competition is fiercer than ever. Still, the company said Irwin Simon, Aphria’s Chairman and Chief Executive Officer, will lead the combined firm.

“New Tilray” also appointed new leadership. Most importantly, Tilray said the combined firm will lead the cannabis-focused consumer packaged goods (“CPG”). In that segment, Tilray will have the largest global geographic footprint in the industry.

Skeptical investors may ignore the flashy headline and look ahead at operating margins. Unless revenue greatly outpaces costs, Tilray will keep losing money. That business model is not sustainable.

A Closer Look at TLRY Stock

“Our global team is laser-focused on turning potential into performance and addressing consumer and patient needs for safe, innovative, and high-quality products,” said Simon.

To get there, the company will deliver $81 million in cost synergies within 18 months. It will achieve cost synergies in all areas of the business. This includes sales and marketing, corporate expenses, cannabis and product purchasing, and cultivation and production.

The operating cost cuts aren’t surprising. The merged firm does not need overlapping sales and marketing initiatives.

Simon said in

this presentation that the combined business will give Tilray around 20% market share, though Simon’s ambitions are to grab a 30% market share.

Investors will find out over the next few quarters if the merged firm will cut costs enough to post profits. In the United States, Multi-State Operators (“MSOs”) post strong profit growth because they focus on key markets. They do not dilute their profits by spreading themselves thin.

Risks Abound for TLRY Stock

The New Tilray has a bigger market capitalization than before. This does not guarantee that the stock will hold current levels. Fortunately, markets are returning to a euphoric sentiment. This could give Tilray shares another lift back to highs not seen in months.

Valuations are another risk. Tilray is trading at unsustainable price-to-sales multiples of over 40 times.

The company is not debt-free, so it may need to sell shares to lower its debt levels. For now, interest rates are low, so Tilray is in no rush to retire debt.

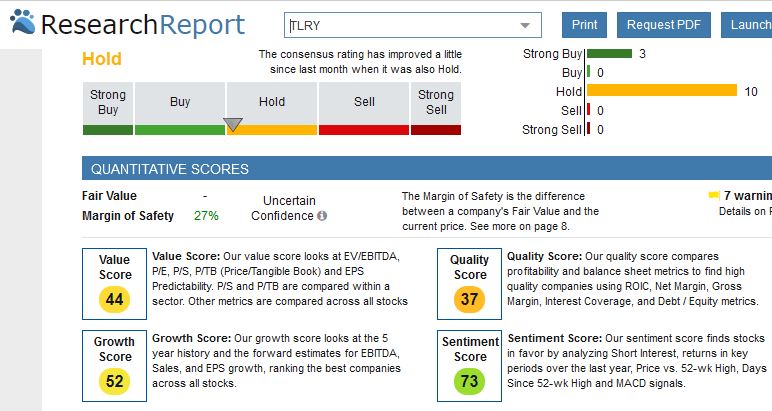

Fair Value

On Wall Street, the 10 analysts covering Tilray have a “hold” rating on the stock. The sentiment score is green, at 74/100, because of the recent rally.

The quality, value and growth scores are about average. This leads to a margin of safety of almost 30%. This implies that the stock has potential upside at the same percentage.

In the research report, Tilray shares could benefit if analysts change their rating from hold to buy. Management must demonstrate underlying strength in product sales before earning that upgrade.

Tilray is in a post-merger transition. The stock could continue its uptrend over the year, but if bears decide to close their 11% short float position on the stock, it could help the price rise quickly.

Speculators could start a small position on Tilray for now. As the company posts smaller losses and growing revenue, investors may accumulate a bigger position over the course of the next year.

Investors should not take a full position on Tilray, since that opportunity came and went. The stock is trading sharply above the $4.41 52-week low. So, if the stock pulls back in the low teens, it will give investors a better entry price than is currently offered.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.